Offsetting Low Yields in a Portfolio

A spoonful of midstream/MLPs or closed-end funds can help remedy lower yields in your income portfolio.

Building an income portfolio today is not as easy as it used to be. With broad market indexes and income sectors like REITs and utilities hovering near all-time highs, the yields for many equity income investments are noticeably lower now than in the past. This can create challenges for an advisor or individual investor trying to build an income portfolio and achieve a certain yield. Today’s note briefly discusses the income challenge facing investors and how allocations to midstream/MLPs or closed-end funds can help offset lower yields elsewhere in an income portfolio.

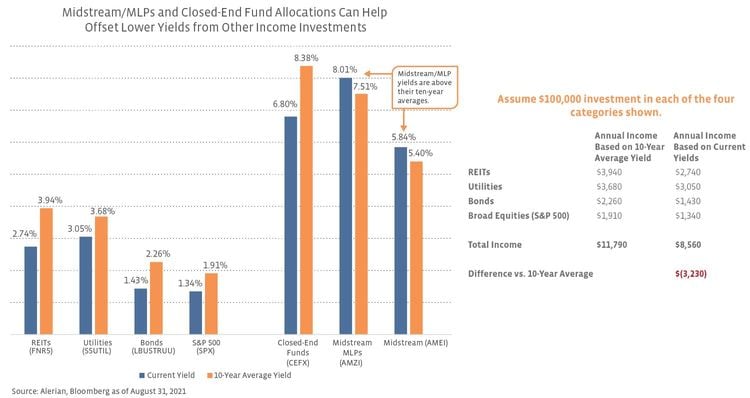

The current yield profile of bonds and income-oriented equities may leave investors less than satisfied. As shown in the chart below, REITs and utilities are currently yielding 120 and 63 basis points, respectively, below their ten-year averages. If an advisor typically depends on a diversified REIT allocation to provide a 4% yield in an income portfolio but REITs are yielding less than 3% today, the advisor will either have to accept lower income or find other investments with more attractive yields. To better quantify this predicament, the example below assumes an allocation of $100,000 each to REITs, utilities, bonds, and equities. The annual income at current yields is ~$8,600, whereas the annual income based on the ten-year average yield would have been ~$11,800.

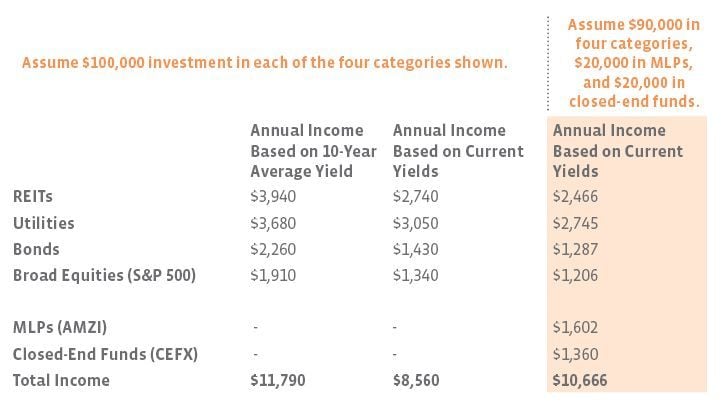

For advisors or investors looking to enhance yield, a relatively modest allocation to midstream/MLPs or closed-end funds could help boost the portfolio’s income. The additional example below again assumes $400,000 is invested with the bulk in REITs, utilities, bonds, and equities ($90,000 each). However, this time the example assumes that $20,000 is allocated to midstream MLPs and $20,000 to closed-end funds. The total annual income based on current yields is ~10,700 instead of ~$8,600.

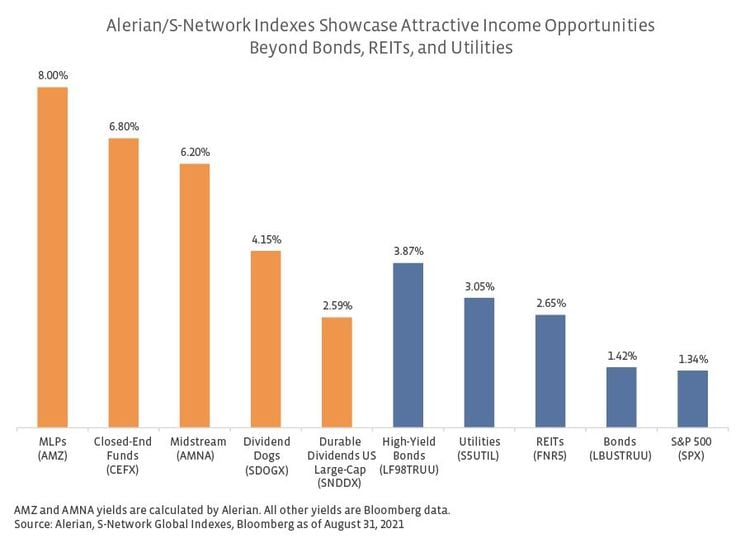

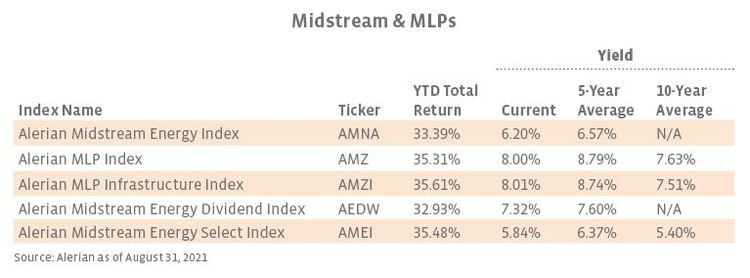

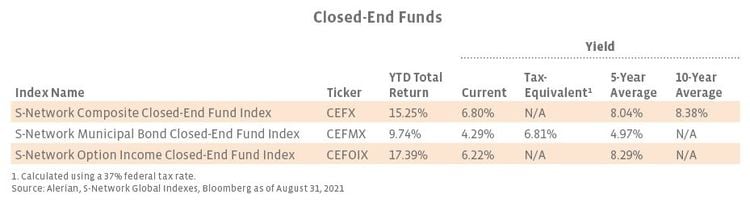

As demonstrated, a relatively small investment in MLPs or closed-end funds can have a fairly significant impact on the income of a portfolio. While not included in the example, an allocation to midstream, represented by the Alerian Midstream Energy Select Index (AMEI), would also enhance portfolio yield relative to REITs and utilities. The AMEI Index includes 75% midstream corporations and 25% midstream MLPs. Notably, the AMEI Index and midstream MLPs, represented by the Alerian MLP Infrastructure Index (AMZI), had yields above their ten-year averages at the end of August. In addition to enhancing yield, midstream/MLPs can provide other portfolio benefits, including real asset exposure and diversification given MLPs’ exclusion from broad market indexes. Closed-end funds, represented by the S-Network Composite Closed-End Fund Index (CEFX), were yielding below their ten-year average on August 31, but current yields are still more generous than the other categories shown.

In summation, while lower yields across several asset classes can make it challenging to build a new income portfolio and achieve a certain yield objective today, a modest allocation to midstream/MLPs or closed-end funds can help boost a portfolio’s income profile to offset lower yields elsewhere.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR). CEFX is the underlying index for the Invesco CEF Income Composite ETF (PCEF).

Current Yields vs. History

Midstream yields are generally below 5-year historical averages but are above the 10-year averages. Dividend stability over the last several quarters adds confidence to midstream yields (read more).

Of the S-Network Sector Dividend Dogs, EDOGX stands out for offering a yield above its five-year average. RDOGX offers a more generous yield than the FTSE NAREIT Real Estate 50 Index (FNR5) discussed above.

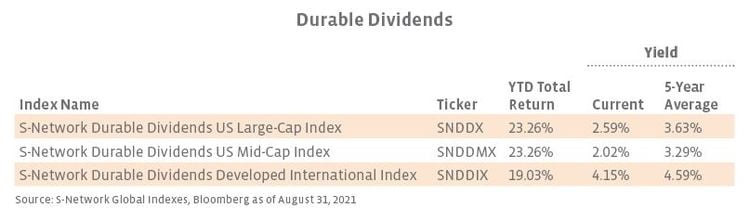

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes. While current yields are below the 5-year average, they are well above the S&P 500’s current 1.34% yield.

Though current yields are below historical averages, closed-end funds continue to represent an attractive option for enhancing the yield of an income-oriented portfolio as discussed above. Municipal bond closed-end funds may be particularly attractive given that muni bonds generate interest income that is exempt from federal taxes.

Related research:

Midstream/MLPs: Summer Sell-Off Feels Overdone

Midstream/MLPs: Well-Positioned for Inflation

Income Opportunities: Interpreting Closed-End Fund Distributions