Insights at a Glance: A Review of MLP Distributions During the Financial Crisis

With broader markets under pressure and MLP yields near all-time highs, many investors are questioning the stability of MLP distributions. Alerian has already addressed improved distribution coverage at length (read more), but what can we learn from the past? While investors wait for increased visibility (typically distributions are announced beginning in mid-April), history may help in contextualizing the durability of MLP yields.

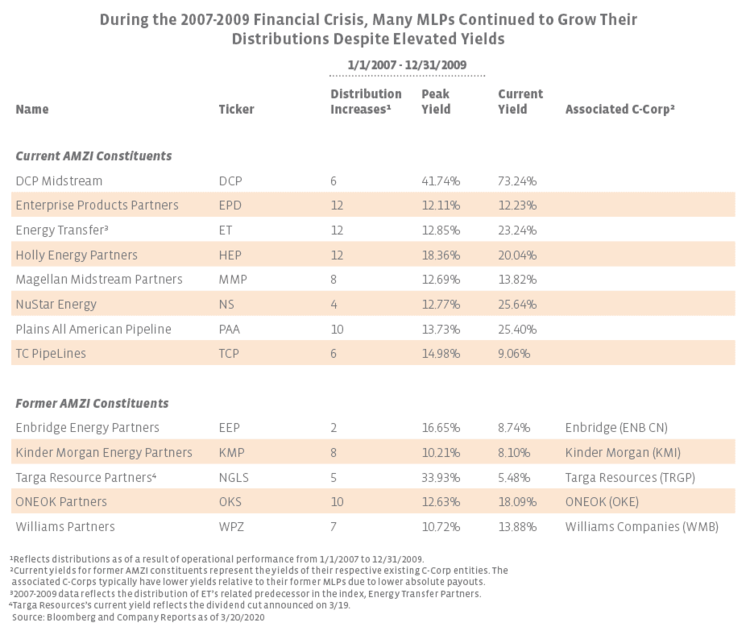

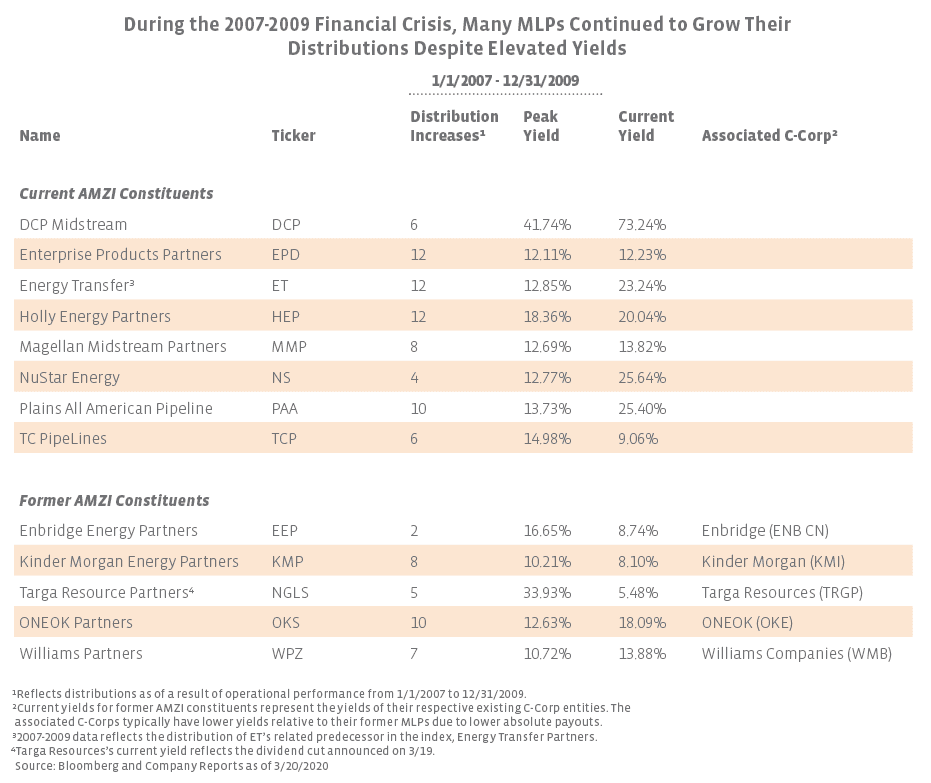

The table below shows how the distributions and yields of current Alerian MLP Infrastructure Index (AMZI) constituents and the former MLPs of several midstream C-Corporations fared during the 2007-09 financial crisis. As a reminder, the S&P 500 fell by 57% from October 2007 to March 2009. Admittedly, this was a much different time for MLPs: general knowledge of the space was limited, liquidity was very thin, and there were no MLP exchange-traded funds or mutual funds. However, this time period also shares a few key similarities with today’s market, including broader macroeconomic volatility and a significant decline in MLP and oil prices. From 1Q07 through 4Q09, none of the partnerships in the table below cut their distributions despite yields climbing over 40% in one case. Additionally, many MLPs continued to grow distributions. Three AMZI constituents, Enterprise Products Partners (EPD), Energy Transfer (ET), and Holly Energy Partners (HEP), consistently raised their quarterly distributions throughout the financial crisis, demonstrating that an elevated yield does not always imply a cut.

While many MLPs have not provided new guidance, a few have provided updates since oil prices collapsed. EPD declared its 1Q20 distribution last week at the same level as its 4Q19 payment, while HEP and Rattler Midstream (RTLR) have reiterated 2020 distribution guidance (read more). On the other hand, DCP Midstream (DCP) announced a 50% distribution cut this morning. DCP’s yield above 70% as of Friday was clearly an outlier in the table below. With the cut, DCP’s yield based on Friday’s closing price is 36.6%, which is slightly below the peak yield from 2007-09. While distribution cuts could be on the horizon for some partnerships, an elevated yield does not always result in a cut based on history. Furthermore, less reliance on equity capital markets, lower leverage, and higher distribution coverage leave today’s MLPs better positioned to withstand an economic and oil price downturn (read more).

{kind=link}