Insights at a Glance: Examining Improved MLP Financial Footing Since 2014

Given the staggering 58.5% year-to-date drop in oil prices to $25.32 per barrel (bbl) as of yesterday, investors have begun to compare the current energy environment to the downturn from 2014-2016. For context, additional supply from OPEC drove WTI crude prices down 75.6% from $107.26/bbl on June 20, 2014, to a bottom of $26.21/bbl on February 11, 2016. Consequently, annual US oil production declined in 2016 for the first time in eight years. The Alerian MLP Infrastructure Index (AMZI) dropped 59.7% from the oil price peak to its trough, and several MLPs cut their distributions. However, this was a much different time for the industry. Midstream MLPs were growing rapidly in order to meet the demand for additional energy infrastructure caused by the shale boom and were reliant on equity capital markets to fund that build-out. In many cases, these companies also had a large amount of debt on the books, were burdened with incentive distribution rights (IDRs), and had a thin cushion between cash flows generated and distributions paid. When equity capital markets began to close on MLPs, distribution cuts were necessary to direct capital to either growth projects or debt payments. Once oil prices began to recover in 2016 and in the following years, the MLP sector began to further emphasize balance sheet strength, distribution coverage, the elimination of IDRs, and self-funding the equity portion of capital expenditures. Additionally, after years of maximizing spending to keep up with US oil and natural gas production growth, the majority of midstream companies likely reached peak growth capex within the last two years (read more). Several MLPs have gone on to further cut back on discretionary spending given the shift in the macro environment (read more). The combination of these efforts represents a significant transformation of the space and has strengthened the MLP business model.

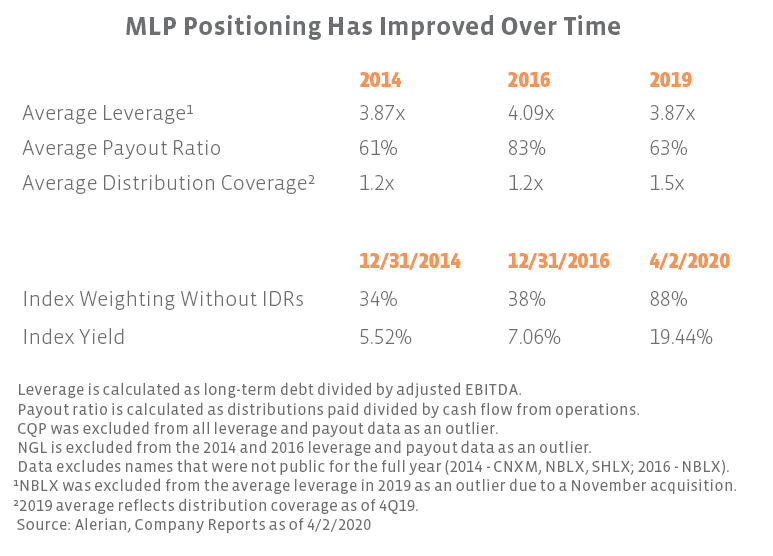

The table below compares the average leverage, distribution coverage, and payout ratios for current constituents of the Alerian MLP Infrastructure Index (AMZI) for 2014, 2016, and 2019. The table also shows the percentage of constituents by weighting that have eliminated IDRs. Leverage and payout ratios are flat when compared to 2014, but AMZI constituents have improved in each category analyzed since the end of 2016. While the elimination of IDRs is the most dramatic change, the rise in average distribution coverage is more evident of the shift in MLPs’ business models, as companies retain cash flows to fund growth spending and reduce leverage. Despite the positive progress that has been made, the current AMZI yield, which incorporates recent distribution cut announcements, is significantly higher than at year-end 2014 or 2016, implying that more risk is being priced into MLP equities in the current oil and gas price environment. While yields are elevated, these changes leave AMZI constituents better positioned to withstand market volatility.

{kind=link}