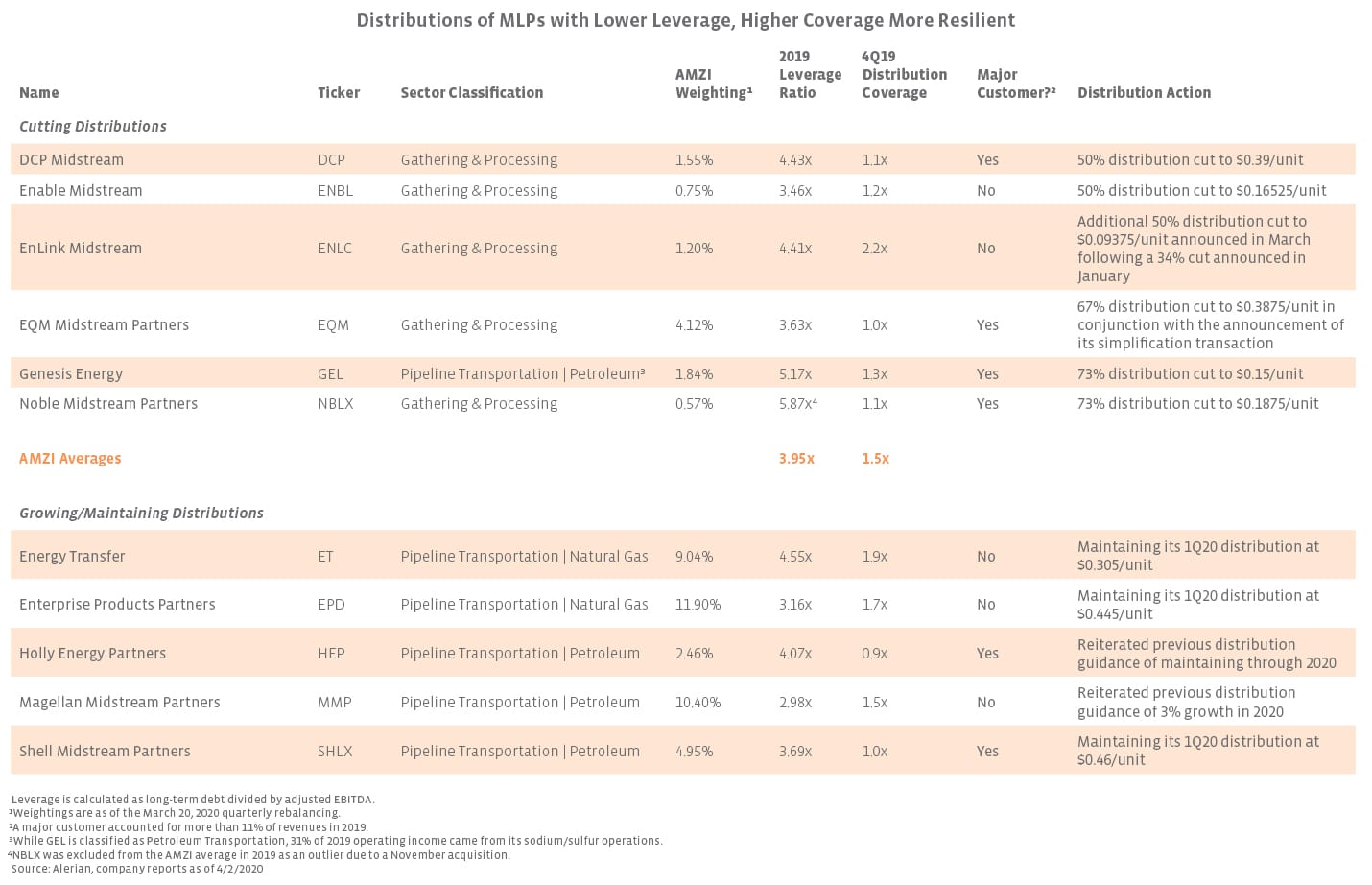

Since oil prices collapsed in early March, several MLPs have announced changes to their capital allocation plans which, in some cases, have included revised distribution policies. While primarily fee-based cash flows and the company-level improvements made in recent years position MLPs to better withstand the current weakness in energy markets, not all MLPs are on equal footing. So far, there have been six distribution cuts announced for constituents of the Alerian MLP Infrastructure Index (AMZI), representing 10.0% of the index by weighting as of the March rebalancing. As seen in the table below, these six names typically have higher leverage and lower distribution coverage than index averages and are primarily gathering and processing MLPs, which tend to be more sensitive to commodity prices. Additionally, four of these partnerships have at least one customer that represented more than 11% of 2019 revenues. Conversely, the five AMZI constituents that are maintaining or growing their distributions in 1Q20, representing 38.8% of the index by weighting, are generally large-cap MLPs with stronger balance sheets and a greater cushion between cash flows and distribution payments (higher distribution coverage). Both Magellan Midstream Partners (MMP) and Holly Energy Partners (HEP) reiterated prior distribution guidance. MMP expects 3% growth, while HEP plans to maintain its distribution throughout 2020. Energy Transfer (ET) did not previously provide distribution guidance, but the partnership has already announced its 1Q20 distribution flat with 4Q19 and has held its payout steady since its simplification transaction closed in October 2018. Enterprise Products Partners (EPD) and Shell Midstream Partners (SHLX) are also maintaining their 1Q20 distributions sequentially despite yields climbing as high as 17.7% and 32.2% in recent weeks, respectively.

The data in the table below help contextualize why some MLPs have proactively cut distributions and why others have maintained course. While there are several other considerations that influence payouts, balance sheet strength, commodity price exposure, and counterparty risk will almost certainly continue to factor into distribution decisions. With the current headwinds in energy today, the larger, diversified MLPs are better positioned to maintain their distributions given their stronger positioning.

{kind=link}