Insights at a Glance: Highlighting MLP/Midstream's Fee-Based Exposure in Today's Tough Tape

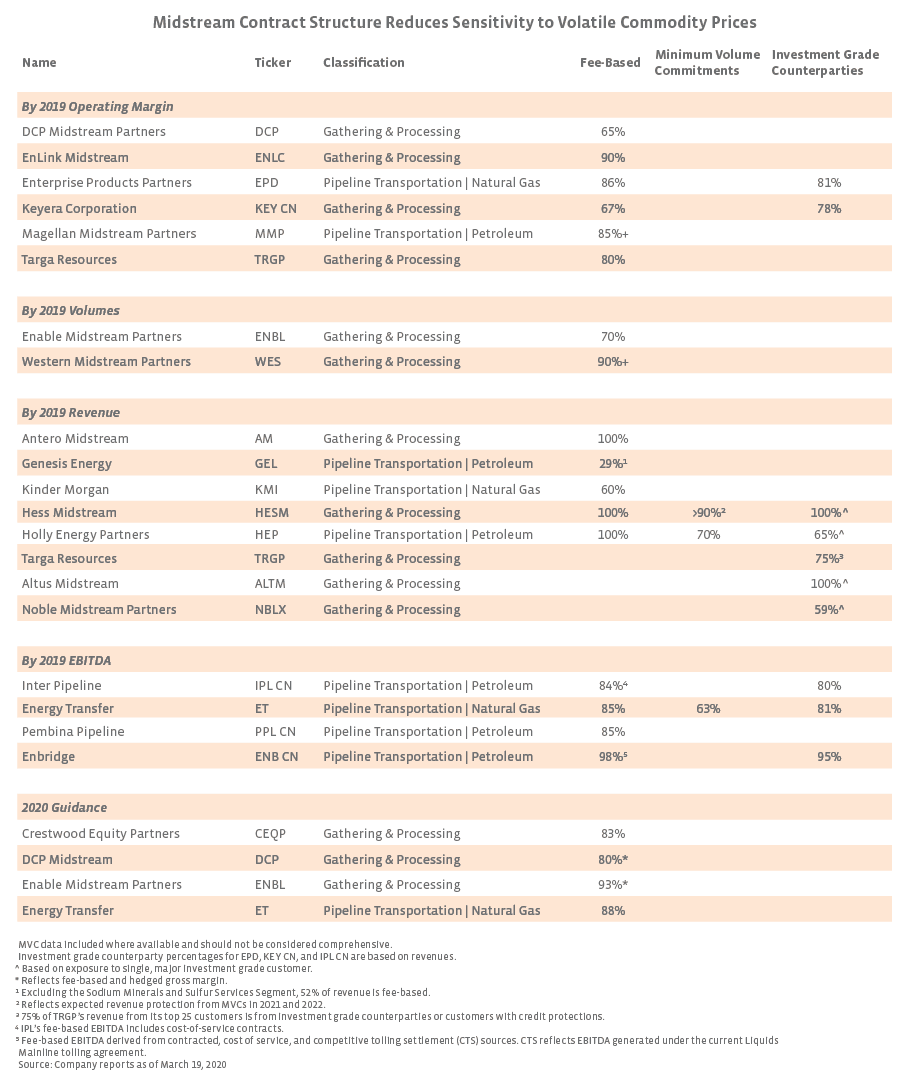

In addition to updated financial guidance, midstream companies have also provided more disclosure around the nature of their cash flows. Specifically, there has been increased commentary around counterparties, minimum volume commitments, and the portion of cash flows coming from fees. While more updates are likely to come, today’s piece provides these data points by midstream company, drawing from annual reports and recent updates.

Alerian has often pointed to the defensive nature of midstream (example) given its fee-based businesses, which should help insulate companies from sharp moves in commodity prices. Over the last several days, midstream, particularly MLPs, have not held up well amid the market volatility, raising questions about midstream’s defensiveness (though midstream has been more resilient than oilfield services and exploration and production companies year-to-date. The weakness in oil prices and broader market volatility have been exacerbated by closed-end funds selling out of positions to reduce leverage, magnifying pressure on the MLP space, which is not as widely traded as other sectors. To better frame midstream’s defensiveness, the table below outlines the fee-based nature of several companies’ cash flows and provides details on investment-grade counterparties (more detail for MLPs here) and minimum volume commitments (MVC) where data was available (the MVC data should not be considered exhaustive). Looking at the 2019 fee-based metrics for the companies below, the average is 82% fee-based, with fees accounting for upwards of 85% of many names’ cash streams.

{kind=link}