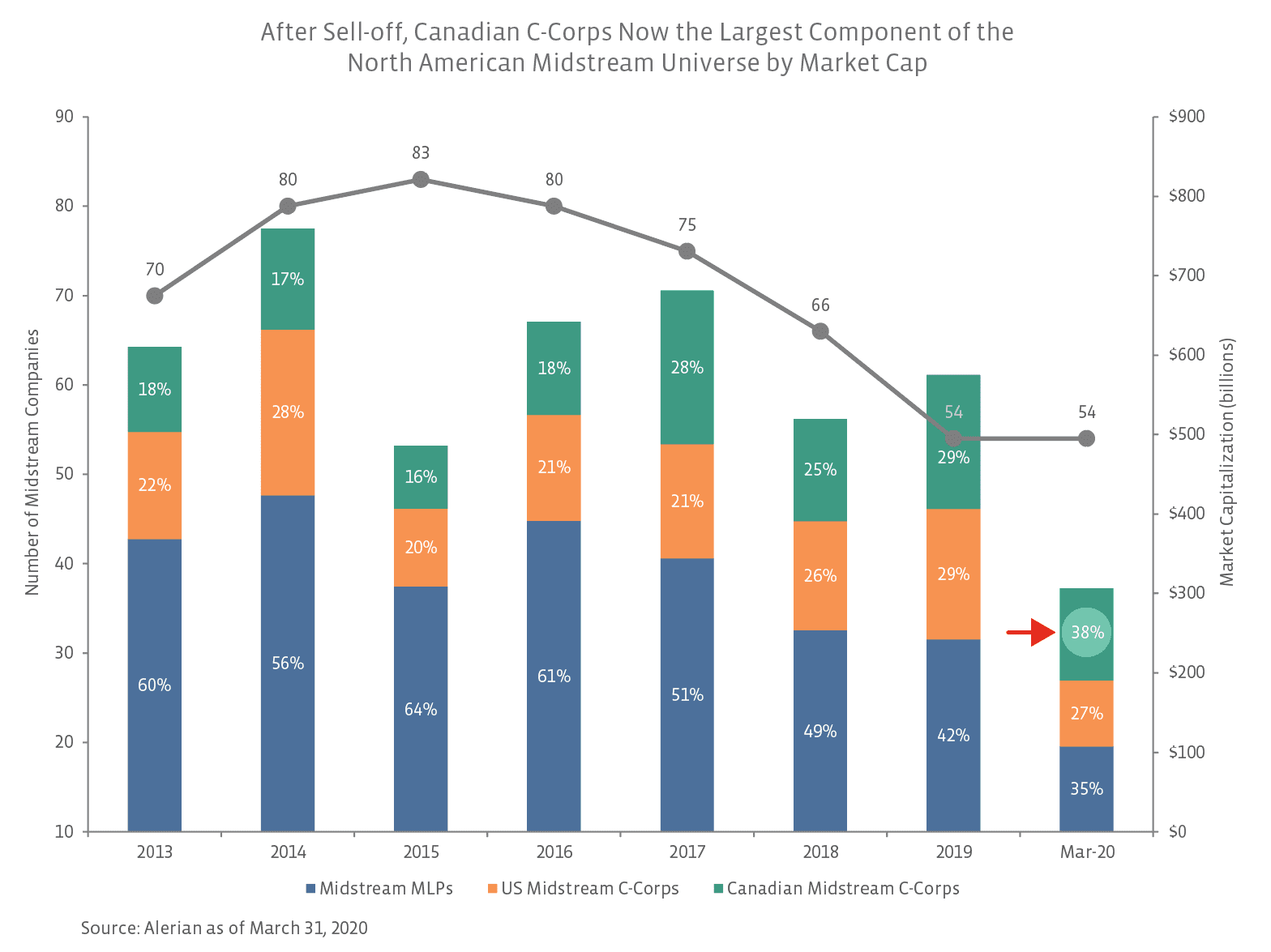

After accounting for the smallest portion of the midstream universe in 2013-16 by market cap, Canadian C-Corps now represent 38% of the universe – more than MLPs at 35% and US C-Corps at 27%. MLPs’ declining share of the midstream market cap has been well documented given the trend of MLP consolidations since 2018 (read more). This has helped US C-Corps gain a greater share and Canadian C-Corps to an extent as well. Recall, Enbridge (ENB) acquired its sponsored MLPs Enbridge Energy Partners and Spectra Energy Partners in December 2018. However, with a static number of companies since year-end 2019, the changes in the first quarter of 2020 largely relate to performance. In addition to the energy and broader market sell-off in March, MLPs were particularly pressured by closed-end funds deleveraging (selling positions to repay debt). With MLPs not widely traded, the added selling pressure in a tough energy tape disproportionately weighed on partnerships, with the Alerian MLP Index (AMZ) declining 58.2% in the first quarter. On the other hand, Canadian midstream names have been resilient. TC Energy (TRP) and ENB were down 9.6% and 20.6% on a price-return basis in the first quarter, respectively, compared to the broad Alerian Midstream Energy Index (AMNA) falling 47.9%. At the end of 2019, ENB and TRP combined to represent 22.9% of the midstream universe by market cap, and on March 31, they accounted for 32.5% of the universe. Stay tuned for a future note discussing more on Canadian midstream performance.

What are the implications of these changes for investors? As discussed in the past, MLPs are not as representative as they used to be and even less representative than just two years ago. For investors allocating to the energy infrastructure space through products, the choice is often between maximizing income (MLP-oriented products) or achieving broad exposure (products with MLPs and corporations). With yields elevated across the space, investors can get healthy yields and broad exposure in products that combine MLPs and C-Corps. For context, the yield of the AMNA Index was 11.3% as of April 3 compared to its five-year average of 6.1%.While midstream market caps will probably continue to fluctuate, Canadian midstream names have clearly become a significant part of the universe, which has performed defensively in a challenging environment.

{kind=link}