Insights at a Glance: Midstream Making the Most of Minimum Volume Commitments

In recent weeks, we have discussed the stability of MLP/midstream cash flows at length by highlighting their underlying fee-based contracts with built-in protections (read more). Protections for the pipeline provider include minimum volume commitments (MVCs), which are intended precisely for the type of challenging macro environment facing midstream today. Disclosures surrounding MVCs, where available, are perhaps the most helpful data points in evaluating cash flow stability, but many investors that are new to the energy infrastructure space may be unfamiliar with how these contract features work. MVCs, which are sometimes referred to as take-or-pay contracts, are agreements in which the customer ensures a minimum amount of throughput and the midstream operator receives a fixed fee per unit of hydrocarbon (i.e. barrel of oil). Under these contracts, the midstream company is owed its fees regardless of whether those volume commitments are actually met. If the volume minimums are not achieved, the customer will be responsible for making a shortfall/deficiency payment for any difference in the actual volumes moved and the MVC. In the current pressured energy environment where producers are slashing spending and dropping rigs, these contracts can be critical to protecting midstream cash flows.

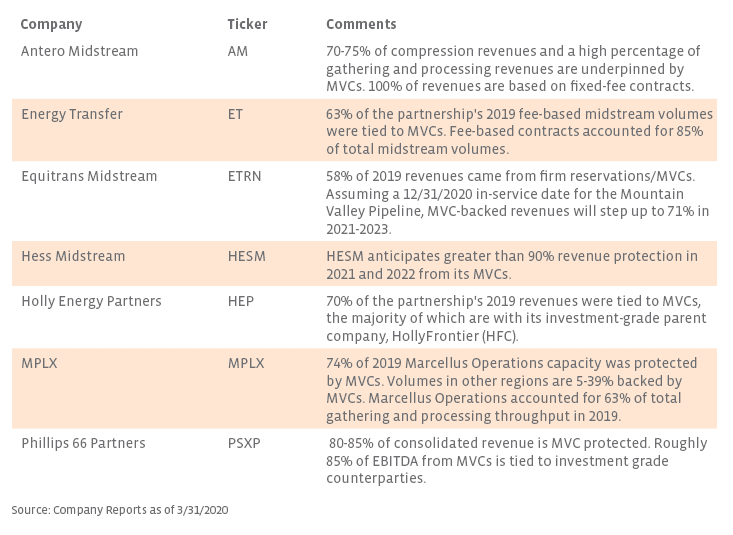

Many midstream MLPs and C-Corps boast take-or-pay contracts with their customers, but fewer companies disclose MVCs as a percentage of revenues or volumes. Often, companies may discuss MVCs for a particular asset, customer, or segment. For example, in announcing plans to build a new pipeline, companies will often say the project is backed by long-term, take-or-pay agreements or describe the capacity as being subscribed and committed. The table below provides a snapshot of MVC commentary for companies that have provided disclosures. A handful of companies have disclosed more than 70% of revenues tied to MVCs. Hess Midstream (HESM) leads the group with forecasted MVC-backed revenues of greater than 90% in 2021 and 2022. Both Energy Transfer (ET) and MPLX (MPLX) break out MVCs as a portion of volumes. MPLX details MVCs by region for its gathering and processing business, with 74% of its capacity backed by MVCs in 2019 in the Marcellus – their biggest region. With production poised to decline in the current price environment, midstream operators will be grateful for the protections provided by MVCs as they support cash flow stability. For their part, investors will likely desire increased disclosure around the portion of projected revenue covered by MVCs.

Links to company materials:

Antero Midstream (AM)

Energy Transfer (ET)

Equitrans Midstream (ETRN)

Hess Midstream (HESM)

Holly Energy Partners (HEP)

MPLX (MPLX)

Phillips 66 Partners (PSXP)

{kind=link}