In a year of significant macro headwinds, midstream has stood apart from the rest of energy for its defensive performance underwritten by the greater cash flow stability of its fee-based business model. As oil and gas producers and oilfield service companies saw their 2020 and 2021 estimates slashed in the wake of the pandemic, the forward outlook for midstream earnings remained steady. Combining resilient cash flows with significant reductions to capital budgets, many midstream companies are anticipating or already generating significant free cash flow and have announced buyback programs as another means of returning cash to shareholders beyond generous dividends. While the energy sector is broadly pursuing free cash flow, investors can have greater confidence in midstream’s ability to deliver free cash flow independent of the oil price level due to the more predictable cash flows of the midstream business. While less directly exposed to commodity prices, midstream still stands to benefit from any potential improvement in the outlook for the global economy and a recovery in oil demand supported by successful deployment of a vaccine.

To better demonstrate midstream’s advantages, the infographic below references the characteristics of the Alerian Midstream Energy Index (AMNA), which is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). The broad-based composite index includes energy infrastructure MLPs, US corporations, and Canadian corporations and is weighted based on float-adjusted market cap with a 10% cap for individual constituents. Unlike other indexes with both MLPs and corporations, AMNA does not limit the weighting of MLPs, providing superior representation of the North American midstream universe. For more detail, please see this index white paper from July 2020.

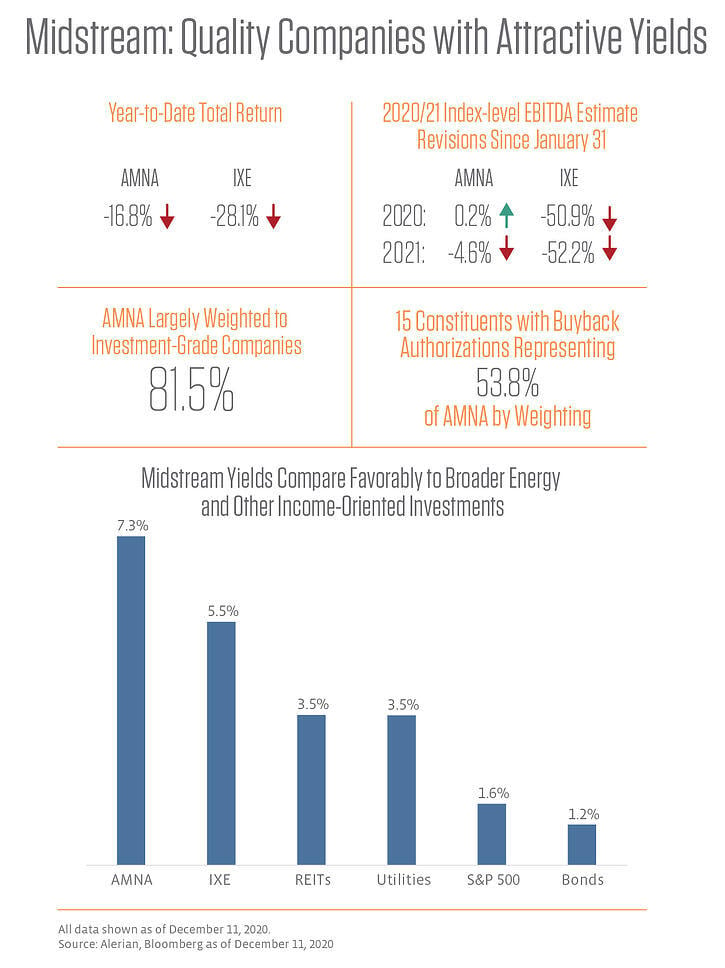

As shown in the infographic below, midstream offers attractive yields from largely quality companies that have performed defensively this year compared to broader energy, represented by the Energy Select Sector Index (IXE). As of December 11, AMNA yielded a more generous 7.3% compared to 5.5% for broader energy. Despite its relative outperformance, midstream has faced selling pressure disproportionate to its modest forward EBITDA revisions. Valuations remain attractive with AMNA trading at 9.9x 2021 EBITDA as of December 11 compared to an average forward EBITDA multiple of 10.9x since inception in June 2018. While the income is attractive, discounted valuations relative to history and the proliferation of buyback programs make for a compelling total return opportunity.