Last summer, we compiled and analyzed a list of all MLPs and their credit ratings. In that article, we talked about how some investors may prefer to invest in those MLPs which are on the cusp of being upgraded to investment grade. This spring however, investors are now trying to avoid those MLPs at risk of losing their investment grade rating.

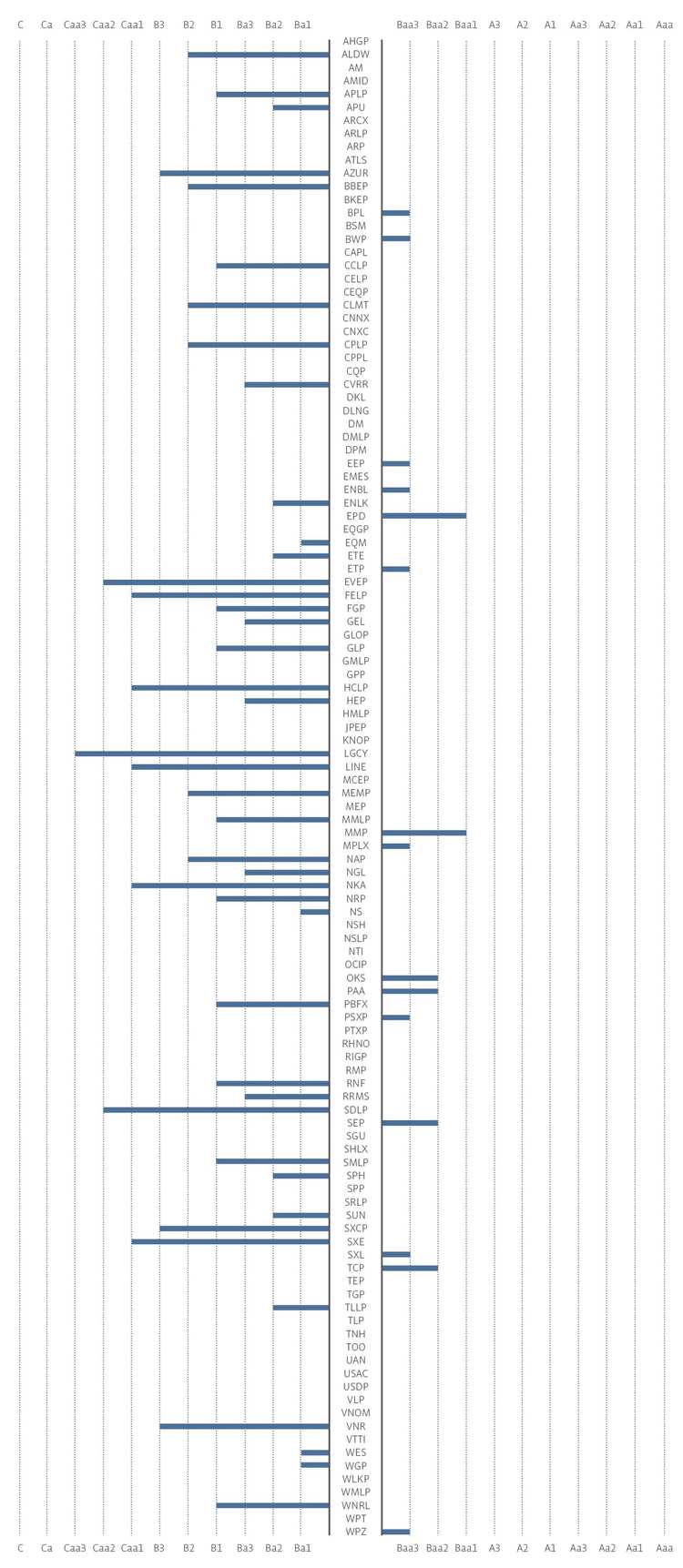

When we last checked in during July of last year, 16 of the 114 MLPs LPs were considered investment grade by Moody’s. Now, that number has changed to 15 of 114. [Please note that these are not the same 114 MLPs. This version includes general partner MLPs which were excluded in the previous version, and several MLPs are no longer trading due to mergers. There were two downgrades from investment grade (explained below), and Sunoco Logistics Partners (SXL), which was previously unrated, is now investment grade.]

Investor Concerns Are Well Founded

I don’t want to belabor any point or company, but as you can read in Moody’s press release, as goes the parent, so goes the MLP. (Think of this like trying to have a parent cosign on child’s first apartment lease. If the parent’s credit is incredibly low, s/he won’t qualify as a cosigner.) When Anadarko Petroleum Corporation (APC) was downgraded, Western Gas Partners (WES) was also downgraded, even though “its stand-alone credit attributes could support a Baa3 rating.” Likewise, thanks to the support of its parent, EQT Midstream (EQM), while not investment grade, has a rating one notch above what it would receive as a standalone company.

The two MLPs that have lost their investment grade rating in the past few quarters include:

(1) EnLink Midstream Partners (ENLK) which was given a negative outlook in December 2015 based on the high price it paid for the Tall Oak acquisition as well as attendant execution risk. The downgrade of two notches in February 2016 was partially due to its basin concentration in the Barnett Shale, but also due to its association with the downgrade of Devon Energy Corporation (DVN), the owner of its parent company, EnLink Midstream (ENLC).

(2) Western Gas Partners (WGP), as mentioned above.

The concerning thing about this chart is not how many MLPs have junk vs investment grade ratings, but how close the investment grade rated companies are to the edge. Last July, nine companies had Baa3 ratings (including ENLK and WGP), and nine companies still have that rating, but the outlook has changed. Before a company is downgraded, Moody’s will often revise its outlook on the company to negative. This happened in December, when Moody’s revised its outlook on Plains All American Pipeline (PAA) (Baa2) to negative from stable, citing a high leverage ratio and low distribution coverage. In January, Williams Partners (WPZ) was downgraded from Baa2 to Baa3, and the outlook remained negative, putting it right on the knife edge.

Protecting the Grade

MLPs which are closest to losing their investment grade rating are likely to do the most to protect it. The poster child here is Kinder Morgan Inc (KMI) [obligatory note: not an MLP] which cut its dividend in order to protect the investment grade rating. As we previously noted, this is an unlikely strategy for MLPs to pursue, but they’ve done just about everything else.

The biggest risk factor for a downgrade seems to be leverage ratios (debt/EBITDA). MLPs have cut and delayed capex budgets in order to avoid taking on more debt. Preferred equity issuance is the newest trend, with the most notable issuance coming from PAA, which raised $1.6 billion selling 8% perpetual convertible preferred units. Not only are public preferred units being offered, but there are also private placements to raise cash. Most recently, WES sold $440 million of convertible preferred unit to First Reserve Advisors and Kayne Anderson Capital Advisors.

Since MLPs have the hallmark of paying significant distributions, selling units raises cash but simultaneously creates a cash obligation. Energy Transfer Equity (ETE), the MLP parent of Energy Transfer Partners (ETP), privately offered existing unitholders the option to forego a portion of distributions for up to nine quarters and instead receive convertible units. Nearly a third of the outstanding units participated in this plan, including the 18% held by Kelcy Warren, the Chairman of the board. This gives ETE cash flow flexibility before it needs it. Management plans to use the newly available cash to repay debt to be incurred with their coming acquisition of The Williams Companies (WMB) “or other transactions to provide financial support to ETP.” This is a great example of why Moody’s evaluates families of companies together. Junk-rated ETE is already prepared to protect investment-grade rated ETP.

Again, the Kinder-cut seems to be the protection of last resort.

The Approaching Barbell

As we see more distribution cuts, ratings outlooks change to negative, and actual downgrades, fewer and fewer MLPs will be able to access the capital markets. Reduced access to capital makes future growth even harder.

In the past year, over a dozen non-investment grade MLPs had their ratings reduced even further. Seven of the junk rated MLPs have ratings at or below Ca1; last year that number was only one. The list reads like an unfortunate who’s who of commodity sensitive small-cap MLPs.

By and large, however, investment grade energy MLPs retained their investment grade rating and have still been able to issue debt. (For instance, Magellan Midstream Partners (MMP) issued $650 million of 10-year notes at 5.0% just last month.) Since the capital markets are still open to these companies, they will be at the table when the junk-rated MLPs sell assets desperate to raise cash. As this environment continues, we’ll see an even greater divide between the haves and the have-nots.

{kind=link}