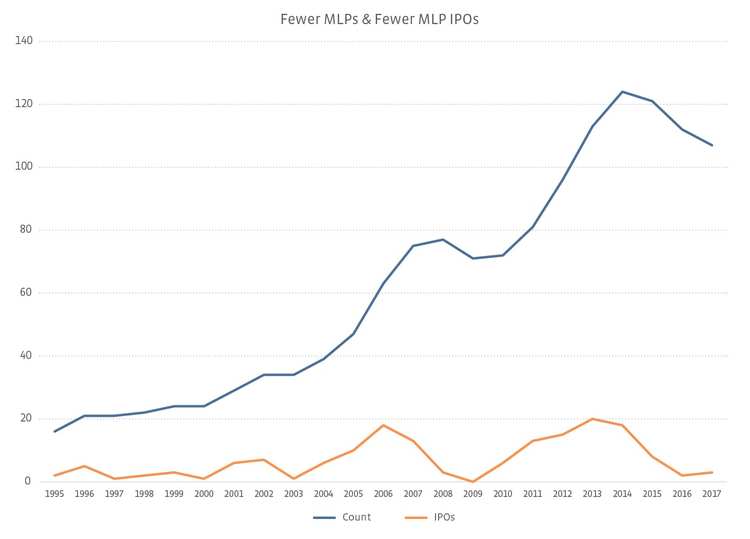

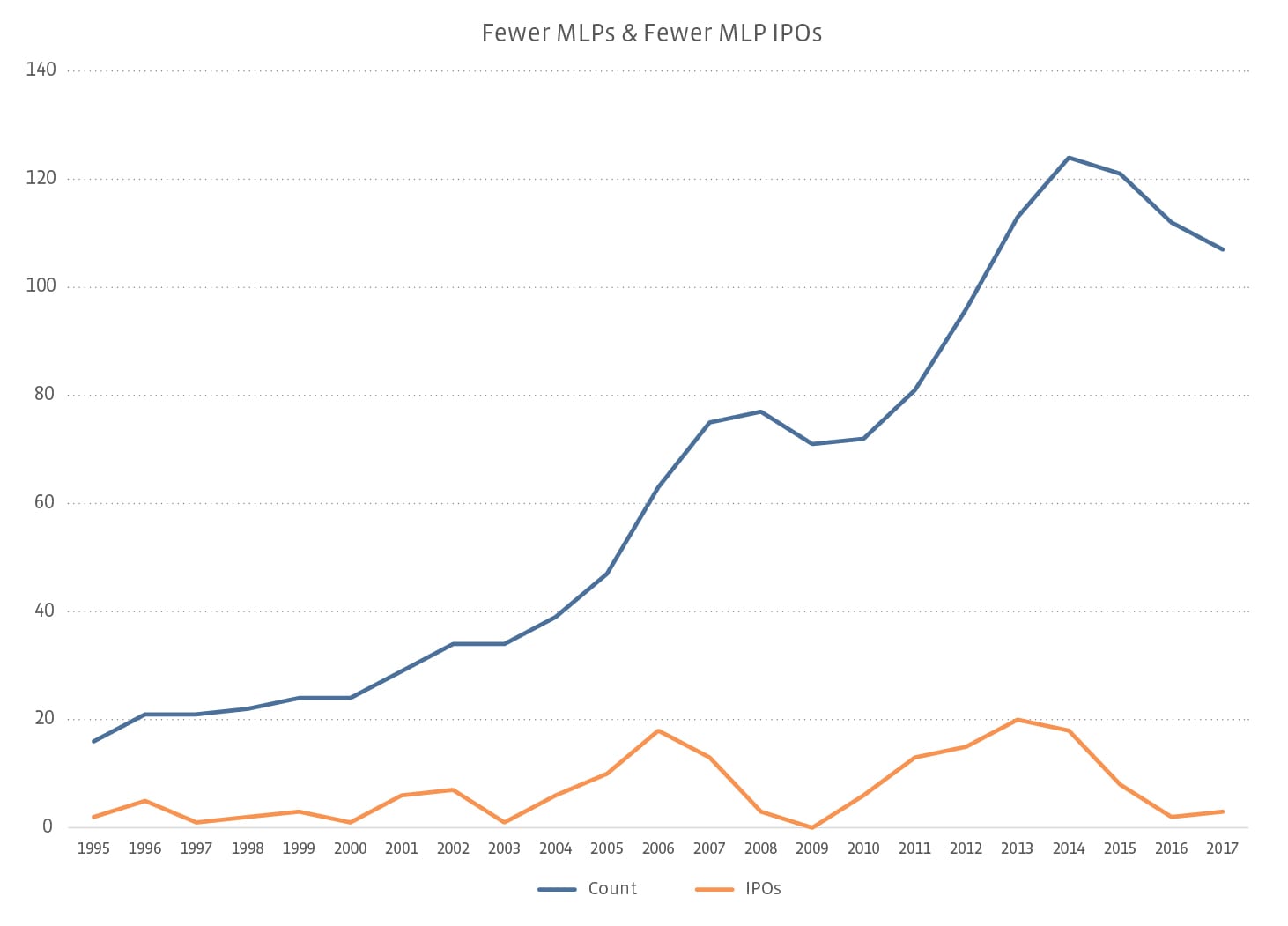

On the one hand, the changes of the past few years can be understood as nothing more than the growing pains of any industry as it matures (which we’ll explore with help from the Harvard business review). After all, the original thesis is intact and profitable, and the industry still has government support. On the other hand, it would be foolish to discount the loss of three major MLPs that had significant market cap. What differentiates those MLPs with limited lifespans from those with staying power?

Original Thesis Still Relevant

One of the first arguments made for the value and expansion of the MLP was that it was just common sense for large energy companies to spin off their midstream assets into an MLP. In short, it would transform an internal cost of doing business into a profit center. This is precisely what Hess Corporation (HESS) did—spinning off its midstream assets into Hess Midstream Partners (HESM) in an IPO just this year that was oversubscribed and priced above the range. And just last month, BP (BP) announced the same thing, potentially raising cash while maintaining access to the assets. Analysts are even speculating that Chevron might try the same thing.

Governmental Support

Since MLPs were created by Congress and are defined by the IRS, it makes sense to follow the government’s lead on this. The folks at the (underfunded, overworked) IRS have taken the time not only to issue new qualifying regulations, they have also issued a number of PLRs in the past few months. My colleague Karyl Patredis goes into further detail on this, but notably, the IRS is still willing to spend its time on this industry.

The Building of MLP Empires

For those of us who didn’t go to business school, this Harvard Business Review article is a great explanation of how an industry moves through a cycle of expansion and consolidation as it matures. MLPs and energy infrastructure are solidly in stage two: Building Scale, also defined as

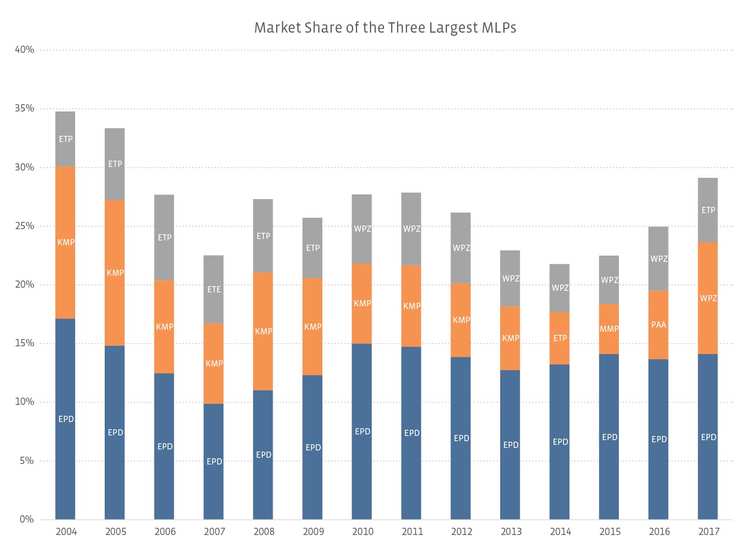

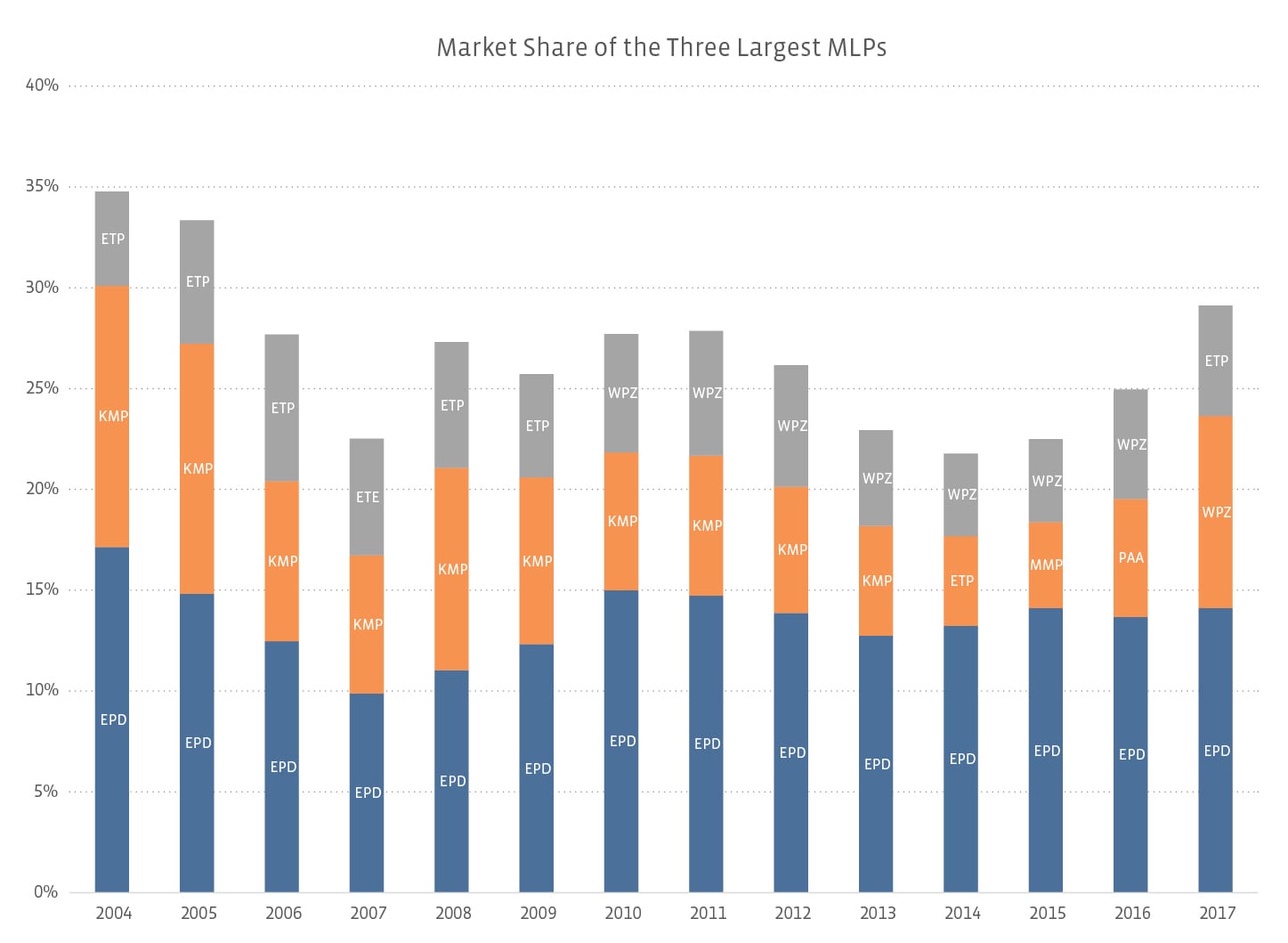

Major players begin to emerge, buying up competitors and forming empires. The top three players in a stage 2 industry will own 15% to 45% of their market, as the industry consolidates rapidly.

The three largest players in MLPs today are: Enterprise Products Partners (EPD), Williams Partners (WPZ), and Energy Transfer Partners (ETP). These names will be familiar to you not just due to their size, but also because of their consolidation efforts.

In 2004, EPD began building its empire with its purchase of Gulf Terra Midstream (former ticker: GTM). The 2009 merger with TEPPCO Partners (former ticker: TPP) cemented its position as the largest MLP. Since then, it has grown through other acquisitions, organic growth, and joint ventures with other major MLPs. (For further details of their growth history, please see the interactive history section on their website.) Unlike the MLPs who have converted to other structures, EPD long ago (2010) bought out its own general partner (Enterprise GP Holdings, former ticker: EPE) as well as the associated IDRs. The following year, it simplified further by buying in Duncan Energy Partners (former ticker: DEP).

Flies in the Ointment

The Fatal Handicaps

Due to its simplification nearly a decade ago, EPD sees no need to abandon the structure. But other companies who built infrastructure empires have found that they only had a limited lifespan as an MLP with IDRs. Kinder Morgan Inc (KMI) is, of course, the popular example of this. However, much more recently, the ONEOK and Targa families of companies have followed suit. Their MLPs have been absorbed into the C corp parent.

Being relieved of the burden of IDRs lowers an MLP’s cost of capital, making it more competitive both in any further consolidation, and in pursuing growth opportunities. Given the limited set of new pipelines to be built in this commodity environment, with the Permian a lone bright spot of opportunity, cost of capital matters now more than ever.

(Since I know there’s always a request for names that don’t have an IDR burden: If you’re looking for large cap MLPs without IDRs (or a general partner with a non-economic interest), a starter list would include: EPD, as previously mentioned, Magellan Midstream Partners (MMP), Genesis Energy (GEL), and Buckeye Products Partners (BPL).

The other major drawback to the traditional MLP structure is a much smaller investor base. Filing Schedules K-1s is about as popular as getting a root canal, for starters. But then there’s the loss of the money tied to the S&P 500 and other total stock market indices too. The best hope for maintaining the structure on this front might be those MLPs with tracking stocks, where one C corp share owns one MLP unit. That way, investors can get exposure to the MLP without needing to deal with a K-1.

(Again, since I know people will want examples. Check out Plains GP Holdings (PAGP) and Cheniere Energy Partners LP Holdings (CQH). Less pure exposure (and therefor more research required) can be found with Enbridge Energy Management (EEQ) and Williams (WMB).)

Final Thought

When Kinder first left the MLP space, it was an anomaly. Now that it has been joined by two more as ONEOK Inc (OKE) and Targa Resources Corp (TRGP) have both also bought in their MLPs, there is validity to the question of whether the MLP model is still relevant. The continuation of IPOs proves that investor interest still remains; however, the industry itself needs to remain cognizant that minimizing an MLP’s IDR burden (or lowering its cost of capital in other ways) and maximizing an MLP’s investor base may be needed to extend an MLP’s lifespan beyond 15-20 years.

{kind=link}

{kind=link}