Investors often ask us if the US is over-piped. The question points to two concerns. First, will an overbuild of pipelines cause headwinds for the MLP space in the form of re-contracting risk? Second, are there still pipeline growth opportunities in this space? In today’s post, we’ll tackle the first concern around re-contracting risk, and we’ll address the second question next week.

MLPs and corporations generally don’t build pipelines without firm long-term commitments for most of the line’s capacity that underwrite a reasonable return on the project. These commitments provide cash flow visibility and are critical for determining if a pipeline will be built. Recent examples include TransCanada’s (TRP) announcement to begin construction preparation for Keystone XL with ~500,000 barrels per day of 20-year commitments (~60% of expected capacity) and the joint venture Gulf Coast Express pipeline, which had ~85% of capacity committed when the decision was announced to move forward with the project.

This conservative approach by the industry should help prevent the overbuild of pipelines. That said, market dynamics can change over the course of the contract’s life and when long-term commitments expire, the customer can choose to enter a new agreement or not. If there is less production or multiple pipeline options, competition could drive lower shipping rates than what the MLP enjoyed previously or leave the MLP with unused capacity. This is what re-contracting risk is all about. Below, we discuss a few considerations around MLP re-contracting risk, but note that exposure to this risk will vary by MLP.

Timing

Commitments for pipeline capacity can vary from 3 to 15 years (or even longer), and customers on the same pipeline may have different contract terms. Because pipelines start up at different times with different contract lengths, contract expirations should generally be staggered over time for each company, which helps mitigate re-contracting risk for the individual MLP. On a broader level, investment in an MLP access product that owns a variety of MLPs should provide further protection from re-contracting risk, given the diversity of assets represented in the portfolio.

Location, Location, Location

The location of the pipeline in terms of the producing region it serves is also an important consideration when it comes to re-contracting. If production has fallen in the region or the economics for producers are less attractive, re-contracting risk is more likely for both gathering and takeaway pipelines. Generally, we’ve seen restructuring of contracts in the gassy plays that kickstarted the shale revolution. Examples include:

-

Boardwalk Pipeline Partners’ (BWP) restructuring with Southwestern Energy (SWN) in the Fayetteville

-

Crestwood Equity Partners (CEQP) and Williams Partners (WPZ) restructuring with Chesapeake Energy (CHK) in the Powder River Basin

- WPZ’s restructuring with CHK in the Barnett and Mid-Continent, with Total (TOT) ultimately assuming the Barnett agreement as CHK’s successor

- WPZ’s restructuring with CHK in the Haynesville

These restructurings broadly resulted in a better alignment of incentives between the producer and midstream provider, with contracts significantly extended (more than 10 years), albeit at a lower rate. The silver-lining is cash flow visibility for years and years.

Destinations and Origins

The destination and origin of point-to-point pipelines are also important factors when it comes to re-contracting risk. A refiner customer needs to get hydrocarbons to a specific refinery and then move refined products from that refinery to end markets. A refinery may only have a few pipeline options for sourcing crude and moving refined product. As an example, CVR Refining (CVRR) had to reduce production at its Coffeyville, Kansas, refinery in 2016 due to a temporary outage on one of three product pipelines used to transport products from the refinery. There wasn’t an alternative pipeline to move the product. Similarly, a utility needs to get natural gas to a specific power plant. Niche pipelines serving a specific asset are less likely to face competition in the form of new pipelines and re-contracting risk related to changes in demand for the pipeline, as long as the asset remains in operation.

Competition – Permian Example

Competition can also lead to increased re-contracting risk, particularly for pipelines providing takeaway from a producing region to an end market where the customer may have more flexibility among pipeline options. The Permian today is a prime example, with several new crude pipelines proposed and expansions underway. The EPIC crude pipeline and Plains All American’s (PAA) Cactus II Pipeline have sufficient commitments to proceed and are expected online in 2019. BridgeTex is expanding by another 40 Mbpd having recently expanded to 400 Mbpd. Enterprise Product Partners (EPD)’s Midland-to-Sealy pipeline may be able to transport up to 550 Mbpd of crude with the use of drag reducing agents compared to the nameplate capacity of 450 Mbpd.

Existing pipelines are feeling the competitive pressure. Magellan Midstream Partners’ (MMP) financial guidance assumes volumes on its Longhorn pipeline will be maintained at historical levels once contracts expire in 4Q2018 but at lower tariff rates due to heightened competition. The new committed rates on BridgeTex, jointly owned by MMP and PAA, are likely a good indication of the market, with a rate of $1.85/bbl from Colorado City to East Houston for a volume commitment of 10-40 Mbpd for a three-year term. In 2016, BridgeTex had filed tariffs for similar volumes at rates of $4.02/bbl for a seven-year commitment.

Headlines of lower rates are negative for the sector; however, there is something to be said for volumes remaining stable and having visibility on cash flows — even if it is at a lower rate. Uncommitted capacity could provide upside for pipeline operators if Midland prices again become significantly discounted relative to Houston prices. MMP guided to up to $30 million of incremental distributable cash flow in 2018 if uncommitted capacity is used on both Longhorn and BridgeTex. (See this post from December 2017 for an explanation of how crude spreads can impact uncommitted tariff rates.) The futures curve points to widened discounts between WTI Midland and WTI Cushing in late 2018 to early 2019, likely reflecting the potential for takeaway capacity to be constrained ahead of the start-up of EPIC and Cactus II. Crude spreads are dynamic, and while lower rates are a concern today, there could be flexibility to raise rates in the future, pending regulatory approval.

Counterparties Matter

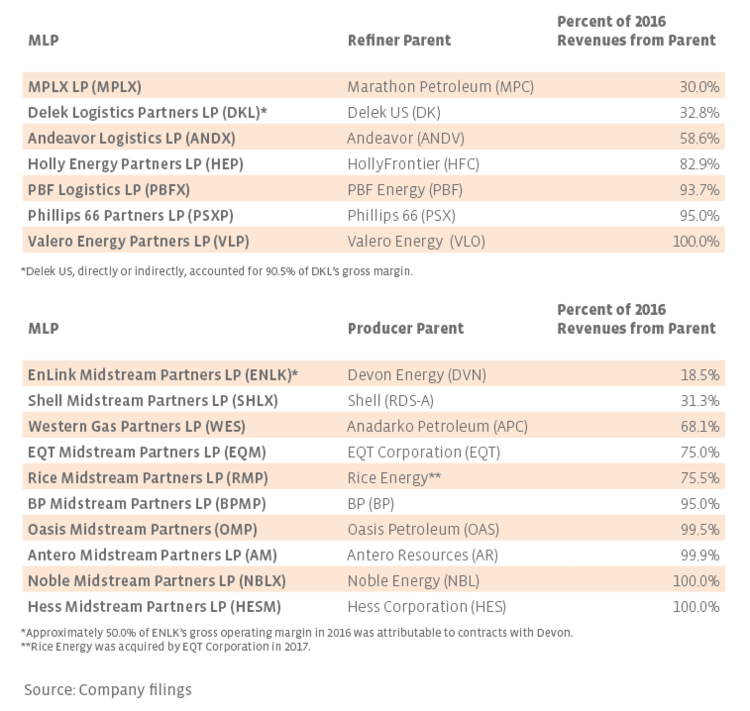

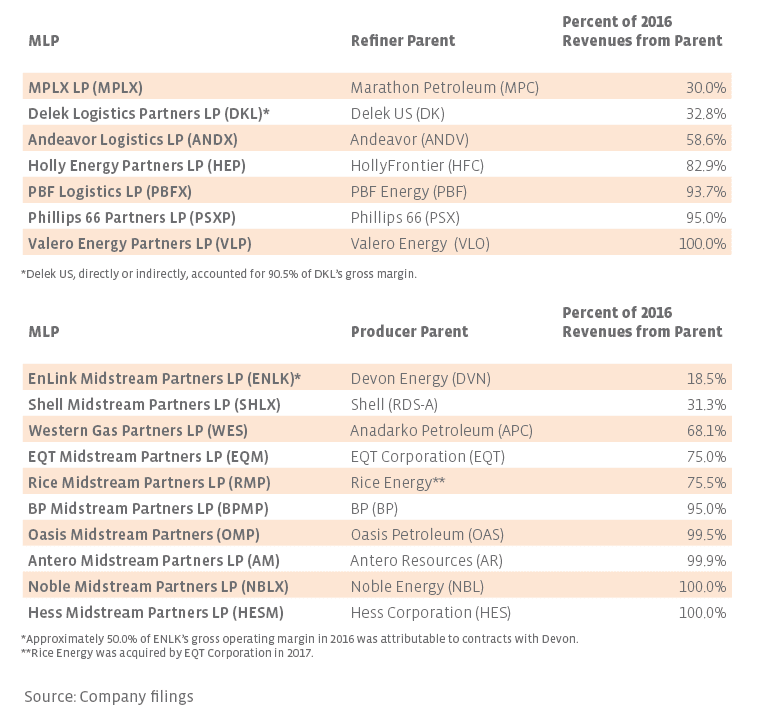

An MLP with a refiner or producer parent as its primary customer is more protected from re-contracting risk than an MLP dependent on unrelated third parties. The parent, which likely owns a significant LP interest, isn’t going to seek out another provider. Contrarians may argue that a lack of third-party revenues for MLPs can be viewed as a negative in the sense that the MLP may be too dependent on a parent and the parent’s financial wellbeing; however, from a re-contracting risk standpoint, it’s likely a positive. Below are several examples of MLPs with refiner or producer parents and an indication of their dependence on their parent based on 2016 revenues.

While we’ve provided some broad thoughts for the MLP sector in general, re-contracting risk will ultimately depend on the individual MLP and the contract terms for its pipeline assets. Information in the MLP’s 10-K can provide helpful context around existing contracts and their expiration. Stay tuned for next week’s post, as we discuss growth opportunities in the space and whether the US is over-piped.

{kind=link}