Rocky Mountain NGLs — ONEOK (OKE) is building a new NGL pipeline from Montana to existing NGL facilities in Kansas to address current pipeline constraints. Production of gas and NGLs in the Bakken and Niobrara has grown along with the growth in crude production, which is now at record highs, and producers require an outlet for the gas and NGLs produced. In announcing the Elk Creek Pipeline, ONEOK noted that the two existing pipelines serving the region, Bakken NGL Pipeline and Overland Pass Pipeline, are operating at full capacity.

Canadian crude — Canada is obviously not part of the US, but the US is an important end-market for Canadian crude. Western Canadian Select crude is currently trading ~$28 per barrel below WTI compared to an average discount of $12.75 per barrel in 2017. The wider discount is largely due to takeaway constraints that were further exacerbated by the downtime for the Keystone pipeline, which was still operating at reduced rates as of late January following a November leak. The ramping of the Fort Hills oil sands project may further exacerbate pipeline constraints.

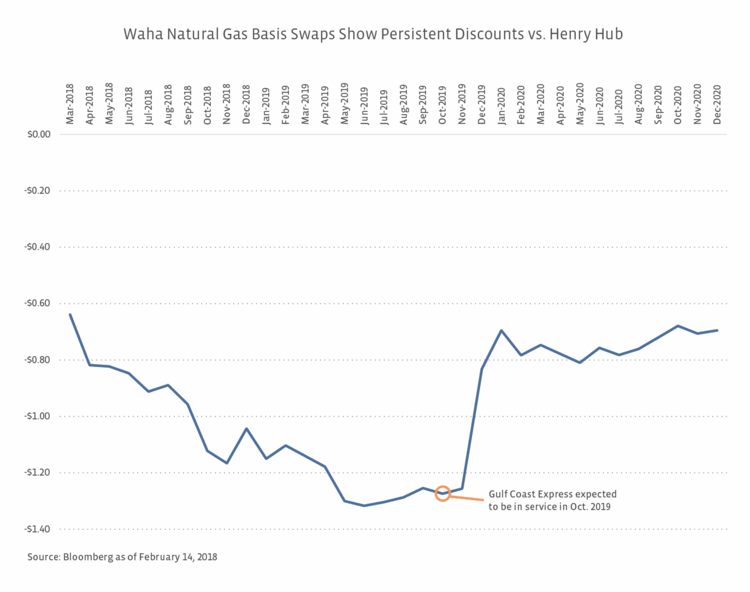

Canadian gas —Again, Canadian gas is linked to the US through exports. Production growth in Alberta has largely outpaced demand and takeaway capacity, forcing producers to grapple with limited options to market their product. The benchmark gas price in Alberta briefly turned negative in October 2017 coinciding with pipeline maintenance and already elevated storage levels. While prices have recovered to ~$1.60 per MMBtu, prices are still ~$1 per MMBtu below Henry Hub and inadequate transportation capacity is likely to remain a near-term challenge. TransCanada (TRP) has been working on an expansion of its NGTL System that transports natural gas in Alberta and British Columbia. The larger NGTL System expansion that will increase capacity by 1.0 Bcf/d is expected to begin service in November 2020 and April 2021.

While these are all examples of areas that are currently pipeline constrained, this list is not exhaustive, and there are certainly pipeline opportunities outside of these regions. For example, earlier this month, Tallgrass Energy Partners (TEP) and Silver Creek Midstream announced a new pipeline project connecting the Powder River Basin with the Guernsey, WY, oil hub. Several Permian crude pipeline projects have been announced in anticipation of future constraints as production grows. In short, there are still opportunities to build new pipelines, but it’s important to note that pipelines aren’t the only means for MLPs to grow.

Growth doesn’t have to depend on new pipelines.

Competition in the midstream space has undeniably increased. There are more players, including MLPs, utilities, and private equity companies, competing for pipeline projects. As a result, we’re seeing more joint ventures among MLPs and other energy players when it comes to projects — pipelines or otherwise. Joint ventures can be beneficial in that costs and risks are shared among partners, though cash flows are also shared.

Setting aside newbuild pipeline projects, growth can come from expanding existing pipelines or by acquiring pipelines. Pipeline expansions are a relatively easy way to grow volumes and can be implemented as production growth necessitates additional capacity. Acquiring pipelines or other assets that fit within an existing geographical footprint can also be an attractive option for growth. The private equity companies that are competing with MLPs today may be selling assets in the future to exit asset-level investments, providing a potential opportunity for MLPs to acquire assets.

We’re also seeing a focus on growth opportunities that aren’t pipeline-related. Gas processing, fractionation, petrochemical projects, refining units, marine terminals, and export-related projects are just some of the alternative options for MLPs to grow. EPD has further expanded into petrochemicals with a PDH facility that produces propylene and an iBDH facility that produces butylene. EPD is also building an ethylene export terminal in partnership with Navigator Holdings (NVGS). Drop downs from refiner parents have started to include specific refinery processing units. Examples include Holly Energy Partners’ (HEP) purchase of certain units at the Woods Cross Refinery and Phillips 66 Partners (PSXP) purchase of processing units at the Sweeny Refinery. Magellan Midstream Partners (MMP) is expanding its Seabrook Logistics joint venture (Houston area), adding dock capacity at its Galena Park marine terminal, and partnering with Valero Energy (VLO) to expand the Pasadena marine terminal.

If you still think MLPs need to build new pipelines to grow, consider MPLX (MPLX), which is guiding to distribution growth of 10% in 2018. MPLX plans to spend $2.2 billion in growth capital in 2018 on gas processing plants, fractionation capacity, a butane cavern, tank expansions, expanding its marine fleet and expanding export capacity at the Galveston Bay refinery. There is no allocation for building new long-haul pipelines, and only a small portion of the budget (less than 15%) is allocated to expanding existing pipelines. Admittedly, MPLX is classified as a Gathering & Processing MLP under the Energy MLP Classification Standard (EMCSSM), but that has not precluded MPLX from participating in major new pipeline projects (the Bakken Pipeline System) and building new pipelines (Cornerstone Pipeline). MPLX exemplifies the fact that MLPs do not have to depend on new pipelines to grow.

Bottom line

The US is not over-piped. Multiple producing regions still face pipeline constraints, and we continue to see announcements for new pipelines with sufficient long-term capacity commitments to justify construction. There is admittedly intense competition in the space, which has resulted in more joint ventures across projects. If oil prices stay at these levels, US oil production is likely to continue growing. Natural gas and NGL production should also grow as northeast pipeline bottlenecks are alleviated and as associated gas production increases. Continued production growth could lead to future capacity constraints that require newbuild pipelines, but nowadays, pipelines are just one of many ways that MLPs can grow.

{kind=link}