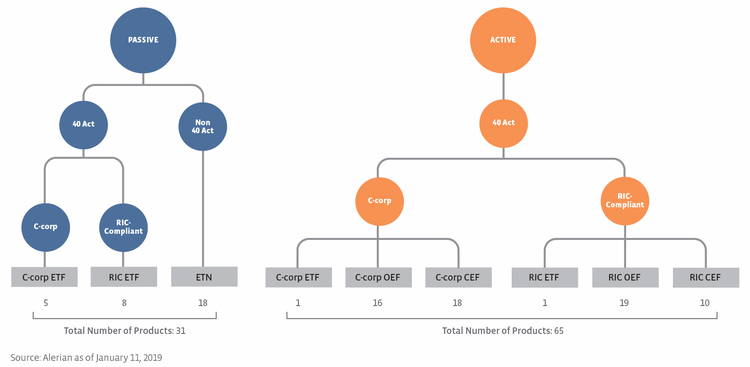

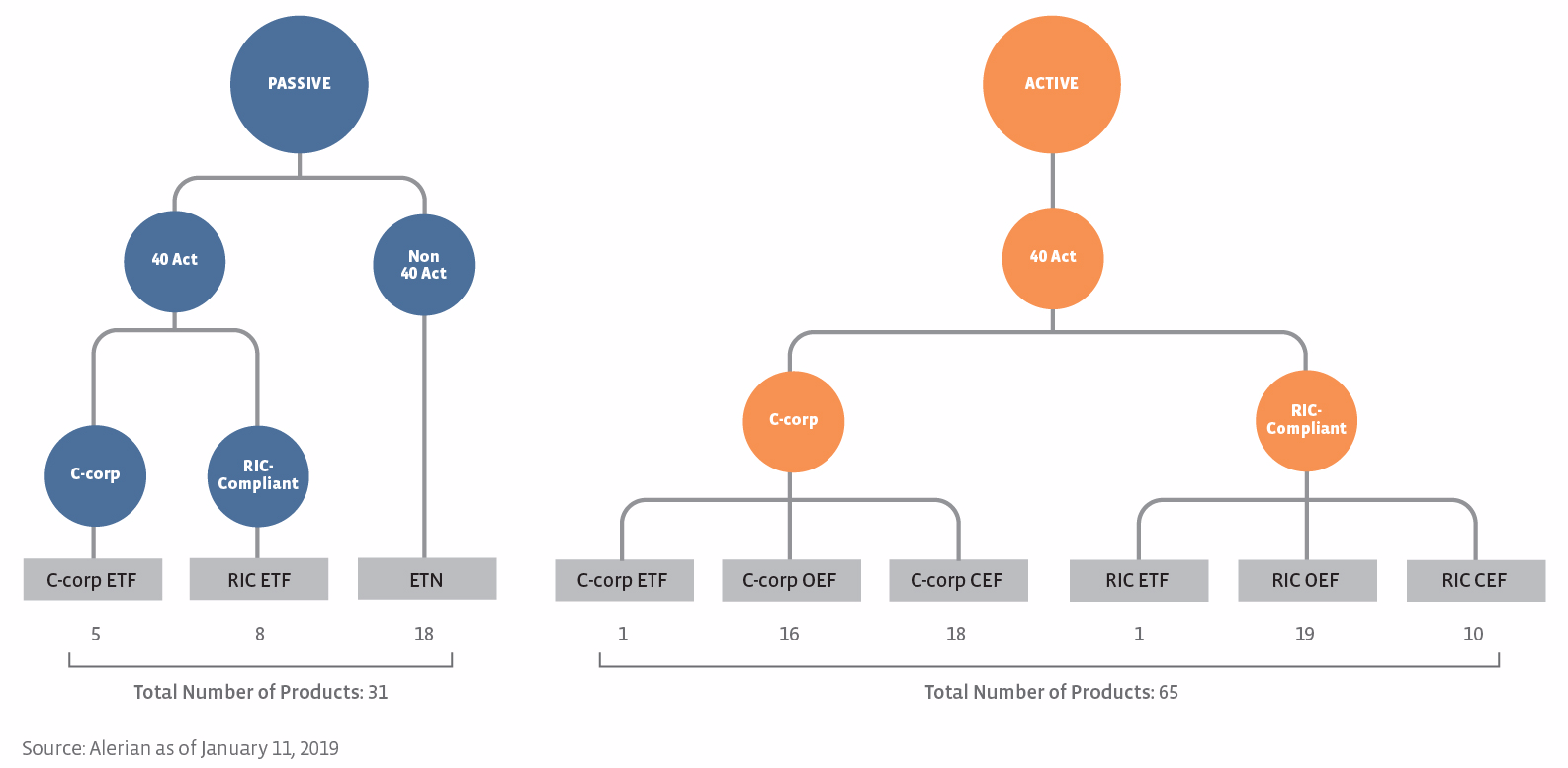

C-Corp funds – Any OEF or mutual fund, CEF, or ETF that owns more than 25% MLPs will be taxed as a corporation. The result is a tax drag, which will cause performance of the fund to differ from the performance of the underlying securities or the underlying index for passive products. As the underlying securities experience gains, C-Corp funds will accrue a deferred tax liability to account for corporate and state taxes. With the lowered corporate tax rate of 21%, tax drag going forward should be more muted relative to the 35% rate in place prior to the recent tax reform. The primary attraction of C-Corp funds is the yield they provide, given the significant MLP weighting.

RIC-compliant funds – Funds that own less than 25% MLPs will not pay taxes at the fund level, allowing the entire return to be passed on to investors. In other words, RIC-compliant funds have no tax drag. There are other nuances to keep in mind, however. RIC-compliant funds have lower yields relative to C-Corp funds because of their lower MLP weighting. It’s also important to understand the holdings of the other 75% of a RIC-compliant fund and to make sure the exposure in the fund is what you want.

Exchange Traded Notes (ETNs) – Unlike C-Corp or RIC-compliant funds, ETNs are unsecured debt obligations of the issuing bank, and holders of ETNs are exposed to the credit risk of the issuer. The issuing bank agrees to pay the investor a return as specified in the issuance documents. MLP ETNs can track a basket of MLPs without any tax drag, but as notes, coupons are taxed at ordinary income rates. For this reason, as we discuss below, ETNs are more suitable for tax-advantaged accounts.

Which product makes the most sense for me?

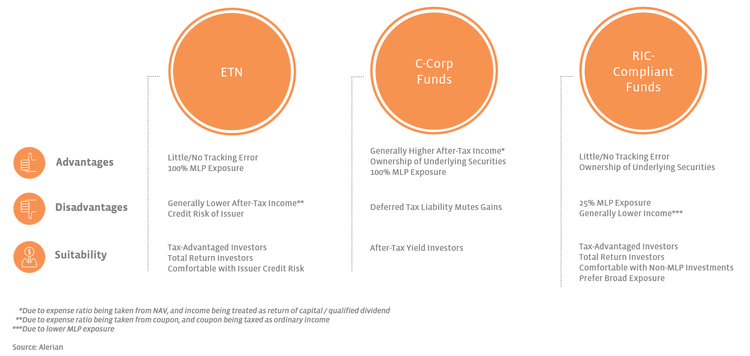

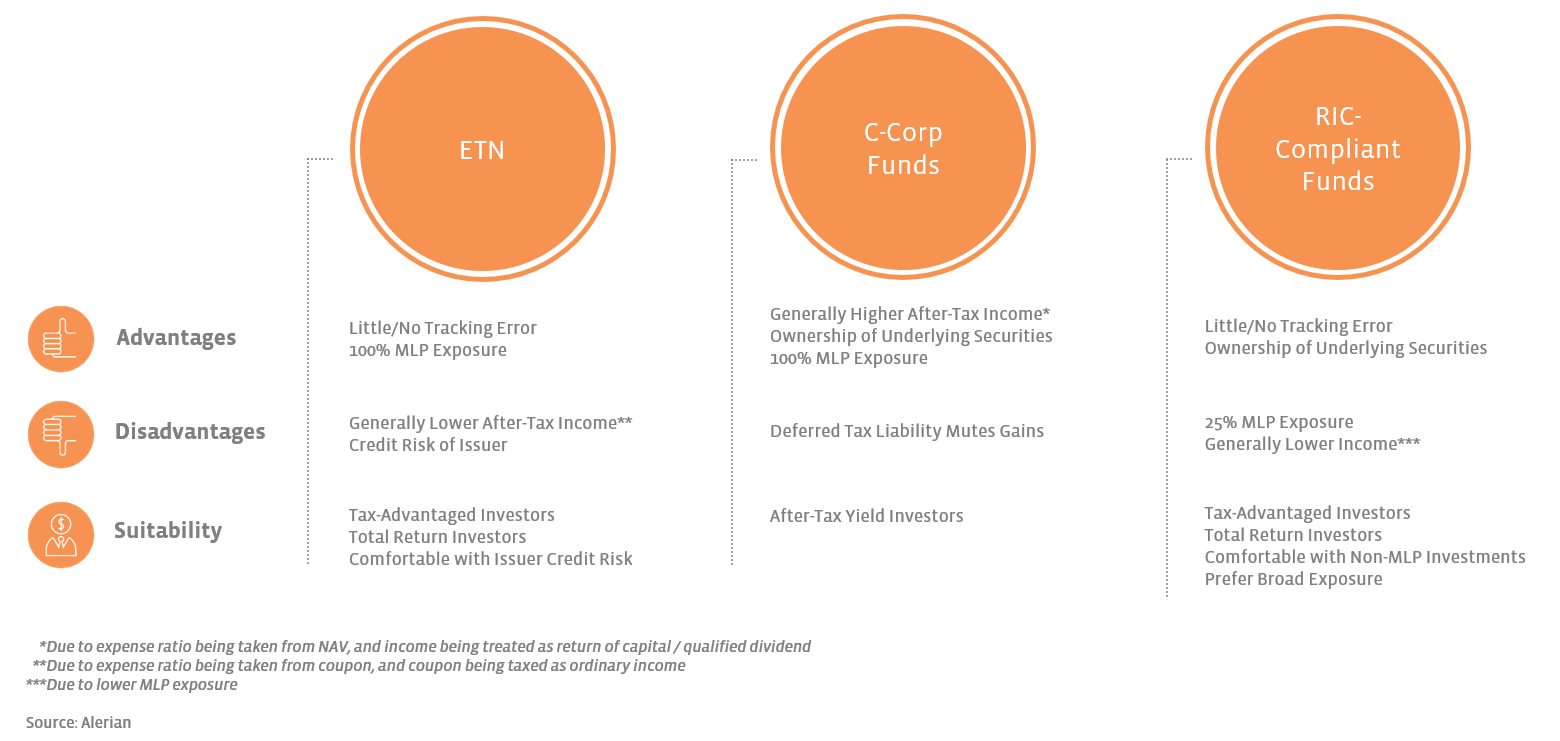

To figure out which product makes the most sense for you, there are a few considerations to keep in mind. For example, is the account where you will own the product taxable or tax-advantaged? What are you mostly looking for from your investment – yield, total-return, broad exposure? What is your expectation for MLP/midstream performance? The graphic below largely addresses these questions by covering the advantages, disadvantages, and suitability of ETNs, C-Corp funds, and RIC-compliant funds. We should also mention that you don’t need to worry about Unrelated Business Income Tax if investing in these products in a tax-advantaged account (read more about owning an MLP ETF in an IRA).

To further clarify, we would add that if you expect MLPs and midstream to see significant price gains, then you are probably going to be more interested in a RIC-compliant fund or an ETN to fully participate in price appreciation. An MLP ETN would give exposure to MLPs but comes with the credit risk of the issuer and is better suited to a tax-advantaged account. A RIC-compliant fund will provide less than 25% MLP exposure, and you will want to make sure the rest of the fund holdings provide the desired exposure.

If you are primarily wanting yield, then you will be more interested in a C-Corp fund as these funds tend to provide higher after-tax income. If you are looking for broad exposure to the midstream space, an MLP-only fund is not as representative as it used to be given recent MLP consolidations. We most recently addressed this topic in a December post (read more), but we also discussed this in more detail in August 2018 (read more). When it comes to investing in energy infrastructure, investors have to choose between yield and broad representation.

Bottom Line

Last week, we summed up the MLP and midstream investment thesis in a sentence with four points. The same cannot be done for MLP investment product options. There are many nuances to take into consideration based on an investor’s preferences for returns (yield vs. total return), desire for broad exposure, tax considerations, and even appetite for credit risk.

{kind=link}

{kind=link}