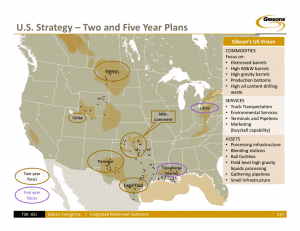

US investors in Kinder Morgan (KMI) and Plains All American Pipeline (PAA), among others, are probably familiar with the fact that their investment isn’t just in domestic energy infrastructure assets, but in Canadian ones as well. But they may be less aware that Canadian midstream companies are also extending their reach beyond national borders. GEI entered the US market with acquisitions in 2010 and 2012, and now provides environmental services and fluid handling, crude oil and NGL hauling, and production services solutions. But management isn’t done yet. In the first slide, it’s clear that GEI isn’t just waiting for deals to come its way; management has outlined two- and five-year plans for its US operations by both geography and activity.

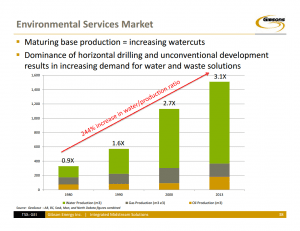

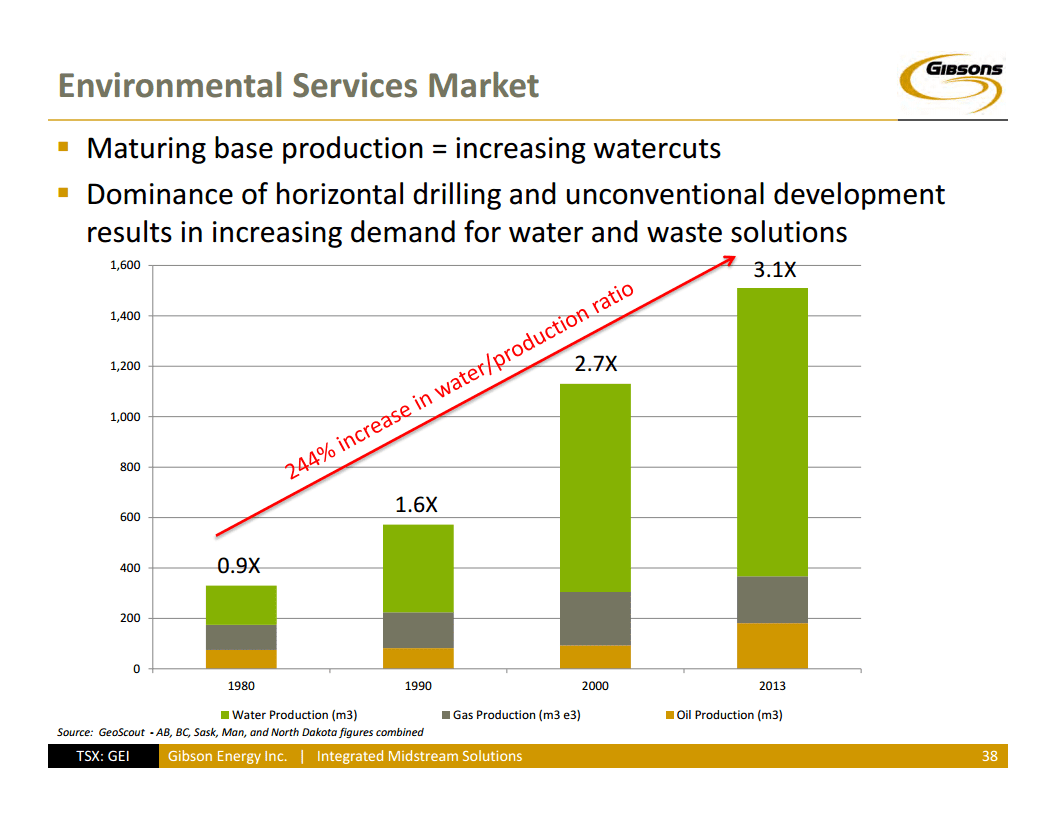

So why bother getting involved in the US? Consolidation of the highly fragmented environmental services market appears to be one good reason. Referencing Wood Mackenzie, GEI notes that produced water and associated waste stream are expected to grow at a 5%-15% CAGR through 2020 in the Permian, Niobrara, Williston, Northeast, and Mid-Continent. These volume increases are due to the development of unconventional plays, the increase in horizontal drilling, and maturing base production, leading the ratio of water to production to increase to 3.1 in 2013 from 0.9 in 1980. If oil production continues to grow, then so will the volume of produced water and the need to deal with it.

Inter Pipeline (slide presentation here)

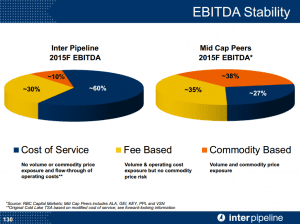

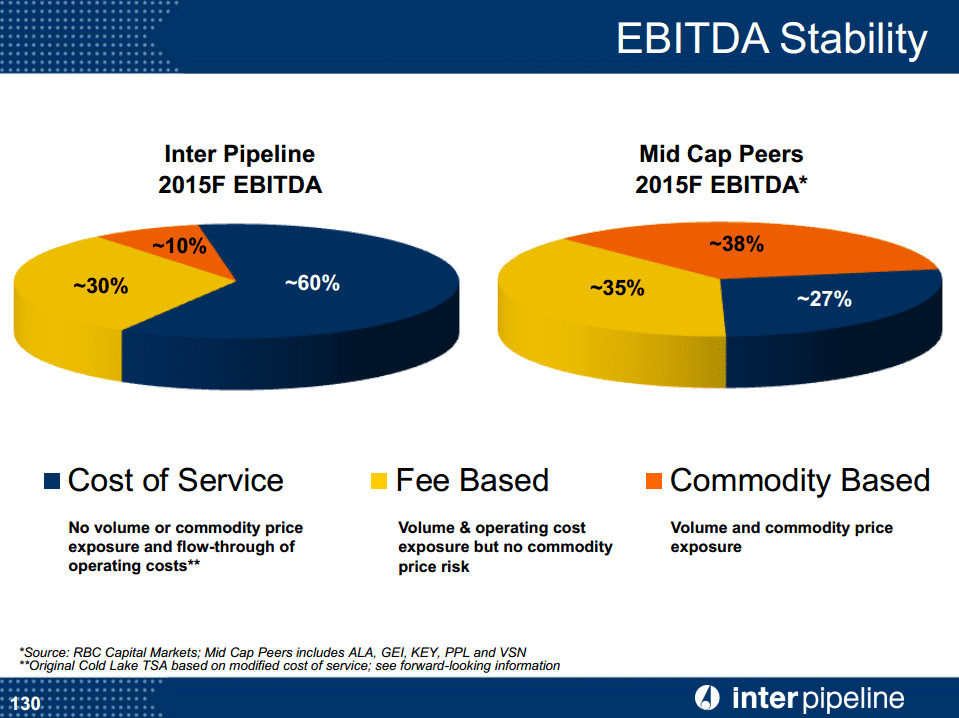

In case you haven’t grown tired of talking about commodity prices, I’ll first quickly point out that IPL sources the Alberta Energy Regulator in noting that economic recovery in the Canadian oil sands and conventional Canadian oil plays requires a WTI price of $55-$110 and $50-$75, respectively. So why hasn’t IPL’s stock price suffered alongside oil prices over the past seven months? The slide on the left. 60% of its 2015E EBITDA comes from cost-of-service contracts, which have neither price nor volumetric risk. Few US midstream assets have similar contracts, which limit both upside and downside even more than fee-based contracts do.

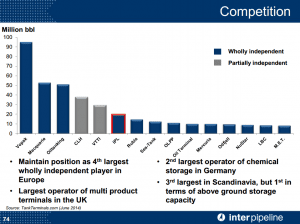

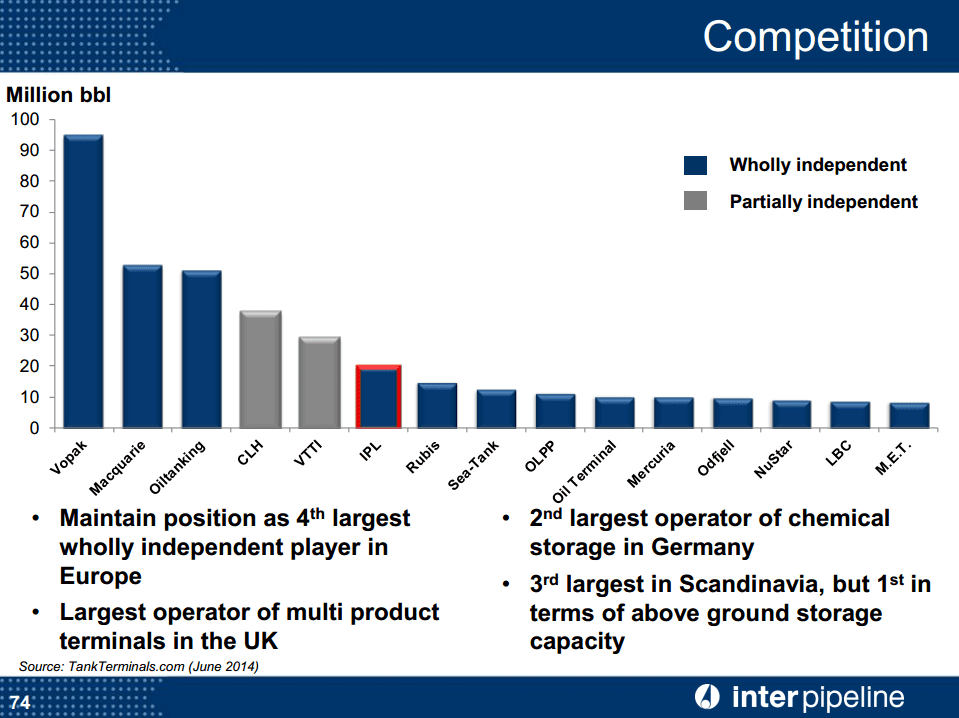

Now to the second slide, why are we highlighting a list of the top 15 European independent storage owners? Three of the names have US ties. NuStar Energy (NS), one of the largest US petroleum transportation and storage companies, operates capacity in the UK and the Netherlands. Oiltanking, a global storage partner for oil and gas, chemicals, and dry bulk, took two of its US terminal assets public in July 2011 as Oiltanking Partners (OILT) and then sold its remaining interests to MLP bellwether Enterprise Products Partners (EPD) last year. And VTTI, co-owned by Dutch energy trading house Vitol and Malaysian shipping conglomerate MISC, recently took a minority interest in its global network of storage tanks public as VTTI Energy Partners (VTTI), becoming the first midstream company with mostly non-US assets to do so. The stock has held up well since its July 2014 inception, outperforming the Alerian MLP Index (AMZ) and Alerian MLP Infrastructure Index (AMZI) by 20% and 17%, respectively. VTTI’s success could prompt other independent global storage operators to consider launching their own MLPs. These companies could also be M&A targets for existing MLPs. VTTI noted in its IPO prospectus that the top 10 independents only own 16% of non-US terminal capacity, suggesting the opportunity for consolidation in that market.

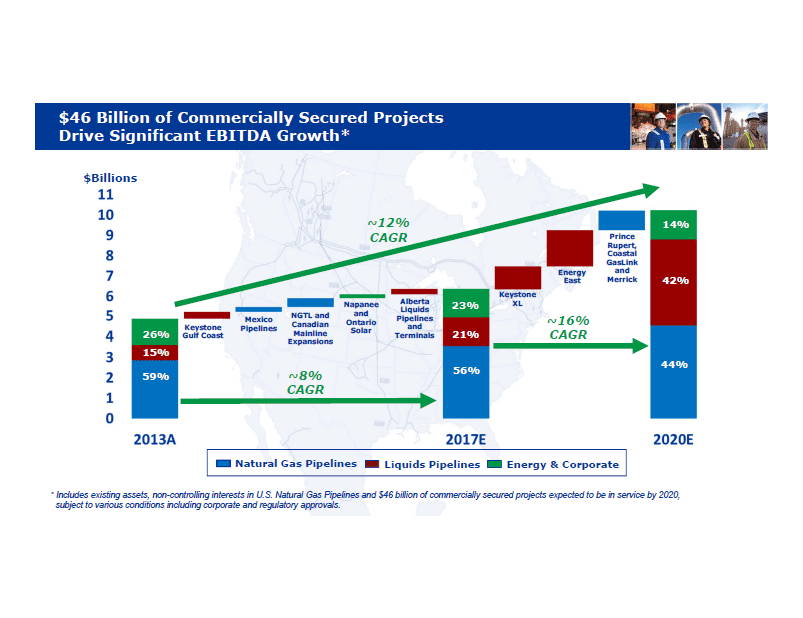

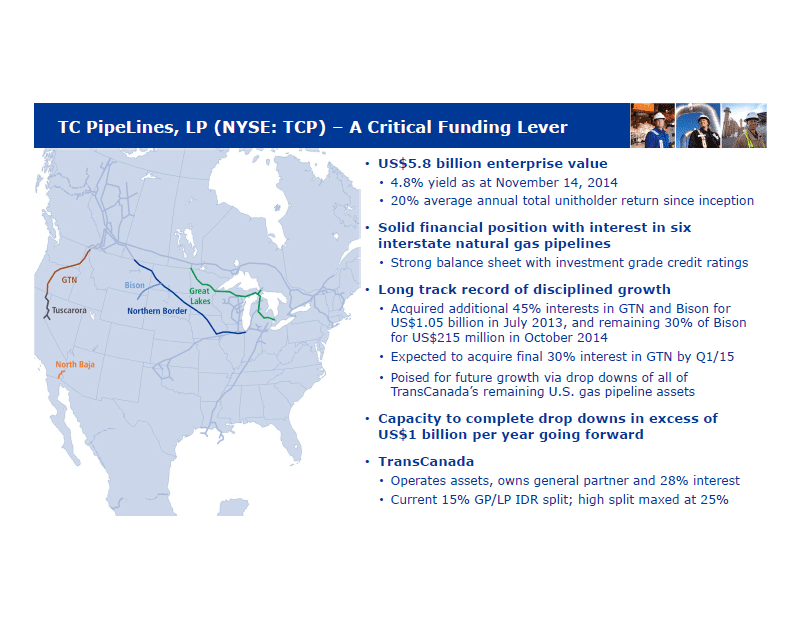

TransCanada and TC PipeLines (slide presentation here)

Let’s just go to the elephant in the room. While there are certainly a few other companies in the business of owning and operating Canadian energy infrastructure assets, it has long been considered a two-horse race between Enbridge Inc (ENB) and TransCanada. From a total return perspective over the last 10 years, however, it’s been a one-horse race, with ENB outperforming TRP by 254% through December 31.

So what’s management’s plan to compete going forward? Higher annual dividend growth anchored by higher EBITDA growth. Two things should be noted, however. One, the asterisk on the first slide. A project can be commercially secure and never receive regulatory approval. Unfortunately for TRP investors, Keystone XL has become the poster child for this scenario. And two, a couple of weeks after TRP’s analyst day, ENB announced a 33% dividend hike in conjunction with a financial restructuring plan and a revised payout policy. ENB management now expects dividend growth for the 2015-2018 period to be 14%-16% annualized. So TRP is still trying to catch up.

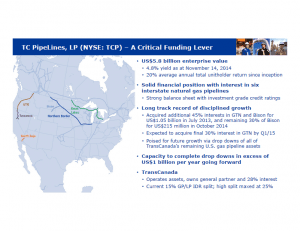

Activist Sandell Asset Management has suggested another route to enhancing shareholder value: an all-in dropdown of the company’s US assets to TCP, a change in reporting metrics, and a spinoff of the company’s power business. It is perhaps noteworthy that in a 109-slide presentation deck, TCP was only in the subject line once, and even then just as a funding lever for its parent. For now, management does not appear to be interested in pursuing the all-in dropdown strategy previously employed by MLP parents Spectra Energy (SE) and Williams Cos (WMB) in 2013 and 2010, respectively. Unfavorable corporate governance has generally spared MLPs from direct activist engagement, minus this 2005 industry classic from Third Point’s Dan Loeb, but their indirect exposure through corporate parents could be on the rise.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}