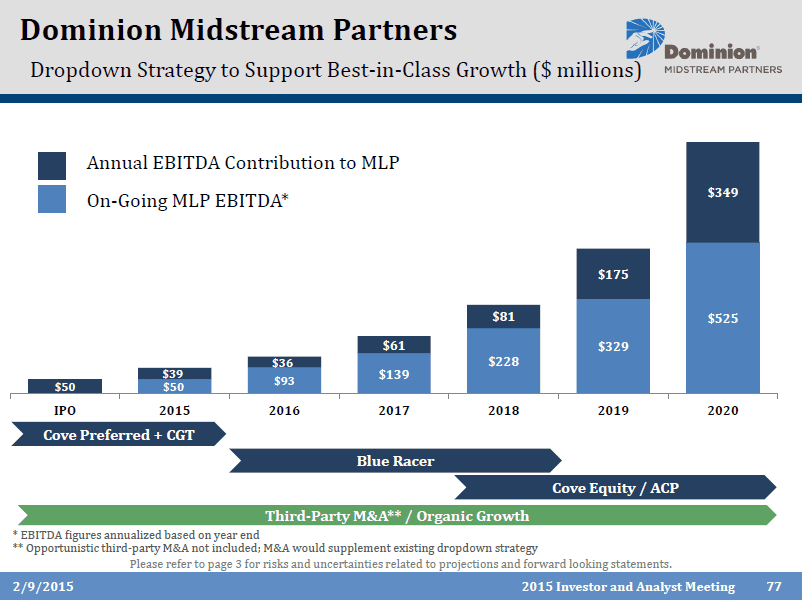

The first slide is the company’s blueprint for getting there. This level of detail not only allows analysts to better understand the timing of dropdowns; it also subtly points out that the assets being sold to DM have an organic growth component to them too. The $89 million of EBITDA projected for 2015 grows to $93 million in 2016 without an acquisition from the parent. The $129 million of EBITDA projected for 2016 grows to $139 million in 2017 without a deal. And so on. In 2020, when DM’s EBITDA hits $874 million, sponsor Dominion Resources (D) expects to generate an additional $1.7 billion in MLP-qualifying EBITDA at the sponsor level. Assuming the size of dropdowns in 2021 and beyond is consistent with the 2015-2020 period as a percentage of prior-year EBITDA, that gives DM another 2-3 years of top-tier distribution growth. In order for investors to continue to ascribe a premium valuation to DM in the 2020s, however, the company will need to keep replenishing its dropdown inventory. Fortunately for management, it has a relatively long time to do that as compared to most of its peers.

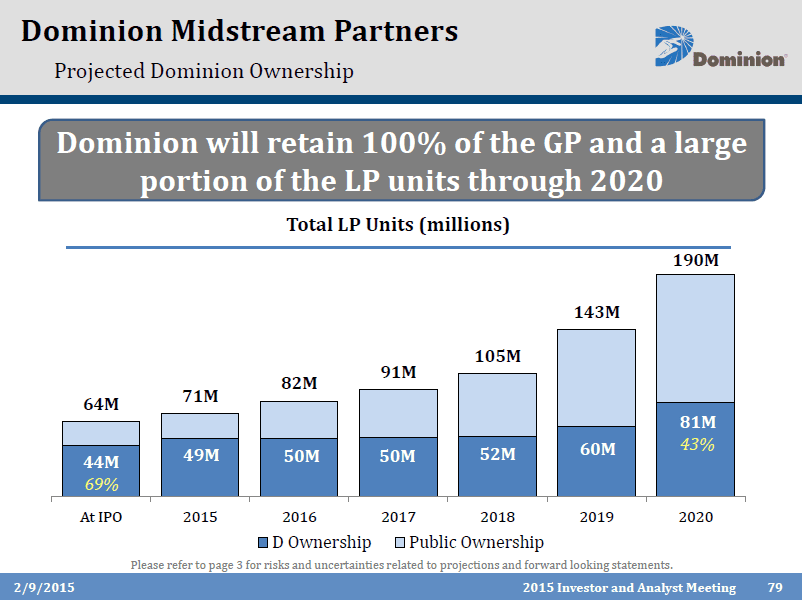

In the second slide, management describes its equity financing plans for these dropdowns. In short: don’t expect D to take a bunch of units in every transaction. Of the 126 million LP units that DM will issue through 2020, D anticipates taking less than 30% of them, resulting in a decline in its LP ownership stake to 43% from 69% at the IPO. In most instances, the knowledge that an MLP will finance an organic growth project or acquisition with public equity creates an overhang on the stock. But investors thus far have found DM’s growth trajectory so compelling that they’re not waiting for the discount associated with these follow-on offerings to take a position. D, meanwhile, will be putting the sales proceeds toward $19.2 billion of growth capex over the next six years, which management believes will drive annual earnings growth of 6%-7% and annual dividend growth of 8% over the same timeframe.

{kind=link}

{kind=link}