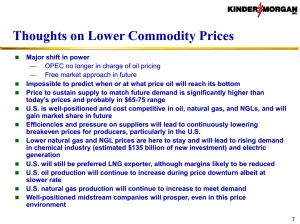

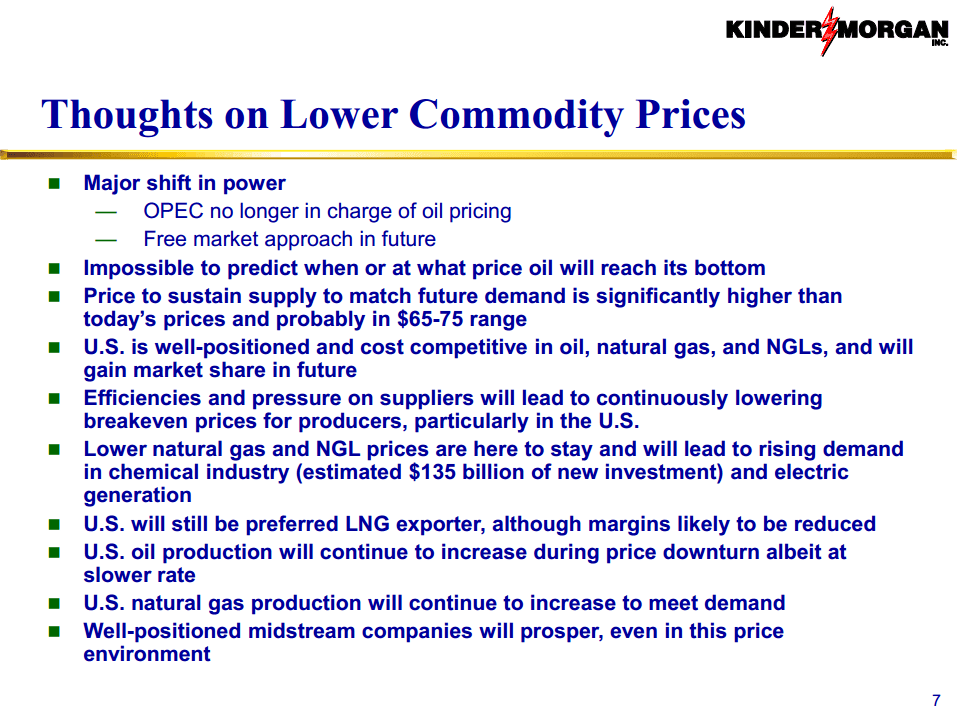

In short: near-term pricing is uncertain, US market share of oil and gas production will continue to increase, breakeven prices will continue to fall due to drilling efficiencies and pressure on suppliers, LNG export margins will fall, and the rate of US oil production growth will slow.

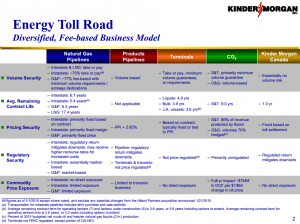

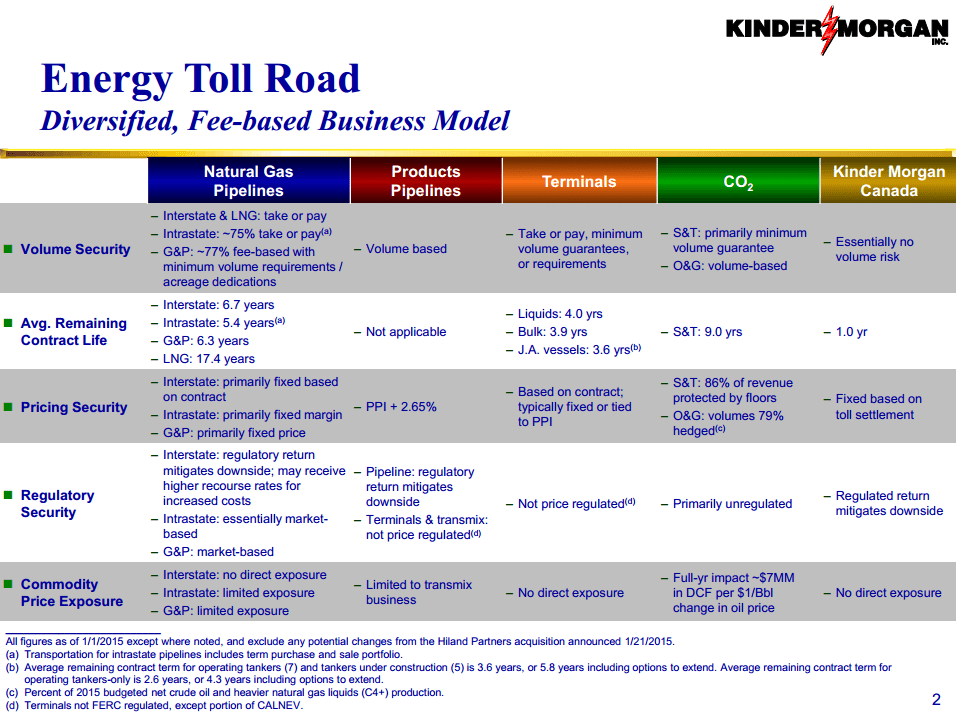

Kinder was quick to follow that assessment with how KMI is “set to weather the storm” with 85% of its cash flows coming from fee-based businesses (94% including hedging). While the investing public’s attention is currently focused (solely, it seems) on each company’s commodity price exposure, long-time energy infrastructure investors know that there are other risks to be aware of, including volumes, recontracting, tariff rates, and regulation. To address these concerns, Kinder included the slide below, which discusses each risk by operating segment.

The transparency here should help investors pacing their bedrooms at 2am get some sleep at night. Management expectations for 15% distribution growth in 2015 and 10%-plus annually through 2020 doesn’t hurt either.

{kind=link}

{kind=link}