Despite being 0.4 miles from our office, fellow Alerianite Karyl Patredis and I drove to the Ritz-Carlton in Dallas for the Energy Transfer Family of Partnerships analyst meeting because (1) it was 37 degrees outside, (2) no one finds it strange to drive 0.4 miles in Texas, and (3) I wouldn’t make an eight-month-pregnant woman walk any more than necessary.

The analyst meetings were held over the course of two days. Day 1 consisted of presentations from Regency Energy Partners (RGP) (2.50 hours) and Sunoco Logistics Partners (SXL) (1.25 hours), with a 30-minute break in between. The two partnerships were an interesting contrast to each other, since RGP focuses more on natural gas and SXL focuses more on crude oil and NGLs. Also, RGP has grown primarily through acquisitions over the past year whereas SXL has grown primarily through organic projects.

I’ll start with SXL. (Download SXL presentation.) When I think of SXL, I think of their dramatic quarter-over-quarter distribution growth, all those Mariner projects in the Northeast, and all those projects in the Permian. President and CEO Michael Hennigan provided an excellent overview of crude and NGL fundamentals and put in perspective the thought process behind each of SXL’s major projects in the Marcellus and Permian, all in less than 45 minutes. Impressive.

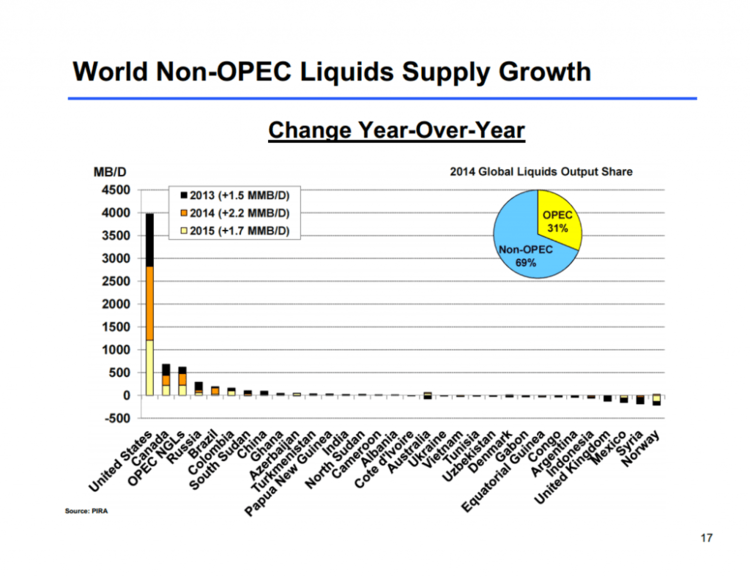

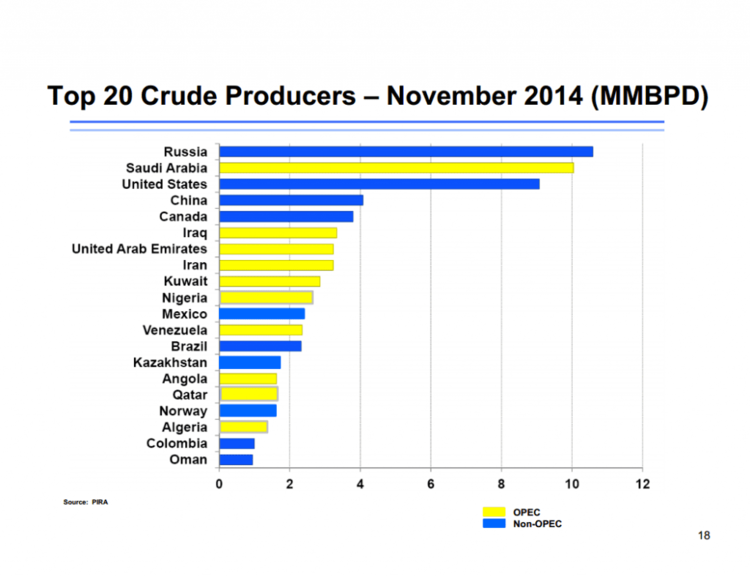

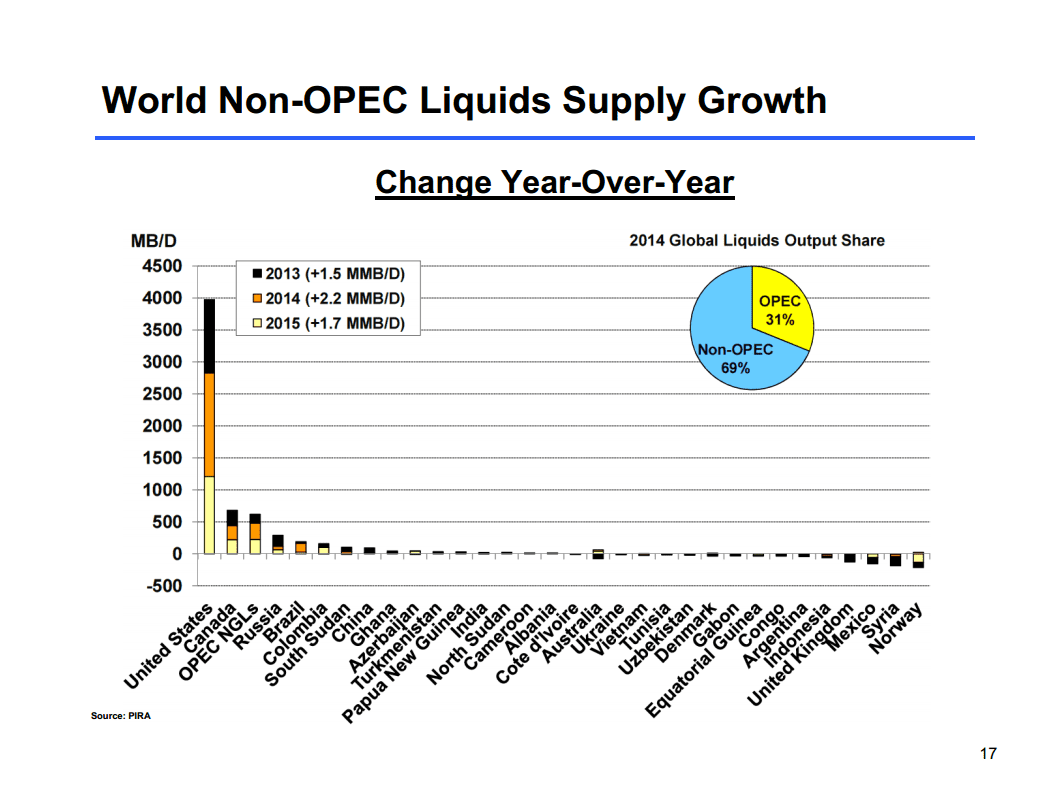

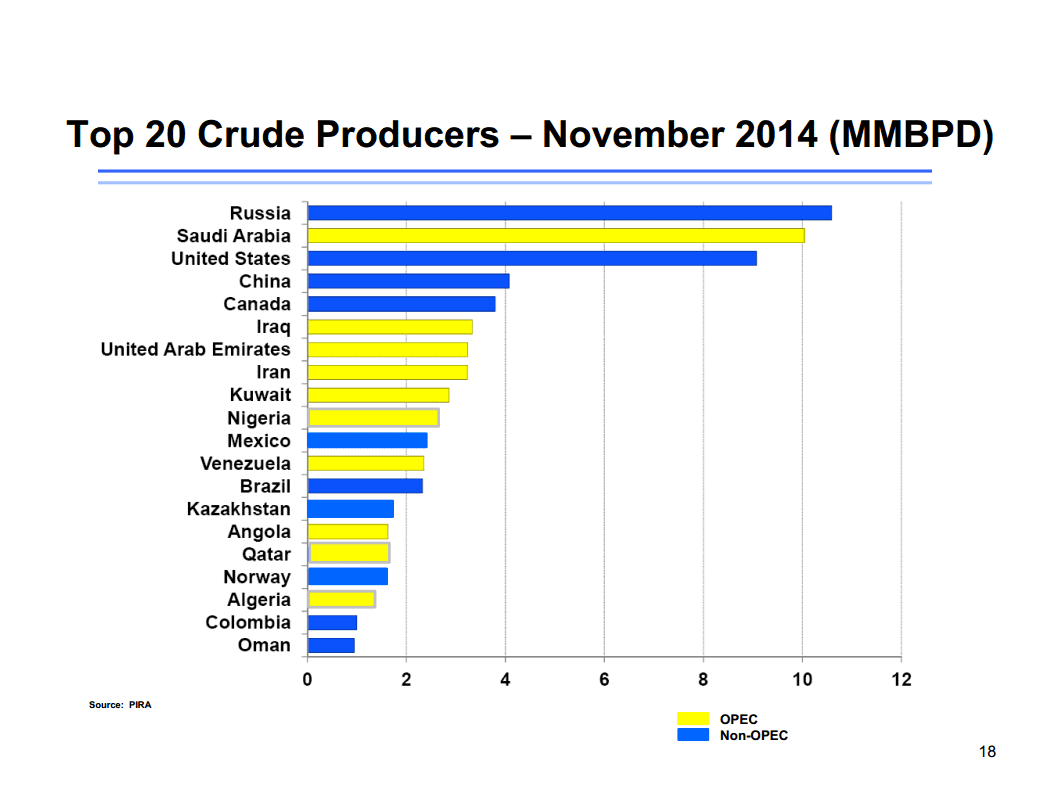

We all know that US year-over-year production is on a tear, but this chart puts in better perspective just how much relative to other nations:

Enough that we’ll probably take the #2 spot from Saudi Arabia in 2015, and eventually be the leading crude producer in the world.

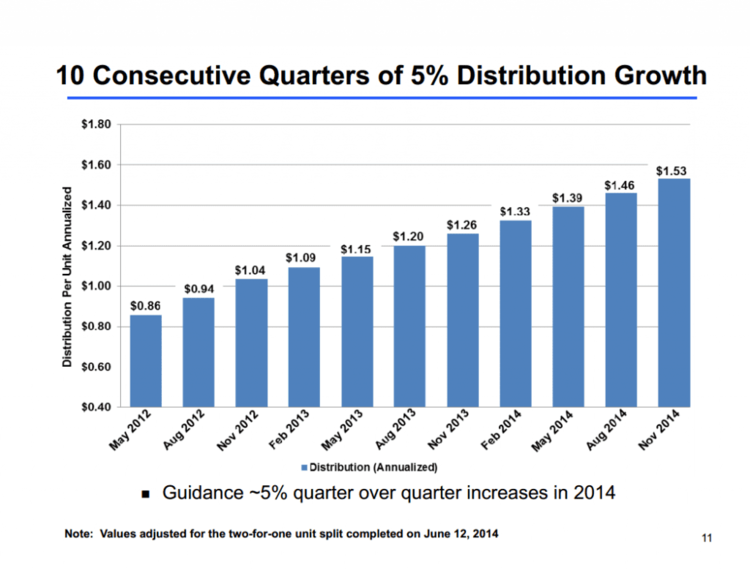

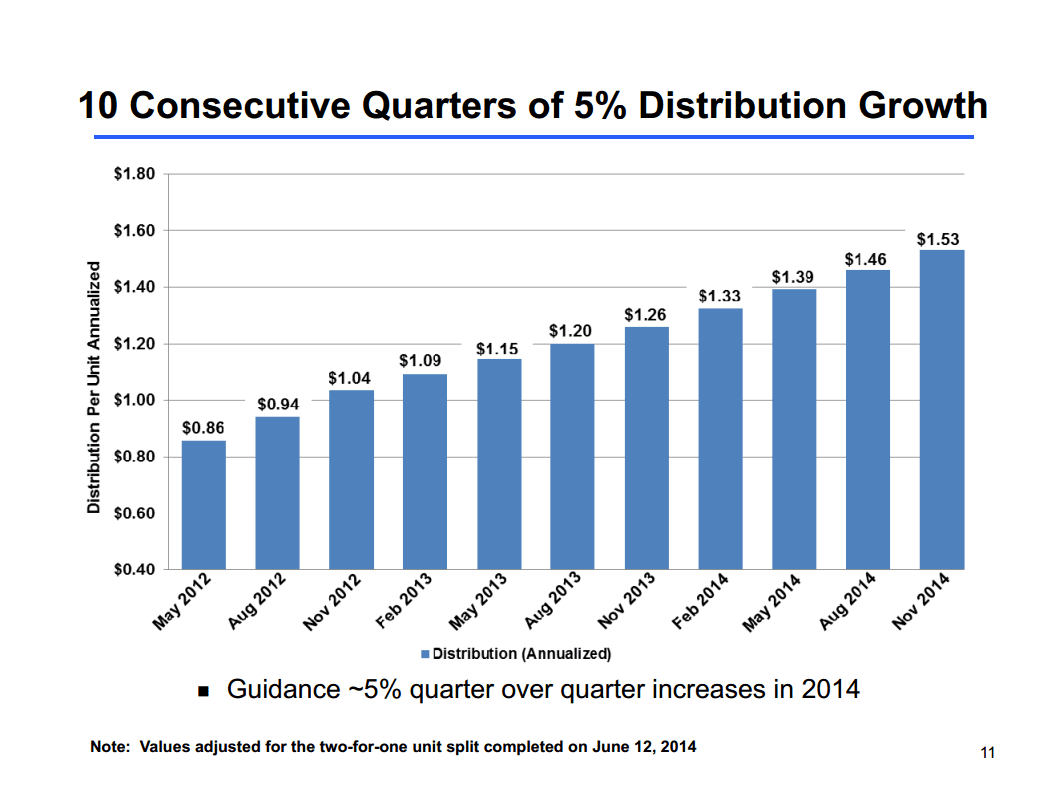

In 2010 and 2011, SXL barely spent $200 million each year in organic capex. Starting in 2012, things began to change. SXL spent $300 million that year, just shy of $1 billion in 2013, and is expected to spend a total of $2.5 billion in 2014. This has translated into 10 consecutive quarters of 5% distribution growth, or 78% on a cumulative basis over 2.5 years. This compares to distribution growth of 1.5%-2% per quarter in previous years.

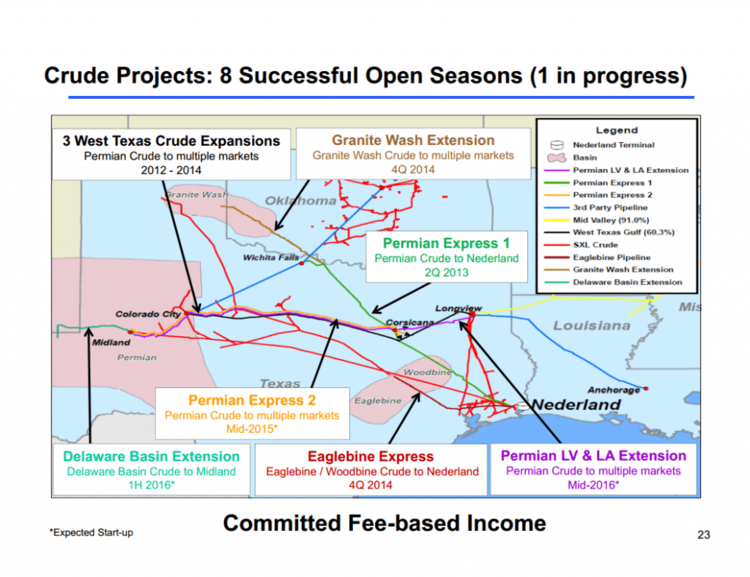

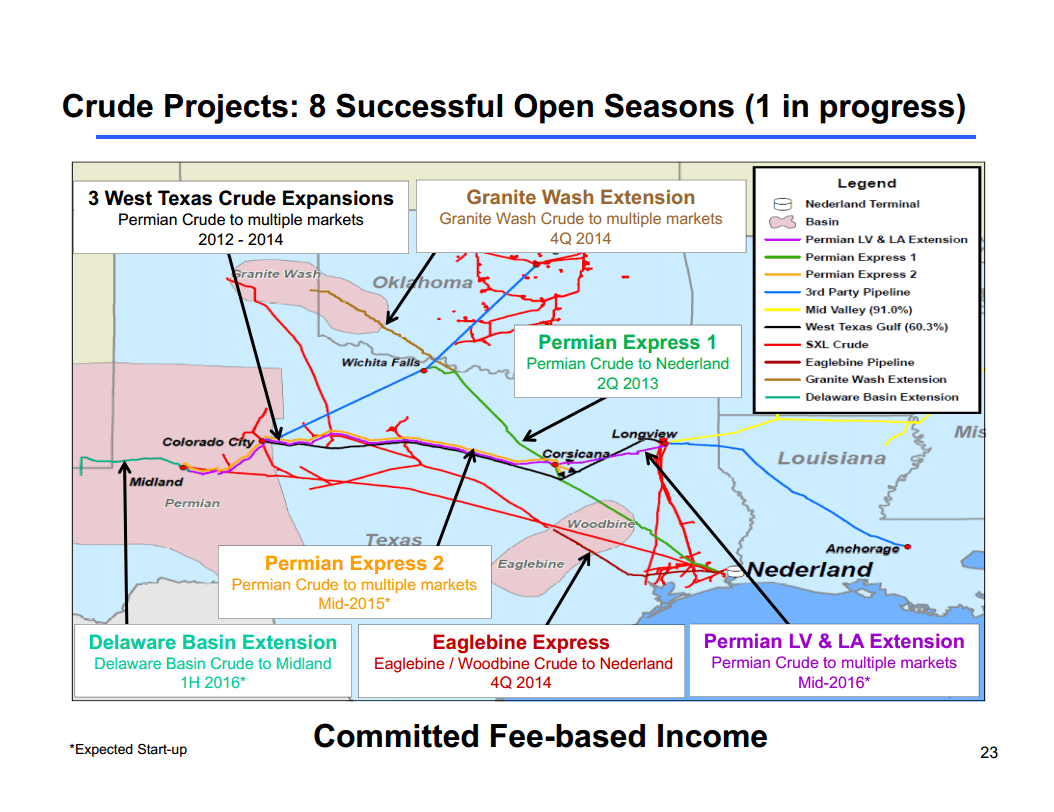

Permian crude oil production has been increasing annually by 250-300 Mbpd, resulting in fierce competition to secure producer commitments and build the next takeaway pipeline solution. SXL has built out an extensive pipeline network to “drag” (as Hennigan would say) production from the Permian to SXL’s Nederland terminal on the Gulf Coast, with five additional projects underway.

To answer the million-dollar breakeven oil price question, Hennigan noted that the breakeven price for oil sands and offshore deepwater production has been increasing since 2010, whereas the breakeven price for shale oil has been decreasing to $65 per barrel from $80 over that same time period. In short: Permian production won’t be slowing down anytime soon.

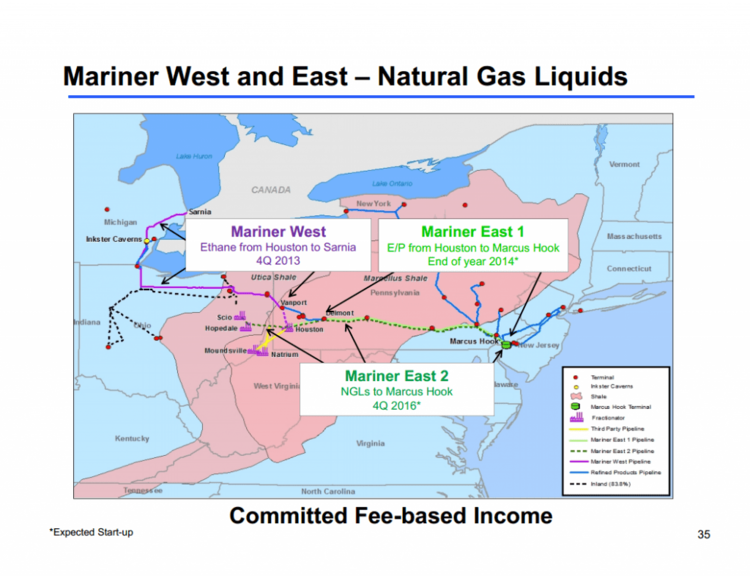

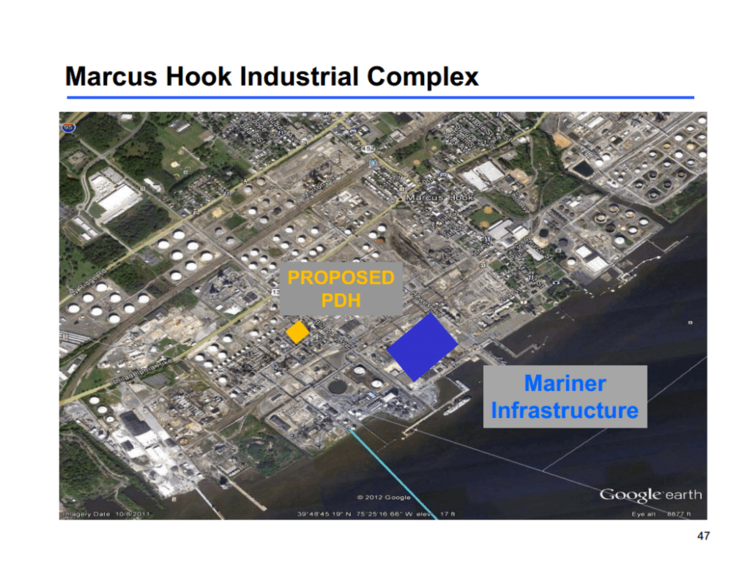

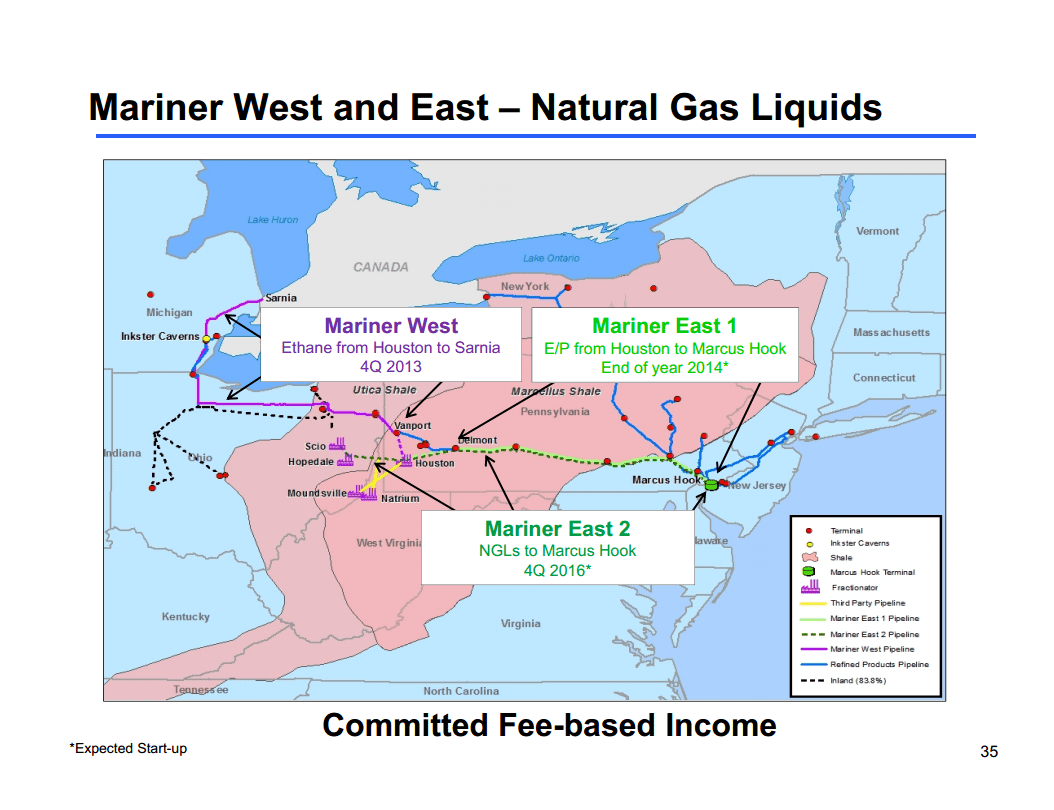

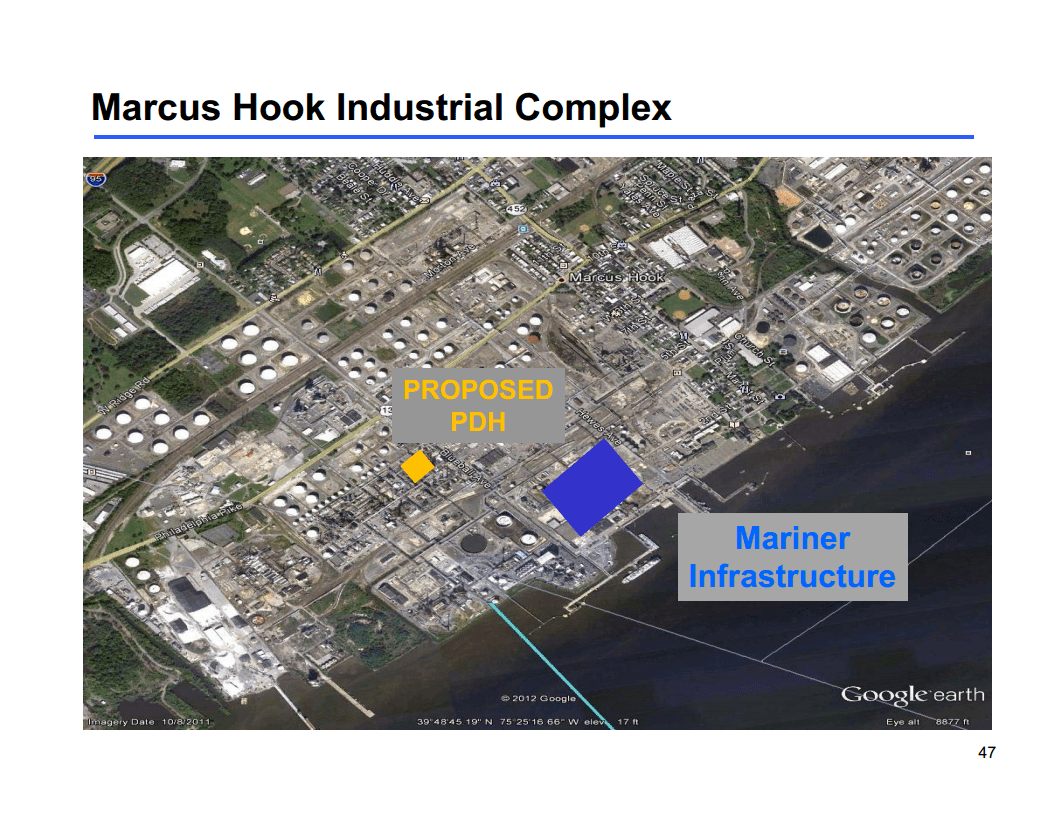

On the liquids front, with the help of increasing production from the Marcellus and Utica, SXL’s goal is to make Marcus Hook the Mont Belvieu of the East. Haters gonna hate and think all liquids should go to Mont Belvieu, but SXL is proving them wrong with plans to export ethane off the East Coast by mid-2015.

From above, there’s still plenty of room for Marcus Hook to expand as a liquids hub. Hennigan admitted that Marcus Hook will never have the underground storage capabilities as Mont Belvieu, but the need for propane and butane storage is lessening as the US becomes a top exporter of liquids.

While it’s impressive that SXL has created an NGL franchise in the Northeast, a crude oil franchise in the Permian, and increased their distributions 78% in the last 2.5 years, I was most impressed with Hennigan’s humbleness, noting several times how happy they were to be a part of the Energy Transfer family, as well as thankful for the partnership opportunities and resource sharing they’ve been able to utilize.

Now, switching gears to RGP. (Download RGP presentation.)

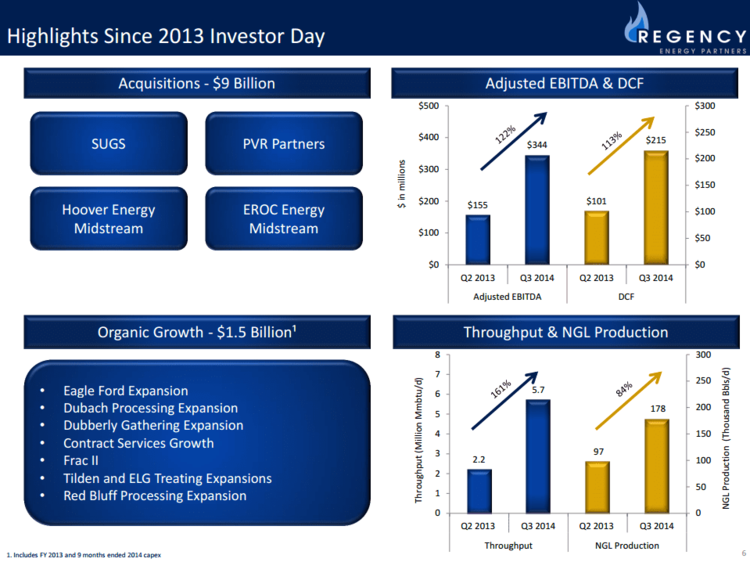

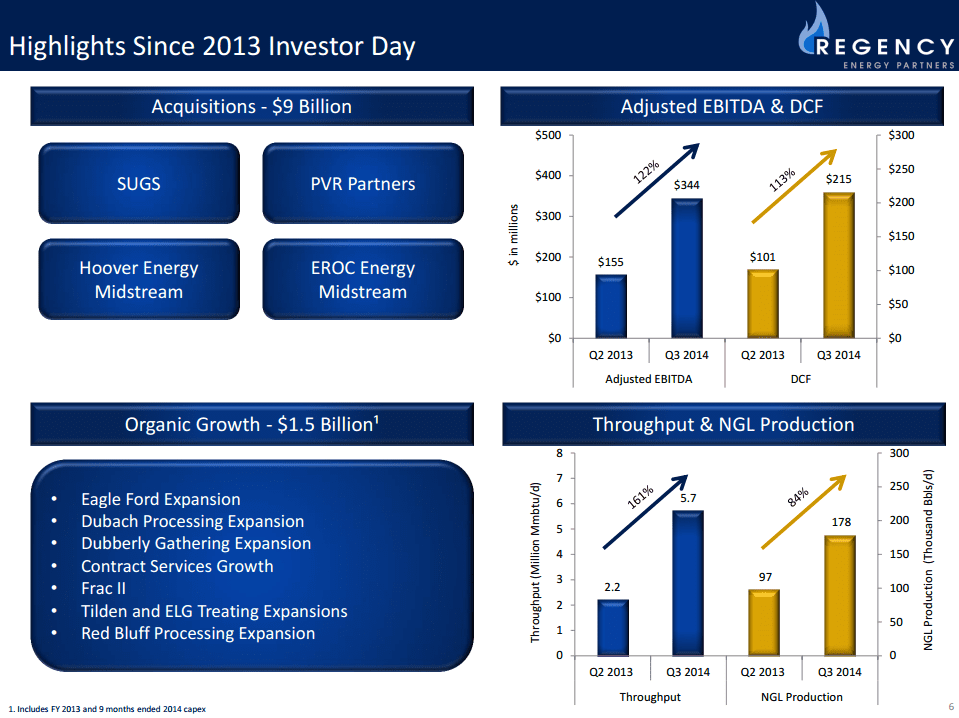

Over the last 19 months, RGP has spent nearly $9 billion on four major acquisitions. For context, RGP’s current enterprise value is roughly $19 billion.

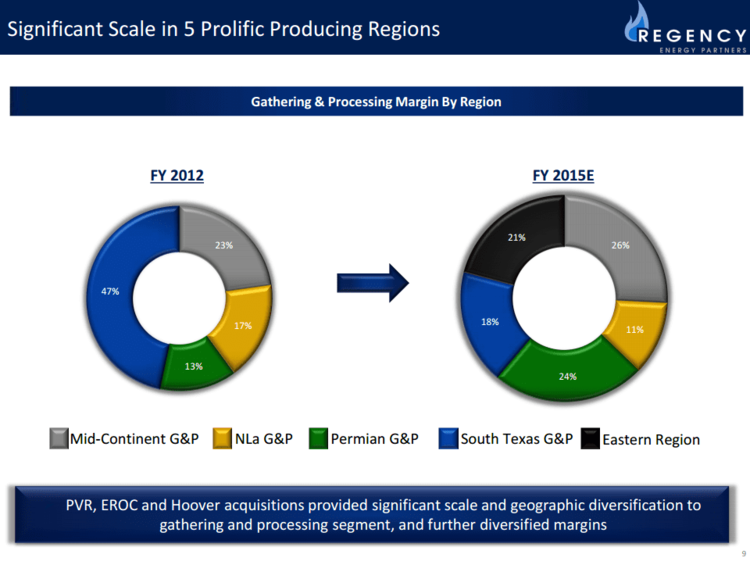

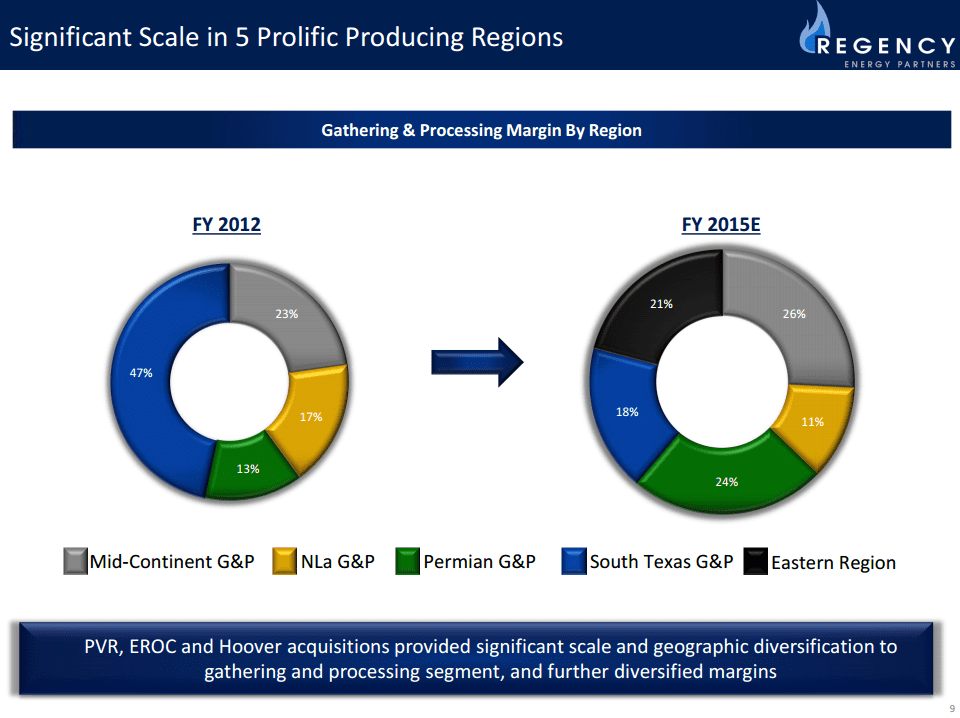

Single basin exposure can be dangerous, as basin economics can fluctuate from time to time. The result of these four acquisitions has been a more balanced gathering and processing portfolio across five major producing regions, as well as significant scale within these regions.

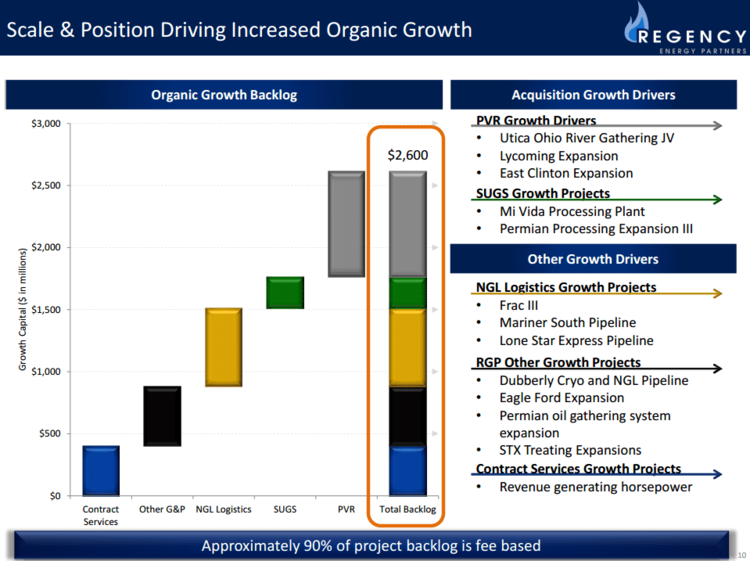

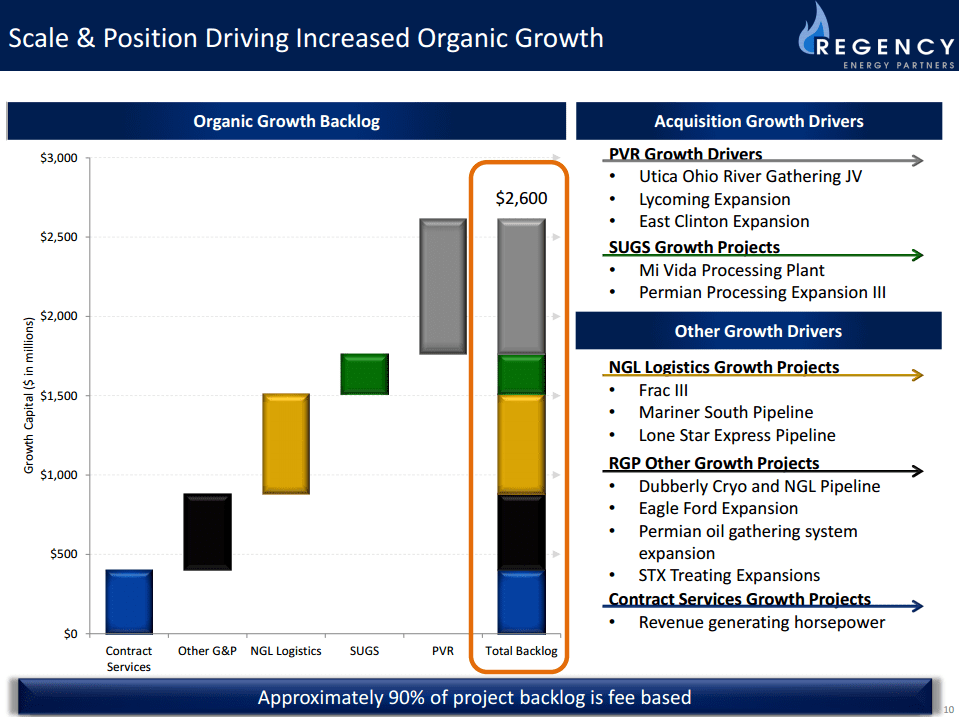

RGP now has an organic project backlog of $2.6 billion: $1.5 billion from legacy assets and $1.1 billion from the SUG and PVR assets.

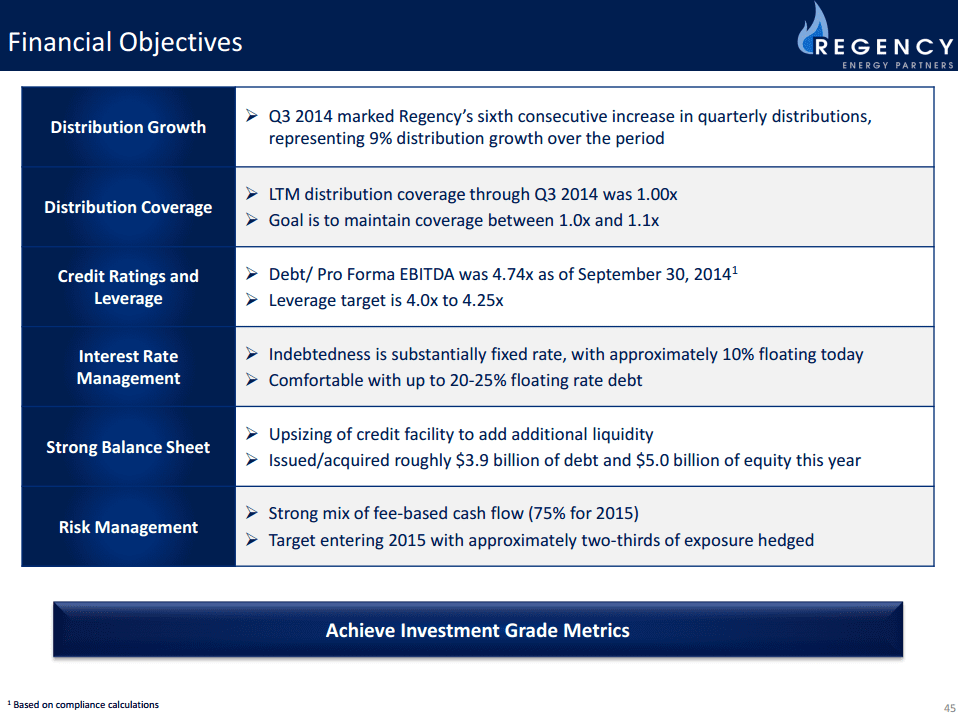

A large portion of the financial discussion was on RGP’s goal of achieving an investment grade rating from the credit agencies. The major issue to address will be the 4.7x Debt/EBITDA ratio, which already includes some EBITDA credit for the organic projects underway and some EBITDA credit from recent acquisitions, but not all. It’s interesting that their leverage target is 4.00x-4.25x, whereas the majority of investment grade MLPs try to target sub-4.0×. Management noted that if EBITDA from all projects were fully accounted for, RGP’s leverage ratio would be at 4.0×.

Maria Halmo and Kenny Feng attended Day 2 of the meetings. Look for their recap shortly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}