Summary

- There are interesting strategic parallels between refining and midstream, and notable lessons that midstream can learn from refiners as their forebears in free cash flow generation.

- Refiners were able to attract an expanded investor base as structural tailwinds drove free cash flow that was largely returned to shareholders.

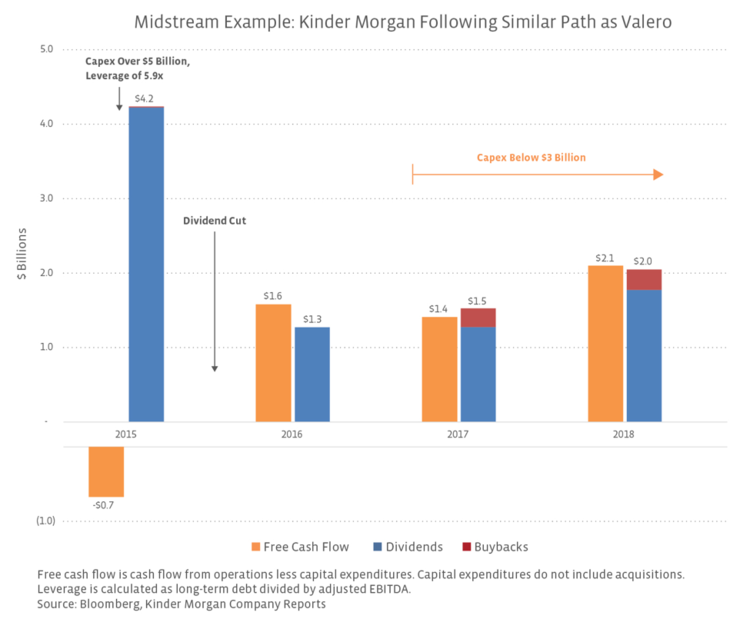

- Midstream has the potential to follow in refining’s path by growing free cash flow and enhancing shareholder returns.

Refining has been the best-performing subsector of energy (excluding renewables) for five of the last eight years. How did refiners, whose profit is totally dependent on volatile commodity prices, become a darling of energy? While structural benefits like U.S. crude discounts undoubtedly helped refining as oil price weakness hurt other subsectors, the shift to harvesting free cash flow and funneling it into shareholder returns was also key. As discussed last week, midstream is getting closer to reaching an inflection point for free cash flow generation as growth spending moderates in line with more modest US oil and natural gas production growth. There are interesting strategic parallels between refining and midstream, and notable lessons that midstream can learn from refiners as their forebears in free cash flow generation.

Growth: Refiners have found new growth areas.

Growth capital spending for midstream likely peaked last year as large pipeline projects progressed or came online, particularly out of the Permian. One pushback to midstream is the future growth profile. These concerns are manifested in questions from investors wondering whether the US has all the large pipelines it needs or if regulatory hurdles would make it difficult to build major new pipelines. To make a parallel with refining, there hasn’t been a new refinery of scale built in the US since the late 1970s. In spite of this, refiner cash flows have grown through capacity expansions, self-help projects to improve margins, and structural benefits such as crude discounts and cheap natural gas prices. Growth has also come from acquisitions and stepping out into related businesses (midstream, fuel marketing, petrochemicals, lubricants, and renewable fuels, among others).

Just as refiners have grown without building new refineries, midstream can also grow outside of newbuild long-haul pipelines. Expanding existing pipelines by adding pumping power is a capital-efficient means to grow. (If regulatory hurdles prevent new large pipelines from being constructed, that makes existing pipelines all the more valuable.) Export facilities are another growth opportunity, with several projects in the works spanning hydrocarbons. Midstream can also step out into related fields like petrochemicals (read more), water infrastructure (read more), and even refining with a set fee for processing. For example, Phillips 66 Partners (PSXP) constructed an isomerization unit at Phillips 66’s (PSX) Lake Charles Refinery, which produces gasoline blendstocks, and Holly Energy Partners (HEP) owns certain processing units at HollyFrontier’s (HFC) Woods Cross refinery. Acquisitions represent another avenue of growth for midstream. Private equity (PE) investments at the asset level (read more) may result in those assets eventually coming up for sale when PE exits. Of course, midstream companies would need to be careful to not overpay for any acquisitions.

Investor base: Refiners managed to attract new investors.

Years ago, hedge funds were significant investors in refiners. Generalist long-only investors (seen as the holy grail for practically any energy company today) typically steered clear of refining given the volatility and complexity of the profit drivers. However, the structural benefits of US crude discounts that began in 2010 combined with shareholder-friendly practices began to more meaningfully attract long-only investors that had previously shied away from the space. The supportive macro backdrop drove significant free cash flow, which was largely returned to shareholders through dividend increases and share buybacks. This helped retain an expanded investor base. If midstream follows a similar path, it could also attract new investors, and to its advantage, midstream arguably has more readily understood and less volatile profit drivers.

Could midstream follow in refining’s shareholder-friendly footsteps?

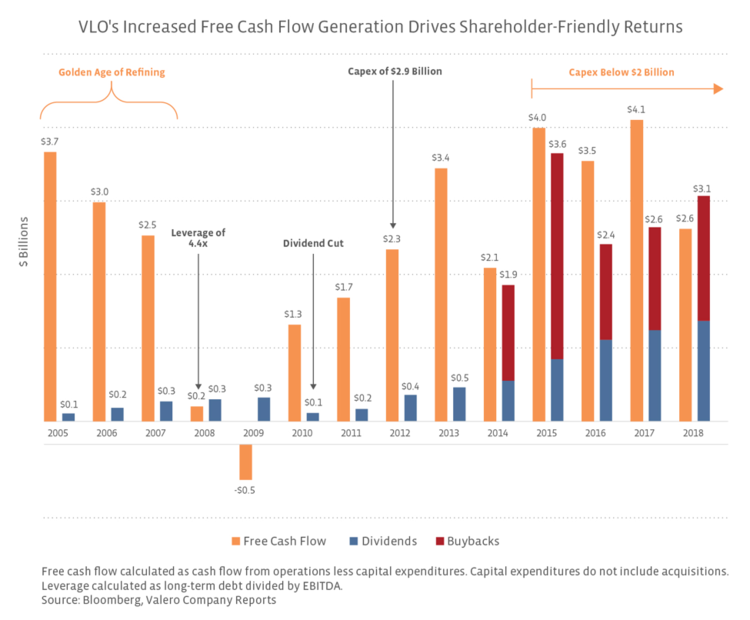

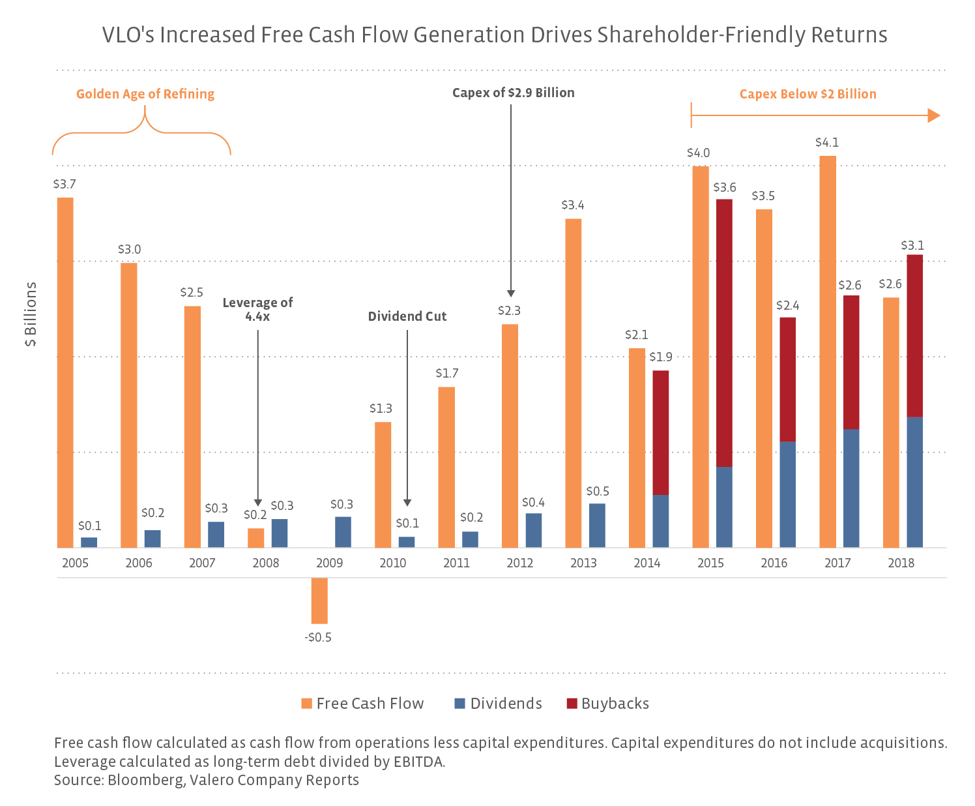

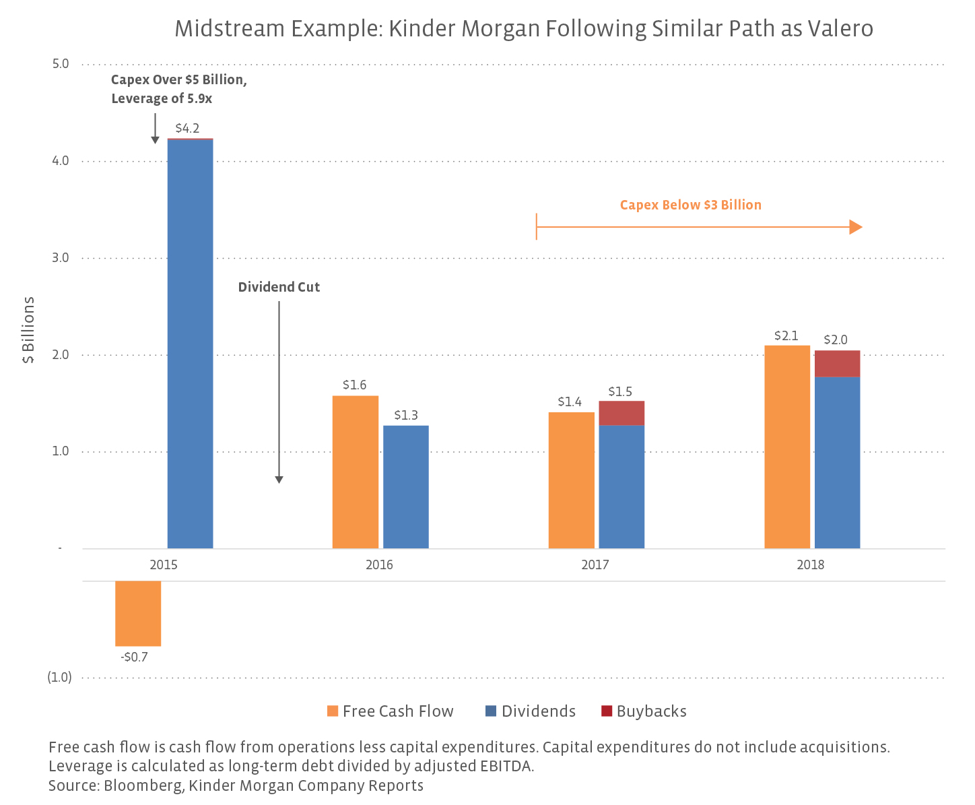

Though it’s no longer the largest refiner by capacity in the US – a title which now belongs to Marathon Petroleum (MPC) – Valero (VLO) has long been the US refining bellwether. Its size and longevity lends itself to a long-term view as shown in the chart below. The company generated significant free cash flow during the Golden Age of Refining, but free cash flow dried up with the Great Recession. VLO’s leverage increased to over 4x in 2008, and the company cut its dividend in 2010. Things quickly turned around as US crude discounts developed. Free cash flow increased, capital spending moderated to below $2 billion annually, and leverage fell to ~1×. VLO initiated a target payout ratio of 50% for 2015, and for 2019, the company targeted a payout ratio of 40-50% of adjusted net cash provided by operating activities.

{kind=link}

{kind=link}