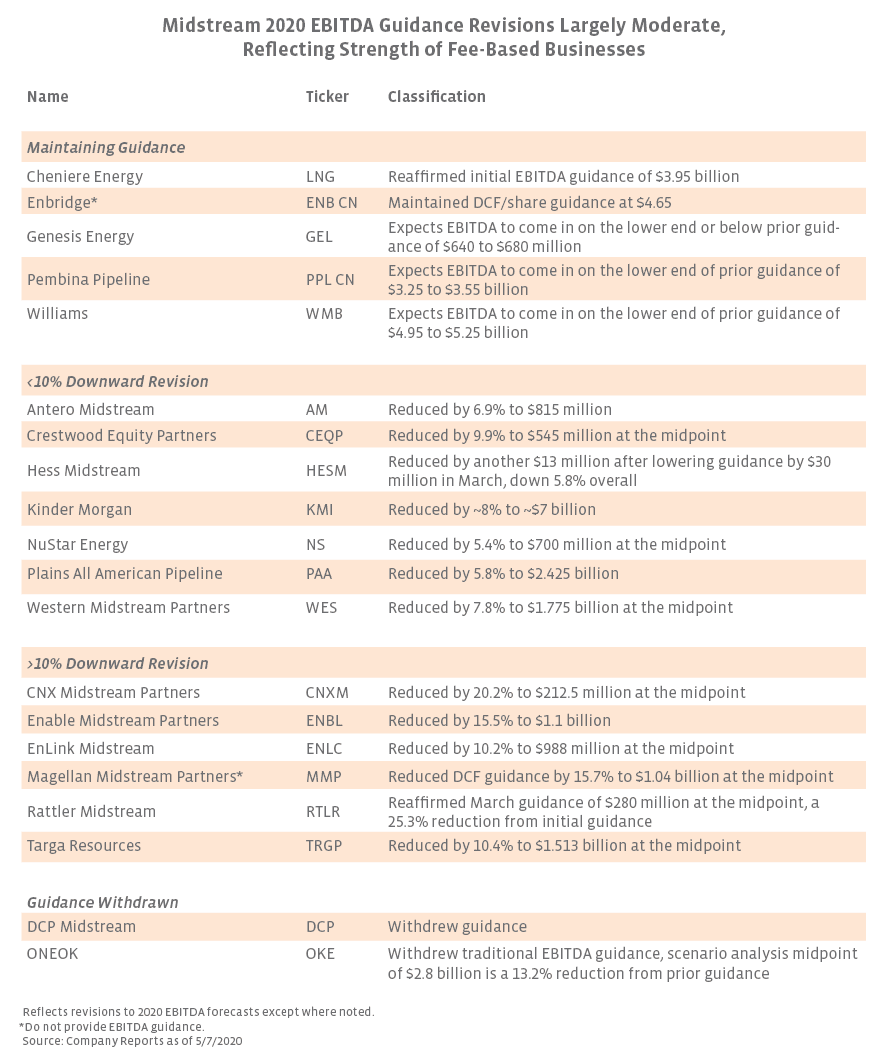

In light of the unknowns surrounding COVID-19, DCP Midstream (DCP) and ONEOK (OKE) withdrew their traditional EBITDA guidance. OKE instead provided an EBITDA scenario analysis of $2.6 billion to $3 billion, the midpoint of which represents a 13.2% downward revision from its prior guidance. DCP updated guidance for select metrics but excluded EBITDA. A few companies have offered other 2020 guidance measures in lieu of EBITDA forecasts. In conjunction with deferring $1 billion of growth capex, Enbridge (ENB) maintained its distributable cash flow (DCF) per share guidance of $4.65. Magellan Midstream Partners (MMP) adjusted its full year DCF guidance to $1.04 billion at the midpoint, a 15.7% reduction from initial guidance. MMP also stated that it intends to maintain its distribution throughout 2020. In addition to WMB and ET, MLPs Crestwood Equity Partners (CEQP) and MPLX (MPLX) reiterated expectations to generate positive free cash flow after their dividends in 2020 and 2021, respectively. While reduced capital spending (detailed here) lowers the hurdle for generating excess cash flow, maintaining free cash flow guidance with steady dividend payouts should still be welcomed by investors. CEQP, ET, MPLX, and WMB all maintained their dividends sequentially in 1Q20.

Overall, these guidance updates continue to underscore the benefits of midstream’s fee-based business model and resilience in a pressured environment, particularly when compared to other sectors of energy.

Links to Company Earnings Reports:

Antero Midstream (AM)

Cheniere Energy (LNG)

CNX Midstream (CNXM)

Crestwood Equity Partners (CEQP)

DCP Midstream (DCP)

Enable Midstream (ENBL)

Enbridge (ENB)

EnLink Midstream (ENLC)

Genesis Energy (GEL)

Hess Midstream (HESM)

Kinder Morgan (KMI)

Magellan Midstream Partners (MMP)

MPLX (MPLX)

NuStar Energy (NS)

ONEOK (OKE)

Plains All American (PAA)

Pembina Pipeline (PBA/PPL CN)

Rattler Midstream (RTLR)

Targa Resources (TRGP)

Western Midstream (WES)

Williams (WMB)

{kind=link}