Summary:

- If management teams feel that dividend/distribution growth is not being rewarded by the market, buybacks may be an appealing option to help support prices.

- Buybacks are ultimately a capital allocation decision, and companies will need to weigh buybacks against other uses for their cash and returns on that cash.

- Prolific growth opportunities at attractive returns likely put a damper on midstream buybacks, but the fact that midstream has shifted from discussing equity issuances to buybacks should be welcomed by investors.

Midstream buybacks are in the spotlight following Enterprise Products Partners’ (EPD) announcement of a $2 billion buyback program on January 31. We previously wrote about MLP buybacks in November 2017. Since then, buybacks have become a more common topic on earnings calls for midstream MLPs and corporations. For companies that have historically been prolific issuers of equity, the fact that buybacks are becoming a more prevalent topic in capital allocation conversations reflects the changes that have taken place in recent years, including greater C-Corp representation in midstream, the shift to self-funding, and prioritizing total return over yield alone.

Why buybacks?

If one were to poll MLP or midstream management teams about their valuations, chances are that most executives would likely express some degree of dissatisfaction with where their equity is trading. Buybacks are one way to support equity prices when a company views its units or stock as undervalued. Beyond dividend/distribution growth, buybacks are an alternative way to return capital to unitholders or stockholders. On its recent earnings call, EPD’s management noted a clear preference for buybacks over distribution growth based on investor feedback in recent months. If management teams feel that dividend growth is not being rewarded by the market, buybacks may be an appealing option to help support prices.

When do buybacks make sense?

Even if a management team believes its equity is severely undervalued, buybacks may not be viable. To state the obvious, buybacks will not be realistic for every midstream company. Some companies will need to use cash for other purposes – reducing debt, paying their dividend, funding capital projects, etc. A homeowner probably would not spend money on expensive window treatments if their home had a broken heater or plumbing problems that had not been addressed. It just doesn’t make sense to spend money on window treatments when there are bigger issues to address. Similarly, buybacks likely will not make sense if a midstream company has high leverage, difficulty affording its dividend, or unmet funding needs. In announcing its buyback program, EPD noted that the first step to returning more cash to unitholders was to first achieve equity self-funding (read more) and to improve its credit metrics.

Buybacks are ultimately a capital allocation decision, and companies will need to weigh buybacks against other uses and returns on their cash, particularly growth projects. In its evaluation, EPD considers the distributable cash flow (DCF) per unit yield and returns on organic growth projects, as well as how a project would impact its overall footprint and current leverage. EPD cited an indicative DCF-per-unit yield of 11% on the $30.8 million buyback completed in December 2018 under a prior buyback program. Capital projects involve greater risk and require a higher return to reward companies for that risk. In addition to risk, the time value of money should also be considered given the immediate impact of buybacks when compared to a multi-month or multi-year construction period for a newbuild project.

At its investor day, the management of Kinder Morgan (KMI) discussed targeting a 15% unlevered after-tax return on projects or a levered after-tax return of 25-30%. The levered return is compared to returns on share repurchases because a share repurchase is buying equity in a levered company. The 25-30% levered after-tax return compares to a sub-20% return on share repurchases, with KMI citing some variability based on assumptions around multiple expansion. Given these differences in returns, KMI indicated that projects would be the priority for free cash flow, and leftover cash would be used for share repurchases.

Prioritizing growth projects over share repurchases is not unique to KMI in the midstream space. The yields for individual companies will vary, but if KMI’s project returns are somewhat representative, it’s easy to see that many midstream companies could be in a similar predicament. Magellan Midstream’s (MMP) management indicated on its 4Q18 earnings call that they are not positioned to do buybacks today because they have better ways to use their cash based on their slate of growth projects. Similarly, MPLX (MPLX) management noted on their recent call that organic growth opportunities are the focus for capital deployment today. As we have discussed in the past, there are plenty of growth opportunities for midstream companies given the robust growth in energy production from the US and Canada and growing exports (read more). Prolific growth opportunities at attractive returns likely put a damper on midstream buybacks, but that isn’t a bad thing.

Could buybacks be gaining traction in the midstream space?

EPD and KMI both have $2 billion buyback authorizations, with KMI having purchased ~$525 million under its buyback program since December 2017. NGL Energy Partners (NGL) announced this week that its lenders have granted approval to purchase up to $150 million in common units (not to exceed $50 million per fiscal quarter) if certain financial conditions are met. NGL currently meets these requirements and expects to maintain them for the remaining life of the credit agreement. To be clear, authorizations for these companies are not commitments to fully repurchase the authorized amounts.

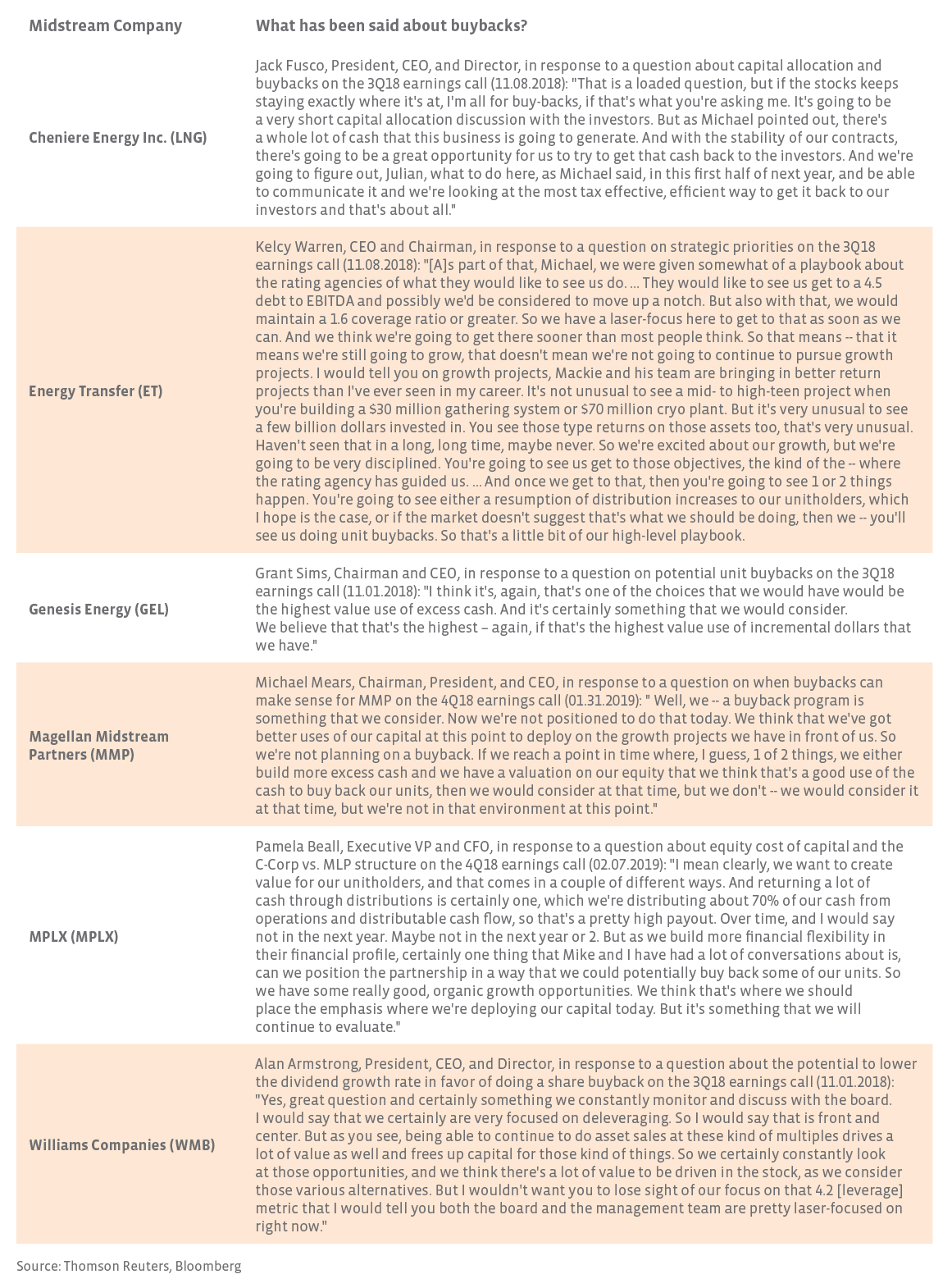

Many more midstream companies are considering buybacks, but for some, achieving a certain leverage target or allocating capital to growth projects are higher priorities today. The table below provides recent commentary from various midstream companies on buybacks.

Bottom line

For midstream MLPs and corporations with excess free cash flow, buybacks represent one of many alternatives for that capital, competing with dividend growth, new projects, and debt reduction. Robust growth opportunities may limit buybacks as companies see strong project returns, but the fact that buybacks are becoming a more prevalent topic in midstream capital allocation conversations reflects the changes that have taken place in this space in recent years. The shift from equity issuances to discussing buybacks should be a welcome development for midstream investors.

{kind=link}