Summary //

- Out of the 39 dividend-paying constituents in Alerian’s broadest midstream index, AMNA, 33 companies maintained payouts, 3 cut, and 3 grew sequentially.

- Multiple names have provided 2021 dividend/distribution guidance and are anticipating flat or increasing payouts.

- Although some dividend cut risk still exists, the vast majority of midstream names appear well positioned to continue to provide investors with steady, attractive income.

Even as buyback programs become more common among MLPs and midstream companies (read more), dividends/distributions remain front and center for investors, particularly in the current yield-starved environment. Since the initial wave of dividend cuts in the wake of COVID-related oil demand destruction this spring, midstream payouts have generally held steady, though there were three cuts among 3Q20 announcements. Despite mostly stable payouts, midstream yields have remained stubbornly elevated. For context, the November 13 yields of 8.51% and 11.57% for the Alerian Midstream Energy Index (AMNA) and Alerian MLP Infrastructure Index (AMZI) are 193 and 286 basis points above their five-year averages, respectively. Today’s piece breaks down 3Q20 midstream dividend announcements and discusses the outlook for payouts going forward.

3Q20 Dividends: Three cuts overshadow stability and a few examples of growth.

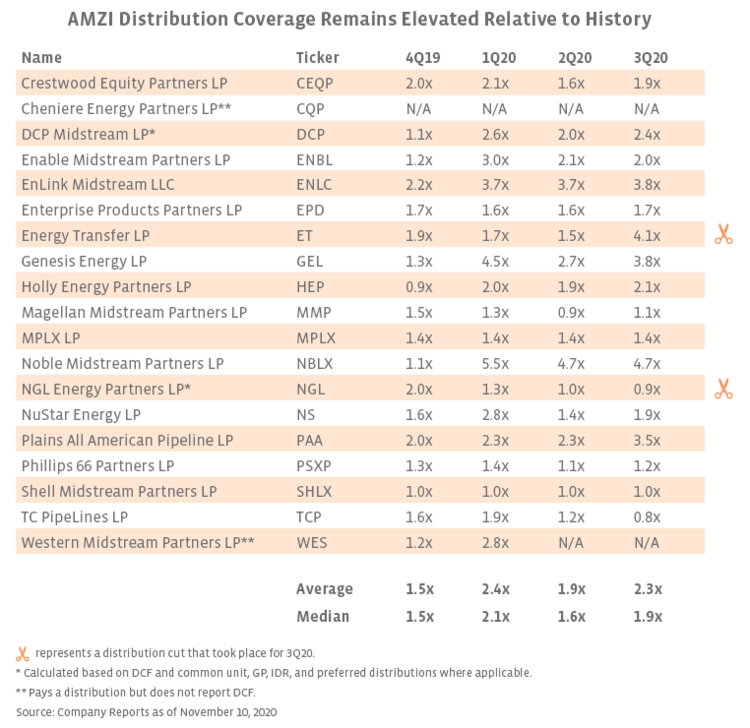

Last quarter, only one small MLP cut its distribution, and the majority of midstream names kept dividends flat (read more). With several cuts to 1Q20 dividends (read more), the ability of midstream companies to afford their dividends has markedly improved. (Please see AMZI distribution coverage details in the appendix.) Stability remained the overarching trend in 3Q, but that tends to be overshadowed by a couple cuts. The charts below show the quarter-over-quarter (Q/Q) changes to dividends for constituents of the AMNA, AMZI, and Alerian MLP Index (AMZ). To be clear, 3Q20 dividends refer to the dividends that will be paid in 4Q20 based on third quarter results. The three names in AMNA that do not currently pay a regular dividend are Cheniere Energy (LNG), Macquarie Infrastructure (MIC), and Tellurian (TELL). However, MIC announced plans to pay a special dividend of approximately $10.75 per share subject to board approval upon closing of the sale of its International-Matex Tank Terminals business, which is anticipated later this year or in early 2021. Additionally, Cheniere’s management characterized a dividend as an “eventuality” on their 3Q call.

Using our broadest midstream index, AMNA, as a benchmark for the space, 36 of the 39 dividend-paying midstream companies either maintained or increased their payouts sequentially for the quarter. For the third straight quarter, Cheniere Energy Partners (CQP), Delek Logistics Partners (DKL), and Hess Midstream (HESM) raised their distributions. Three MLPs announced distribution cuts: Energy Transfer (ET), NGL Energy Partners (NGL), and Rattler Midstream (RTLR). Both ET and NGL reduced payouts by 50%, citing the desire to accelerate deleveraging. This was NGL’s second cut this year, with the 3Q20 payout representing a total decline of 74.4% from its 4Q19 distribution of $0.39/unit. Instead of being leverage focused, RTLR’s distribution cut represented an opportunistic reallocation of capital in response to the market environment. Alongside its 31.0% reduction, the partnership launched a $100 million unit repurchase program as another means of returning capital to its unitholders. Even after accounting for recent cuts, each of these names continued to yield north of 10% as of November 13, which to be fair, is not unique among midstream names.

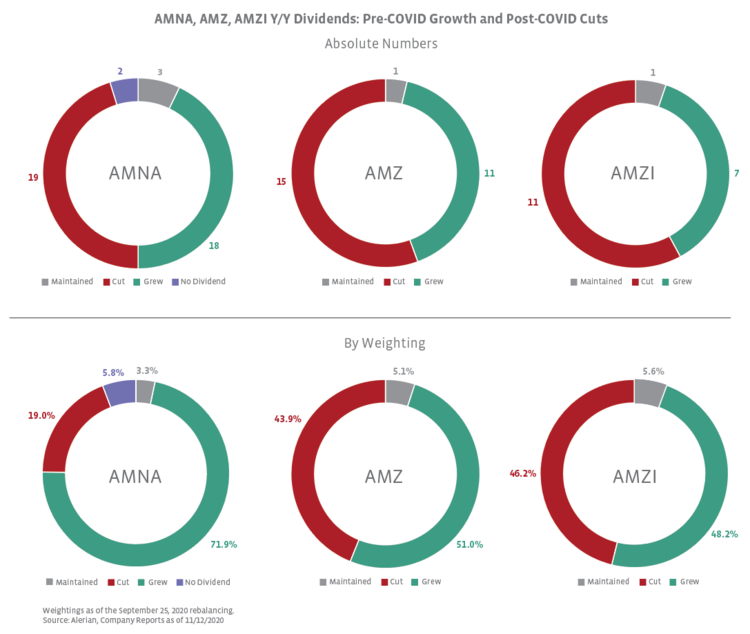

Year-over-year comparison reflects pre-COVID growth and post-COVID cuts.

With a few exceptions, the midstream universe has largely been maintaining dividends rather than growing in order to protect balance sheets and preserve financial flexibility. The year-over-year comparison below reflects the combination of growth from names that raised 4Q19 payouts in early 2020 and post-COVID cuts for many names. While a somewhat muddied comparison, the charts below provide helpful context, particularly given that some companies, such as Enbridge (ENB) and TC Energy (TRP), have historically grown their dividends on an annual basis instead of making smaller, quarterly increases. As shown, the majority of AMNA, AMZ, and AMZI constituents by weighting have either grown or maintained their dividends on a year-over-year basis. For AMNA specifically, 71.9% of the index has grown payouts from 3Q19 to 3Q20, reflecting the health of the larger names that command a higher weighting in the index and the inclusion of US and Canadian corporations, such as ENB and TRP. It is worth noting again, however, that the vast majority of this growth occurred in 4Q19.

What’s next for dividends/distributions? While a recovery in energy fundamentals, particularly for oil, remains in process, dividends from midstream companies are expected to remain largely steady. This view is supported by the combination of proactive cuts already made and the solid positioning of large names that have maintained payouts. Looking ahead to 2021, some companies have discussed maintaining payouts next year or even targeting growth. Magellan Midstream Partners (MMP) plans to target 2021 distributions at the current level as noted in the 3Q release. In its preliminary 2021 guidance, Western Midstream Partners (WES) indicated that it intends to pay at least $1.24/unit of distributions for the year, which is in line with its existing quarterly payout. CQP is guiding to continued annual growth of 1.9% at the midpoint for its 2021 distributions. TRP continues to project 8-10% dividend growth in 2021 followed by 5-7% annual growth afterwards. Altus Midstream (ALTM), which is not currently in AMNA, announced that management would recommend to its board initiating a quarterly dividend of $1.50 per share starting in March 2021, sending shares up 204.5% on the day of the announcement.

While the likelihood of further dividend cuts is seen as limited, there is still some risk. Many companies have already cut to prioritize their balance sheets, but there could be straggler cuts announced with a goal of reducing leverage. Persistently high yields could also cause boards and management teams to reevaluate dividends as the market has arguably not adequately rewarded steady payouts. Elevated yields could lead to additional examples of a dividend cut paired with a buyback announcement, similar to RTLR, though it seems unlikely that many companies will follow in RTLR’s footsteps (read more). Finally, the outcome of the legal proceedings surrounding the Dakota Access Pipeline (DAPL) could impact the distribution of Phillips 66 Partners (PSXP). On the 2Q20 call, management indicated a DAPL shutdown would be reason to evaluate the distribution. Despite these risks, the vast majority of names are well positioned to continue to maintain their current dividends, and some are positioned for growth.

Bottom Line

Despite a few cuts this quarter, the majority of the MLP/midstream universe has continued to provide investors with substantial income, with a couple names even continuing to raise payouts throughout the year. Looking ahead, the vast majority of energy infrastructure companies appear well positioned to maintain their current dividends or even provide growth, representing an attractive opportunity for income-seeking investors.

Appendix