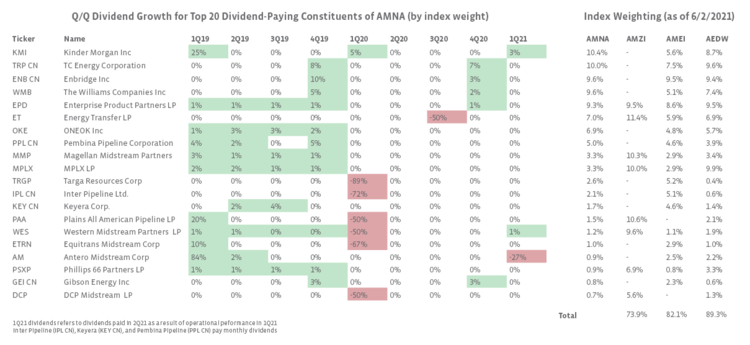

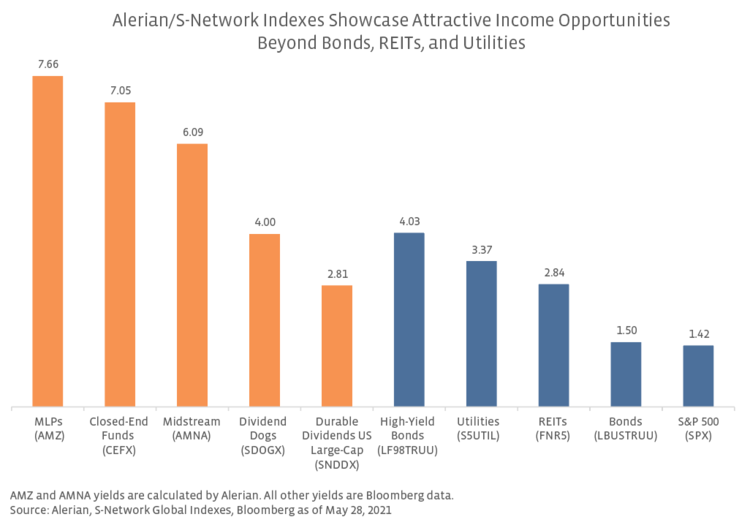

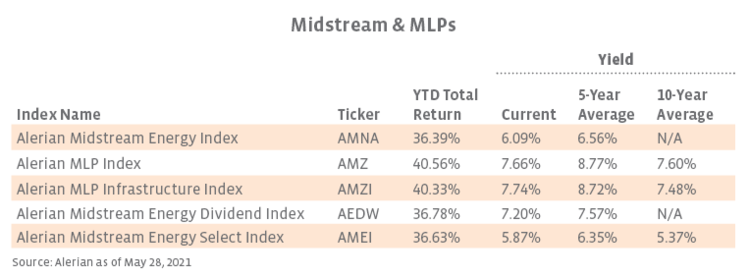

As the financial implications of COVID worsened in early 2020, midstream yields increased to peak levels due to overall weak equity performance, and multiple midstream corporations and MLPs cut their dividends by 50% or more, though cuts were biased to smaller names in the space (read more). Since then, dividends have remained mostly stable each quarter, which allowed yields to moderate to more sustainable levels as equity prices continued to improve (see our most recent dividend recap note). Currently, the yield for the Alerian Midstream Energy Index (AMNA)—Alerian’s broadest midstream index—is 6.1%, which is only slightly below the five-year average yield of 6.6%. The Alerian MLP Index (AMZ)—a narrower universe of energy infrastructure MLPs—has a current yield of 7.7%, compared to the five-year average yield of 8.8%. While both indexes are trailing their five-year average yield, they continue to offer higher yields relative to other income-oriented sectors including bonds, utilities, and REITs.

With lower capital expenditures compared to prior years, midstream companies are beginning to generate more free cash flow, which provides financial flexibility to maintain or grow dividends. During the past few quarters, several constituents have placed an emphasis on positive free cash flow (FCF) after dividends. For example, Kinder Morgan (KMI), has generated positive free cash flow after dividends since 2016 and has significantly reduced annual capex spend. Another large constituent, Williams (WMB) also reported positive FCF after dividends in 2020 and expects to do so again in 2021. Higher free cash flow gives companies more options to either pay off debt or pay for dividends/repurchases. Although repurchases are becoming more popular, dividends are still the primary method of returning capital to shareholders within the midstream space.

Current Yields vs. History

Midstream/MLP indexes continue to offer healthy yields near historical averages.

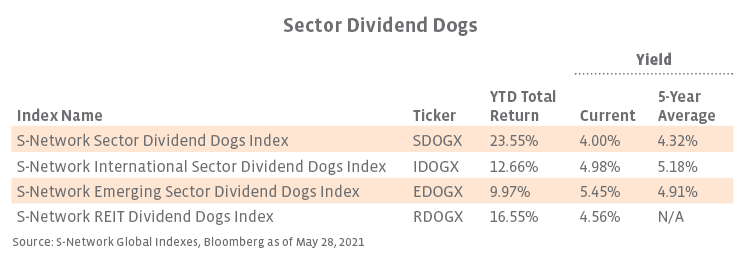

Among the Sector Dividend Dogs, yields are not too far from historical averages. EDOGX is the only index in the suite to offer a current yield above the 5-year average.

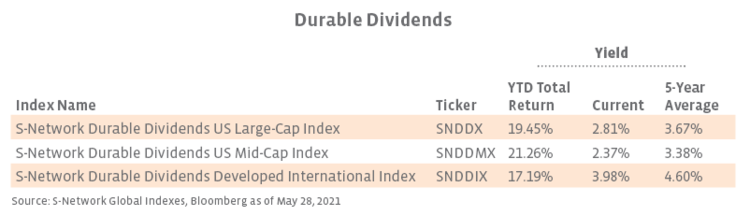

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes.

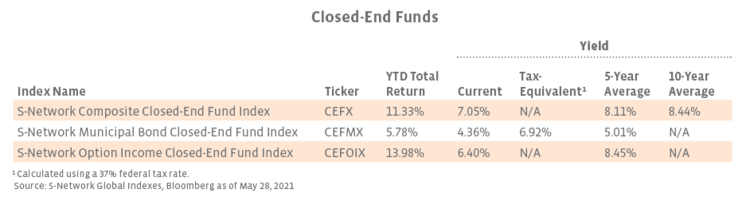

Though current yields are below historical averages, closed-end funds continue to represent an attractive option for enhancing the yield of an income-oriented portfolio.

Related research:

1Q21 MLP/Midstream Dividend Recap: Stability Intact

Weather, Improving Macro Drive Strong 1Q21 for Midstream

Midstream/MLPs: 2020 Cost Discipline Has Benefits into 2021

Insights at a Glance: Midstream/MLP Buyback Update

Biden’s Tax Proposal and Tax-Efficient Income Opportunities