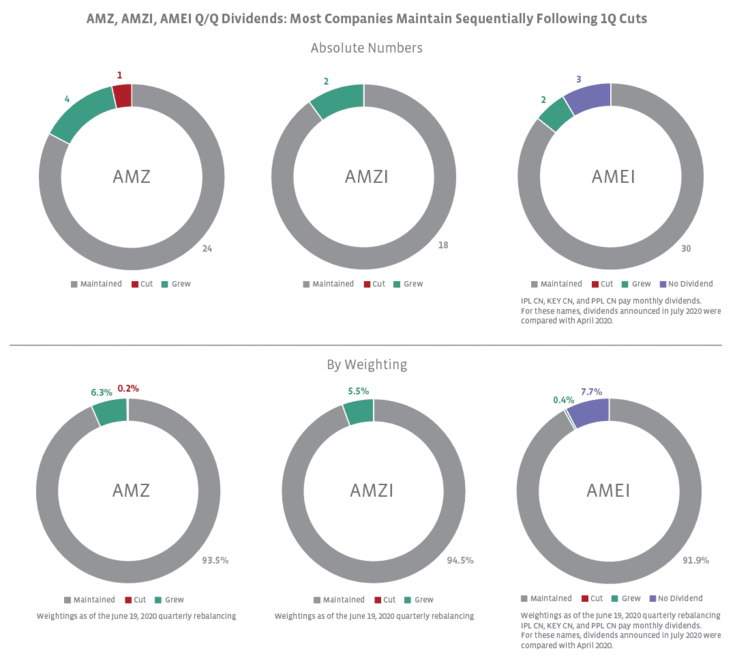

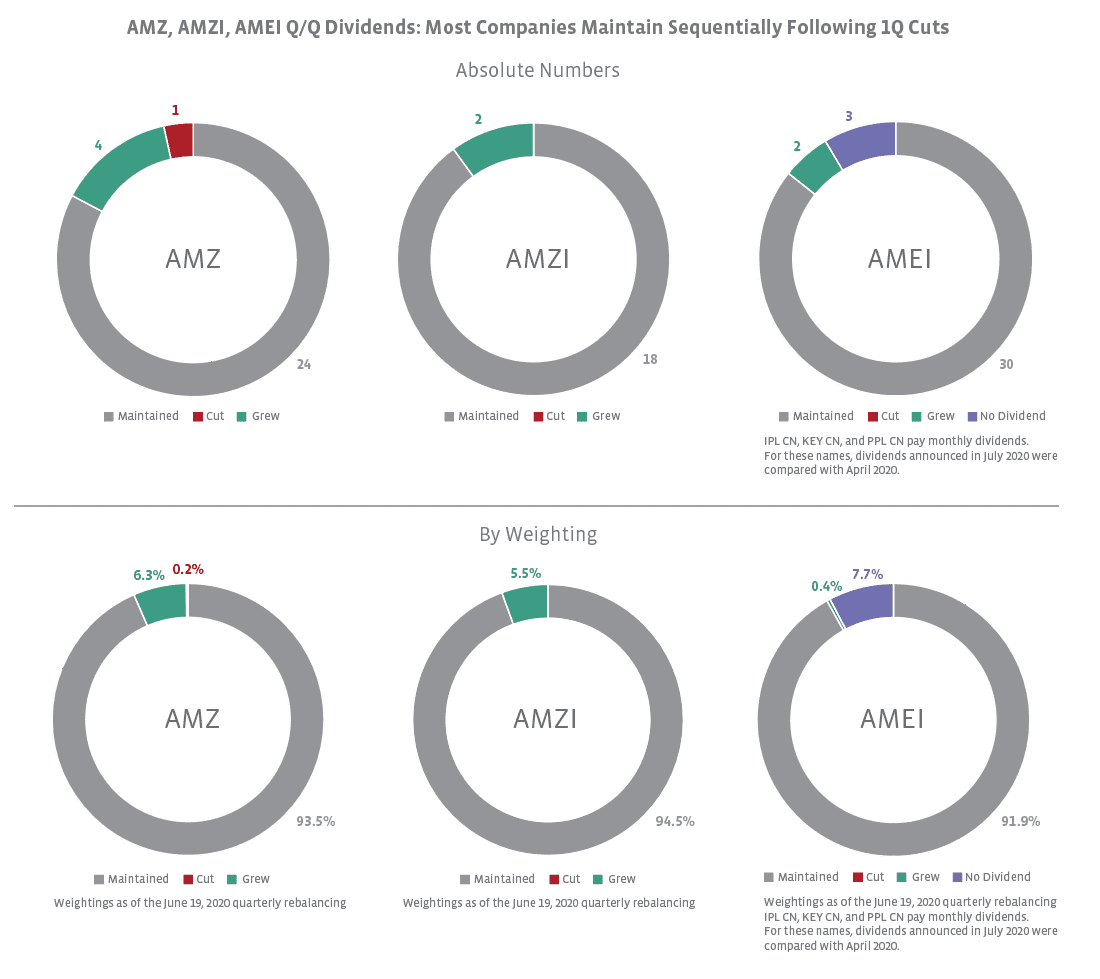

A handful of MLPs grew their distributions sequentially for 2Q20, while C-Corps all maintained. Hess Midstream (HESM), Delek Logistics (DKL), and Cheniere Energy Partners (CQP) increased their distributions approximately 1% sequentially. All three had increased their payouts for 1Q20 as well. Alongside the announcement that it is being acquired by CNX Resources (CNX), CNX Midstream (CNXM) announced a 2Q20 distribution of $0.50 per unit – up from $0.0829 per unit in 1Q20. Per the merger documents, CNXM is barred from making any additional distributions without the consent of CNX.

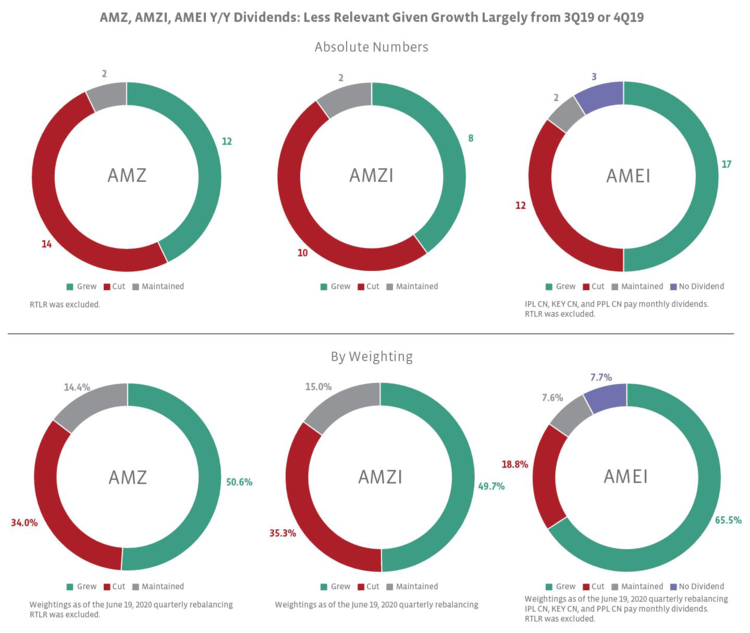

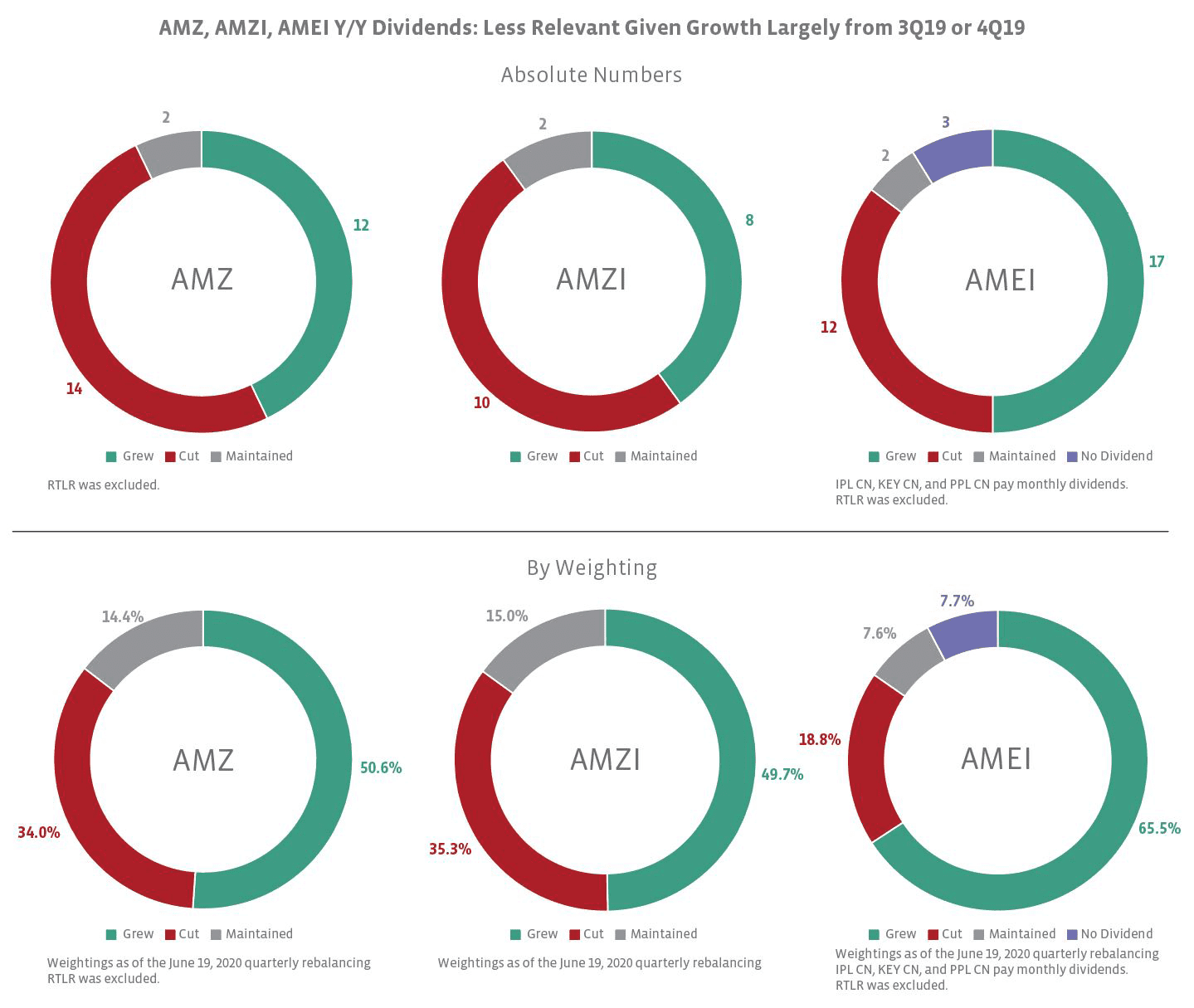

Year-over-year comparison likely less relevant.

Given market headwinds and a fragile recovery, most midstream names are maintaining payouts instead of increasing them. As noted already, HESM, DKL, and CQP are notable exceptions. It also bears noting that Enbridge (ENB) and TC Energy (TRP) typically raise their dividends on an annual basis with the fourth quarter dividend. TRP has guided to dividend growth of 8-10% in 2021 and 5-7% beyond 2021. Given the dramatic change in operating environment from 2Q19 to 2Q20, the year-over-year comparison below is less relevant than in the past; however, it is included for context. The charts below compare the 2Q20 payout with 2Q19 for names in the indexes in both periods. This admittedly introduces survivorship bias. AMZ and AMEI constituent Rattler Midstream (RTLR) was excluded below since its first distribution was for 3Q19. As shown, several constituents have seen in an increase in their payouts on a year-over-year basis, but that is more a reflection of increases in 3Q19 or 4Q19.

Are distribution/dividend cuts firmly in the rearview?

A steady quarter for payouts and an improving macro backdrop (read more) are positives for midstream and are helpful for restoring confidence in the space. Given cuts made earlier this year and firmer footing in terms of fundamentals, the downside risk for midstream payouts overall feels substantially lower yet yields remain stubbornly elevated. As of August 7, the AMZI, AMZ, and AMEI were each yielding 370, 360, and 180 basis points above their respective five-year averages. We continue to view the larger names in the space as well positioned overall to maintain their payouts and see less risk from smaller names given sizable cuts already instituted or significant cash flow stability (or even growth) for some names.

While the downside risk to distributions has diminished in our view, it would be premature to say that the risk of distribution cuts is completely behind the space. On their earnings call on July 31, Phillips 66 Partners (PSXP) indicated that a shutdown of the Dakota Access Pipeline (DAPL) would be cause to evaluate the partnership’s distribution. On August 5, an appeals court ruled that the pipeline could continue operating; however, the court is still evaluating arguments from the Army Corps and DAPL that an environmental review is not needed, which leaves some lingering uncertainty. On its August 5 earnings call after the court’s decision, the management of Energy Transfer (ET) expressed confidence that the pipeline would continue to operate. When asked about the distribution and the company’s investment-grade credit rating, ET’s CFO mentioned that the distribution is a topic when discussing how to reduce leverage with rating agencies. For context, ET’s distribution coverage ratio for 2Q20 was 1.54×. To be fair, these are unique circumstances, but they help inform the cautiously optimistic outlook for distributions going forward.

Bottom Line

Dividend cuts have been prevalent across the energy sector this year, with BP’s (BP) recent announcement of a 50% dividend cut perhaps the latest addition to a long list including Royal Dutch Shell (RDS-A), Halliburton (HAL), and many others. Within this context, it is reassuring to see only one cut across the midstream universe for 2Q20 and from a small MLP at that. Equity yields remain stubbornly high even as the risk of additional distribution cuts seems limited, though some unique situations continue to bear watching. The steady payouts in 2Q are positive, and ongoing stability will likely be conducive to attracting income-seeking investors to this space.

{kind=link}

{kind=link}