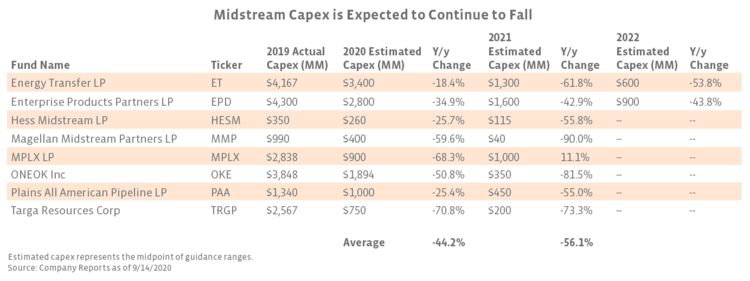

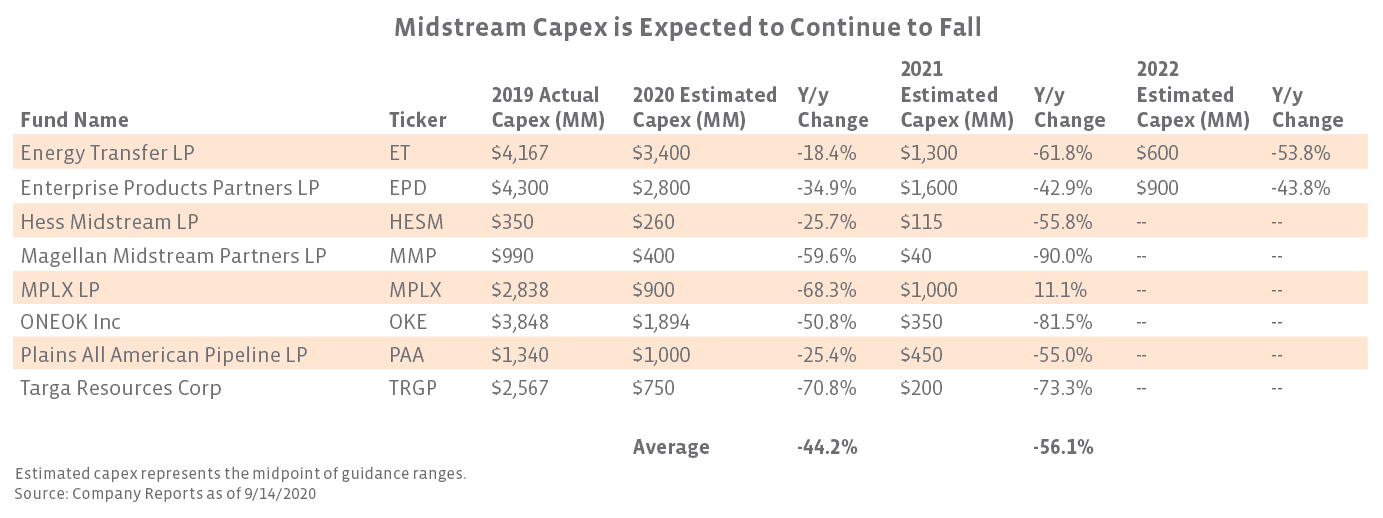

Some names, while not providing firm guidance, have indicated that spending is likely to continue to trend lower going forward. On its 2Q20 earnings call, Kinder Morgan (KMI) indicated that future growth spending would be in line with or below its 2020 expectation of $1.7 billion. This marks a reduction from the $2 – $3 billion capital run rate of recent years. A September presentation from DCP Midstream (DCP) shows a continued sequential decline in total capex in 2021 after a projected 79% decline in growth capital spending this year.

Reduced capital spending will help drive significant free cash flow generation. Some companies have already achieved positive free cash flow after dividends this year, while other names, including MPLX and ET, are targeting free cash flow after distributions in 2021. In the current environment, free cash flow will likely be used to strengthen balance sheets but could also be used to enhance return of capital to shareholders down the road. Going forward, this could represent a tailwind for the sector (read more).

Several projects are nearing completion.

As alluded to earlier, reduced midstream spending is being driven in part by the completion of several capital-intensive projects. Placing these projects in service provides the dual benefit of reducing a company’s capex burden and increasing fee-based cash flows. While COVID-19 may have disrupted plans for added gathering capacity from the wellhead, many midstream projects slated to be placed into service this year have continued to move towards the finish line since, in many cases, these are firmly contracted projects that take years to complete. For example, ET’s Lone Star Express Pipeline Expansion, which will provide NGL transportation capacity in Texas, was completed ahead of schedule in September after initially being announced in late 2018. Targa Resources (TRGP) has already placed several projects into service this year. As of its August earnings release, the company had begun operations its Train 7 fractionator at Mont Belvieu, Peregrine natural gas processing plant in the Permian, and Galena Park liquefied petroleum gas (LPG) export facility expansion in 2020. TRGP also expects to place its Train 8 fractionator at Mont Belvieu into service this quarter followed by the Grand Prix NGL pipeline early next year. OKE has also completed a slate of NGL-focused projects so far this year including the West Texas LPG pipeline expansion, the Arbuckle II NGL pipeline, and the MB-4 fractionator in Mont Belvieu.

Several other major projects are expected to come online in 2021. In September, KMI stated that its 2 billion cubic feet per day (Bcf/d) Permian Highway natural gas pipeline is nearly complete with only 11 miles of the 430-mile project left to be constructed. The company expects the line to be fully in service by early 2021 and, while a final investment decision has not been made yet, has discussed constructing a third 2 Bcf/d Permian natural gas pipeline later in the decade. Cheniere Energy (LNG) expects to place the third liquefaction train at its Corpus Christi facility into service during the first half of 2021 after noting over 90% completion in August. Equitrans Midstream (ETRN) is targeting an early 2021 in service date for its Mountain Valley Pipeline (MVP). Additionally, ETRN also expects to start-up the MVP Southgate project, which is a 75-mile extension of MVP into North Carolina, sometime in 2021. Project backlogs can also help frame midstream growth and underscore the long-term demand for energy infrastructure. Enbridge (ENB) has secured $11 billion (CAD) of growth projects, and TC Energy (TRP) has outlined $37 billion (CAD) of projects through 2023, $11 billion of which are currently underway. KMI’s $2.9 billion backlog, which includes the previously mentioned Permian Highway pipeline, has a 71% concentration in natural gas projects, with natural gas representing a relative bright spot in energy lately (read more).

How can midstream grow going forward?

With capex budgets declining and capital discipline in focus, many investors have raised questions regarding the potential for further growth among energy infrastructure companies. While the growth opportunity set may be shifting away from long-haul pipelines, there are still several avenues through which midstream companies can expand going forward. Additionally, the need for growth may not be as dire as it has been previously. The MLP business model has shifted from a singular focus on distribution growth supported by incentive distribution rights (read more) to a model more focused on sustainable distributions, total return, and free cash flow generation. Capital budgets will likely remain well below peak levels seen in 2018/19, but this does not necessarily equate to an absence of growth opportunities. More moderate growth is positive for free cash flow generation (read more).

As companies move away from longer, capital-intensive interstate pipelines, additional pipeline capacity needs will increasingly be met with capital efficient enhancements to existing infrastructure such as adding pump stations or short extensions of existing pipelines. After the cancellation of Dominion Energy (D) and Duke Energy’s (DUK) Atlantic Coast Pipeline in July, WMB stated that it is well positioned to meet transportation demand on the east coast through incremental low-cost additions to its existing infrastructure. MMP’s $40 million of expansion spending planned for next year is focused on “small, low-risk bolt-on projects.” NGLs, which are expected to see growing production in the US in the Energy Information Administration’s forecast period through 2021 despite oil production declines, could present opportunities for midstream companies to build transportation, fractionation, or export capacity (read more). Other export infrastructure could also be required as US production recovers given growing global demand for energy. ET took over development of the Lake Charles LNG export project in March, and EPD is seeking government approval for its Sea Port Oil Terminal off the coast of Texas, which is not currently included in capex forecasts.

Midstream also has opportunities beyond pipeline expansions and export terminals. Petrochemicals are another potential growth area for midstream given the natural fit with existing operations, particularly around NGLs. Inter Pipeline (IPL) has continued to advance construction of its $4 billion (CAD) Heartland Petrochemical Complex this year even while searching for a project partner, and EPD continues to build out its second propane dehydrogenation plant (PDH-2). Finally, energy infrastructure companies could invest in renewable energy. ENB already has enough renewable power generation to meet the needs of 900 thousand homes, and WMB has a $400 million initiative to invest in solar installations across its footprint (read more).

Bottom Line

Midstream management teams have been prioritizing capital discipline for some time, which has been further enforced by the ongoing impacts of COVID-19 on energy markets and the need for financial flexibility. Lower discretionary spending with a focus on high-return projects can help drive free cash flow generation while enhancing balance sheet strength. Going forward, there are several areas of opportunity for continued midstream growth, but capital spending will likely remain below the levels seen in the late 2010s as the need for growth moderates due to changing trends in production and an evolved midstream business model.

{kind=link}