Despite these metrics trending in the right direction, yields have increased. While the leverage improvement may not seem dramatic, its bears noting that large MLPs Enterprise Products Partners (EPD), Magellan Midstream Partners (MMP), and Plains All American (PAA) have reduced their leverage each year since 2016, and all had 2019 leverage below 3.2×.

As detailed earlier this week, MLP distribution coverage and midstream payout ratios are at comfortable levels, providing some peace of mind to investors. For MLPs, distribution cuts over the years have helped bolster these metrics, but painful lessons from the past have led to a greater focus on sustainable distributions. From a C-Corp perspective, it bears noting that Canadian midstream corporations – Enbridge (ENB), TC Energy (TRP) Inter Pipeline (IPL), Keyera (KEY) and Pembina Pipeline (PPL) – boast a strong dividend track record and did not cut their dividends in the aftermath of the oil price decline that begin in 2014 (read more). On average, these companies are only down 3.7% year-to-date through March 3 on a price-return basis in keeping with their more defensive nature.

Another factor contributing to midstream’s improved positioning for today’s market challenges is the general decline in growth spending that is underway (read more). The benefit is twofold: 1) Midstream companies are reaping the cash flows from projects that were recently completed, and 2) midstream has greater flexibility when it comes to capital allocation. On the first point, out of 29 midstream MLPs and C-Corps with 2020 EBITDA guidance, 15 companies are guiding to double-digit percentage EBITDA growth in 2020 compared to 2019, which includes both MLPs and larger corporations like ONEOK (OKE) and Targa Resources (TRGP). Midstream’s transition over the last few years away from using equity capital to fund growth projects is another positive relative to the past.

Do upstream headaches mean midstream headaches?

As discussed above, midstream companies have worked to limit commodity price exposure, but their customers, particularly exploration and production companies (E&Ps), can be at the mercy of commodity markets, with some potential protection from their hedge books. In our view, the most recent downtrend in WTI oil prices from the low $50s to the high $40s per barrel over the last two weeks has probably not yet impacted producer plans. In other words, oil has not been low enough for long enough for producers to respond. That said, producers are clearly watching the markets and especially the OPEC and non-OPEC meetings taking place this week (discussed below), and capital discipline is a focus for E&Ps. If prices remain in the mid-$40s for a period of weeks, producers may further reduce activity, which could have impacts on midstream volumes. However, midstream contracts typically include minimum volume commitments (MVC) or take-or-pay features to protect the midstream company.

On the natural gas side, there have been some contract adjustments announced already for midstream companies with a single major customer. In December, Antero Midstream (AM) announced a growth incentive fee program with Antero Resources (AR) under which AM provides lower fees for 2020-2023 conditional upon AR achieving volume targets. As part of its broader announcement last week that included Equitrans (ETRN) acquiring EQM Midstream (EQM), EQM announced a new 15-year gathering agreement with EQT Corporation (EQT) that provided fee relief but also extended the contract and increased the MVC. The result was a $2.1 billion increase in the present value (using a 10% discount rate) of MVC revenue. In 2015 and 2016, producers and midstream providers restructured contracts in mutually beneficial ways (read more). History could repeat itself if E&Ps are squeezed financially.

Despite near-term demand concerns, the long-term outlook is positive.

While global oil demand is being pressured by the impact of the coronavirus today, the world will need US oil and natural gas in the years ahead. Estimates for the oil demand impact from coronavirus vary, with IHS Markit estimating a 3.8 million barrel per day (MMBpd) or ~3.8% decline in 1Q20 demand compared to 1Q19 this week. In mid-February, the International Energy Agency (IEA) had forecasted a 0.44 MMBpd decline in 1Q20 demand and had projected full-year demand growth of 0.8 MMBpd, though clearly much has changed since mid-February and numbers will likely be adjusted with the next Oil Market Report scheduled for March 9. Today, OPEC estimated that full-year 2020 oil demand would increase by 0.48 MMBpd but noted that the risk is biased to the downside. Admittedly, estimating demand impacts is largely speculation at this point, but until there is more clarity surrounding coronavirus, the risk remains for downward revisions.

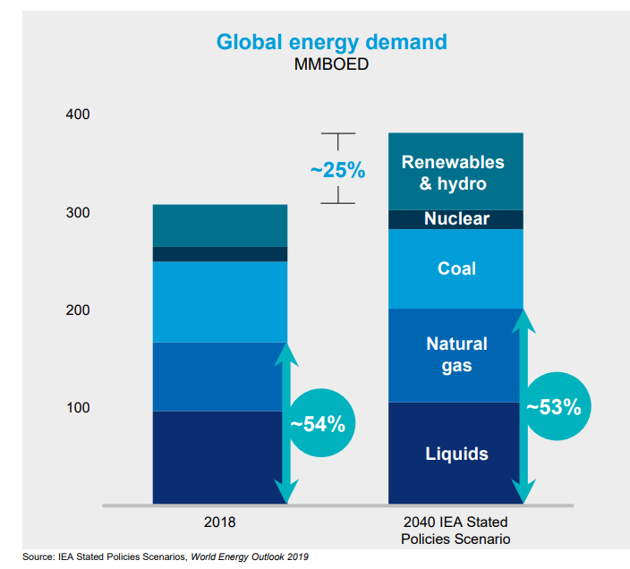

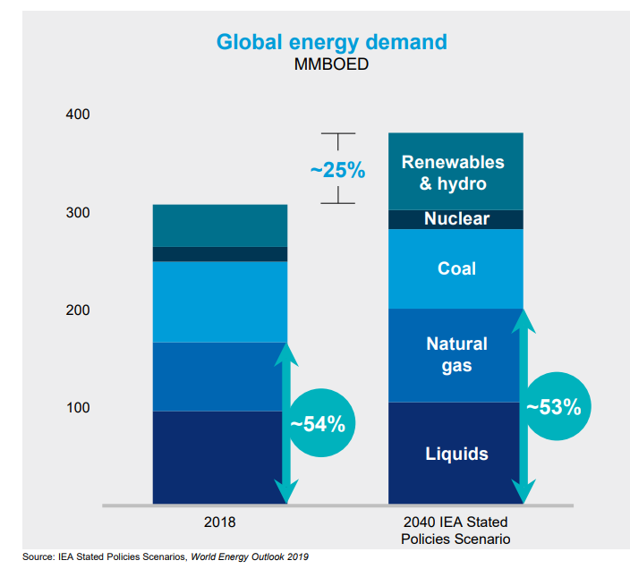

Taking a longer-term view, under the Stated Policies Scenario of the IEA’s World Energy Outlook 2019, which incorporates existing policies and announced policy plans, the US would account for 85% of the growth in global oil production and 30% of the growth in worldwide natural gas production through 2030. To provide a more pointed example, on Tuesday, Chevron (CVX) unveiled expectations for sustained Permian production above 1 million barrels per day through 2040 with relatively flat activity. The same IEA report forms the basis for the chart below, which shows energy demand increasing by 25% from 2018 to 2040 with liquids (petroleum) and natural gas representing a similar share of the energy mix. While it is admittedly difficult to look beyond today’s uncertainty, the long-term expectation is that midstream companies will play a vital role in connecting US energy with global demand and will increasingly generate significant free cash flow as growth spending subsides (read more).

Source: Chevron Analyst Day Presentation

What are potential near-term catalysts or positives?

Additional buyback announcements or execution on existing programs. Midstream companies with buyback programs in place include Antero Midstream (AM), Cheniere (LNG), Enterprise Products Partners (EPD), Kinder Morgan (KMI), Magellan Midstream Partners (MMP), and NGL Energy Partners (NGL). More companies have discussed the potential for buybacks, with some framing repurchases as more of a 2021 event. With equity values where they are today, buyback plans could be brought forward, or those with programs may accelerate repurchasing activity.

Insider buying. In volatile markets, management teams buying shares/units represents an important vote of confidence in their companies. To state the obvious, there’s only one reason management teams buy shares – because they think they will be worth more in the future. There has been considerable insider buying at Energy Transfer (ET), Kinder Morgan (KMI), Genesis Energy (GEL), Plains All American (PAA/PAGP), and Noble Midstream (NBLX) over the last two weeks.

OPEC+ meeting. OPEC hosted an extraordinary meeting today and will meet with non-OPEC counterparts tomorrow. Oil prices have rebounded from their lows leading up to the meeting, given headlines regarding Saudi Arabia’s push for larger production cuts (example). OPEC announced today that it will recommend an additional 1.5 MMBpd cut through 2Q20 to the OPEC and non-OPEC representatives meeting tomorrow (1.0 MMBpd from OPEC and 0.5 MMBpd from non-OPEC), which would bring total cuts to 3.6 MMBpd. Media reports have indicated that Russia’s cooperation with the deeper cuts still needs to be determined. An improvement in oil prices coming out of tomorrow’s meeting could be helpful for E&Ps and reduce the need to adjust activity from an oil production standpoint. However, if Russia does not agree, oil prices could fall, or even if Russia cooperates, oil prices could fall on a sell-the-news trade.

Private equity transaction. When the buyout of Buckeye Partners was announced in May 2019, the transaction highlighted the disconnect between how public markets and private equity value midstream assets, while also providing credibility to the argument that private equity may help keep public market valuations honest (read more). Pressured midstream valuations and the volatility in commodity prices, which complicates valuation discussions for producing assets, may steer energy-focused private equity shops toward midstream instead of upstream. A buyout or asset-level transaction at an attractive multiple may resonate with public market investors.

Bottom line

The positive fundamentals in the midstream space are likely to take a backseat to developments related to the coronavirus. It is admittedly too early to tell whether the coronavirus will actually impair those fundamentals and the portion of 2020 EBITDA growth guidance that may be at risk, if any. On the bright side, the midstream space is better positioned for a downturn today thanks to lessons learned in 2014-16, and midstream investors are being paid attractive dividends in the meantime, as the 10-year Treasury yield sits below 1.0%.

{kind=link}

{kind=link}