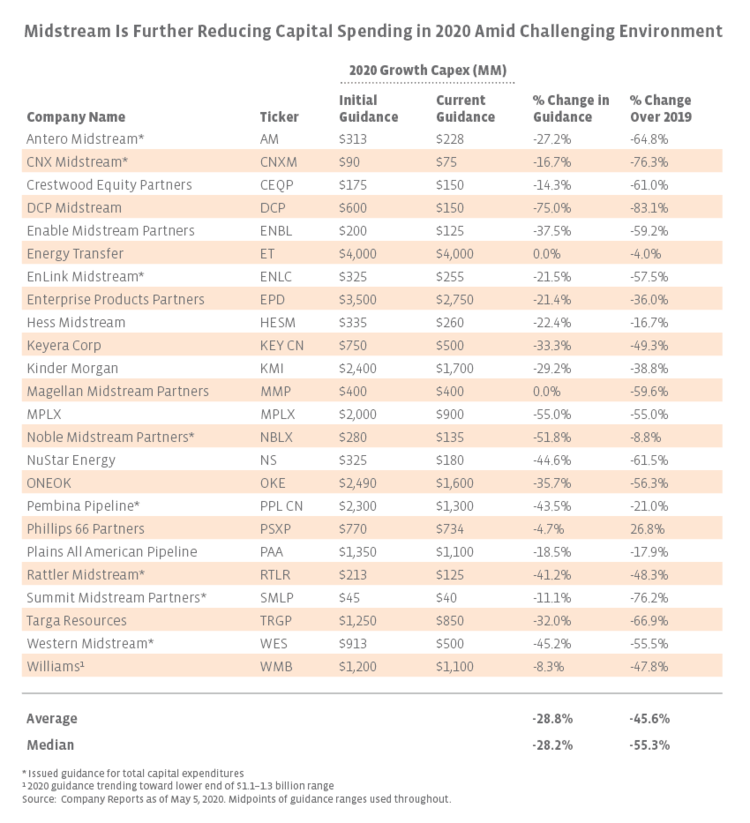

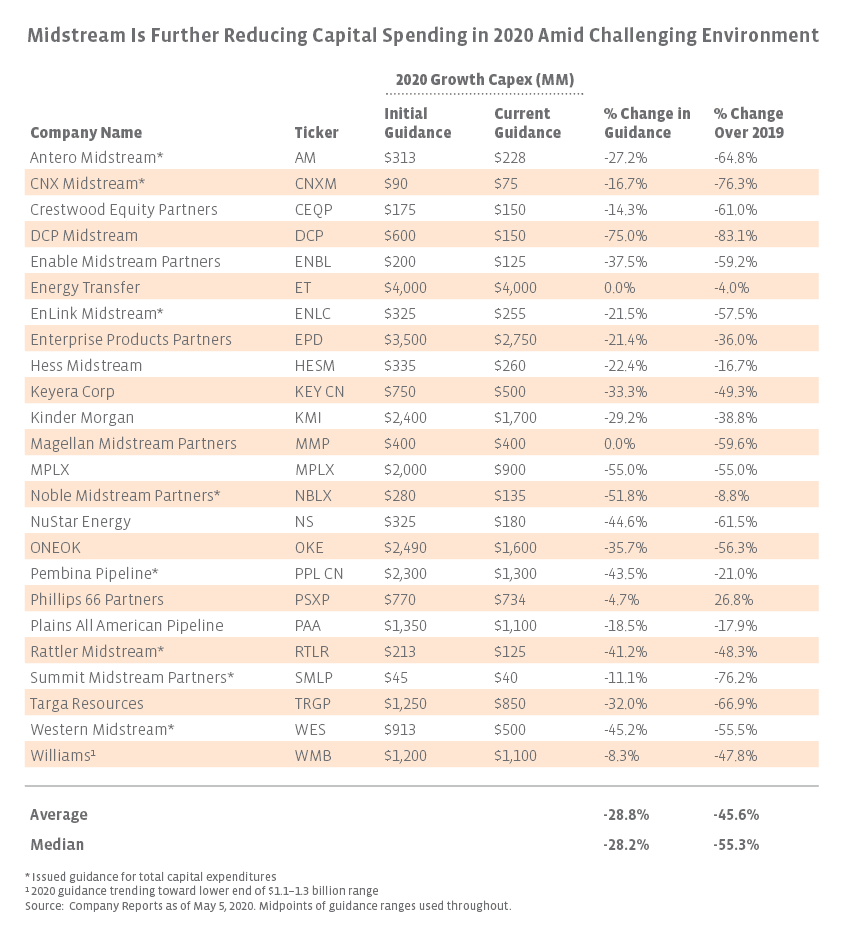

Companies across midstream are lowering capital budgets, representing a diverse array of business lines and basins. Energy Transfer (ET) and Magellan Midstream Partners (MMP) stand out in the table for not reducing 2020 spending guidance, but the table does not tell the full story. ET, which reports earnings next week, previously indicated that it is evaluating $500 million in projects that could be delayed to 2021-2022 and expects its long-term capex run-rate (2021+) to decrease to $2.25 billion per year at the midpoint from $4.0 billion in 2020. MMP maintained its initial $400 million growth capex budget, but 2020 spending was already modest compared to MMP’s $792 million of growth spending in 2019. The majority of MMP’s capital spending in 2020 is related to its refined products business and backed by long-term contracts with investment-grade counterparties.

Looking more closely at projects, companies have evaluated spending on a case-by-case basis. Projects of all types near completion are more likely to be finished than deferred, while projects under development with completion dates in 2021 or later are at greater risk of being deferred or canceled. For example, Phillips 66 Partners (PSXP) said it had commenced full operations on the Gray Oak Pipeline, a newbuild crude pipeline transporting up to 900 thousand barrels per day (MBpd) from the Permian to the Corpus Christi area, on April 1. However, it also announced it would defer the Liberty Pipeline, a crude pipeline from Wyoming to Cushing previously expected to begin service in 1H21, and postponed a final investment decision on the ACE crude pipeline in Louisiana. Three other notable Permian pipelines with construction already in progress, the one-million barrel-per-day Wink to Webster crude pipeline, Kinder Morgan’s (KMI) Permian Highway gas pipeline project, and MPLX’s (MPLX) Whistler gas pipeline continue to progress toward completion in 1H21, early 2021, and 2H21, respectively.

Cancellations and deferrals have not been limited to a single midstream asset type or region, indicating that depressed commodity prices are being felt broadly. OKE’s reduced spending, for instance, includes project deferrals across the Bakken, Permian, Gulf Coast, and Mid-Continent. Enterprise Products Partners (EPD) canceled or deferred spending on 13 projects, including the Midland-to-ECHO 4 Permian crude pipeline, PDH 2 plant, and Mont Belvieu isomerization plant. EPD management noted that the company is currently negotiating six joint ventures that could lead to further spending reductions.

With weaker commodity prices changing the outlook for energy production and the demand for new infrastructure, midstream is responding appropriately by recalibrating capital spending. Reduced spending this year can help provide the flexibility needed to withstand short-term headwinds by freeing up cash, while also decreasing the odds of an overbuild of infrastructure as volumes recover.

Company Guidance Updates:

Antero Midstream (AM)

CNX Midstream (CNXM)

Crestwood Equity Partners (CEQP)

DCP Midstream (DCP)

Enable Midstream (ENBL)

Energy Transfer (ET)

EnLink Midstream (ENLC)

Enterprise Products Partners (EPD)

Hess Midstream (HESM)

Keyera (KEY CN)

Kinder Morgan (KMI)

Magellan Midstream Partners (MMP)

MPLX (MPLX)

Noble Midstream Partners (NBLX)

NuStar Energy (NS)

ONEOK (OKE)

Pembina Pipeline (PPL CN)

Phillips 66 Partners (PSXP)

Plains All American Pipeline (PAA)

Rattler Midstream (RTLR)

Summit Midstream Partners (SMLP)

Targa Resources (TRGP)

TC Energy (TRP CN)

Western Midstream (WES)

Williams (WMB)

{kind=link}