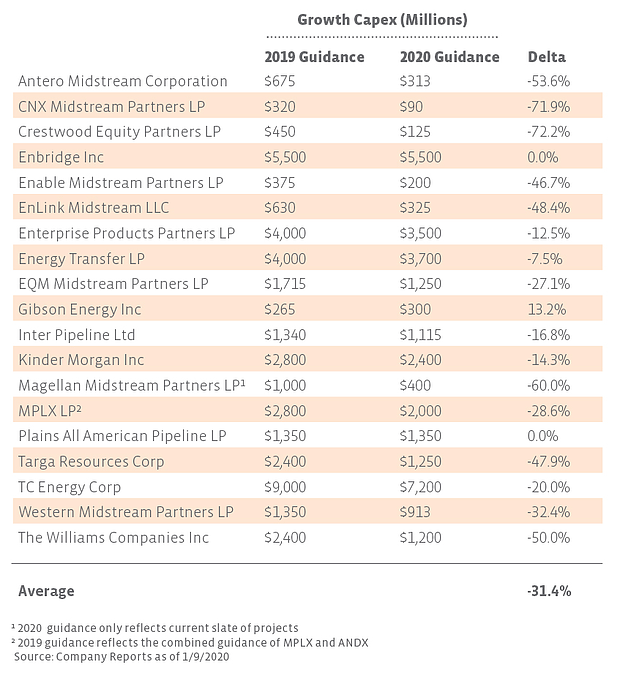

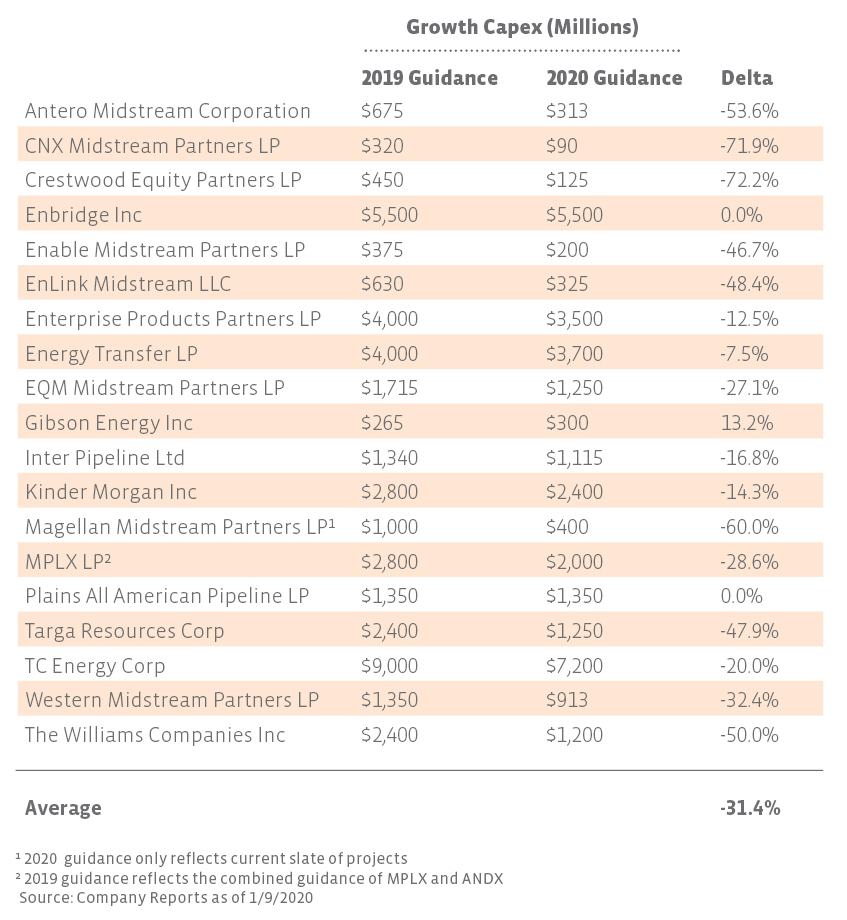

While cuts are the prevailing trend, there are a few companies that are increasing or maintaining spending levels in 2020. Gibson Energy (GEI), a Canadian crude storage company, expects a 13.2% increase in growth capex primarily driven by spending on an expansion of its Hardisty Terminal. Plains All American (PAA) expects 2020 spending to be flat with 2019 due to its Red Oak, Capline, and Wink-to-Webster pipeline projects. However, the partnership expects material reductions to its capital spending in 2021 and beyond once these projects are completed.

Lower capex a key ingredient for free cash flow generation

As a result of reduced capex and the additional cash flows from newly completed projects, midstream companies are nearing a free cash flow inflection. For the purpose of this piece, free cash flow is defined as cash flow from operations after capital expenditures and dividends. A vast majority of the industry is currently not generating positive free cash flow, even with the expected reductions in capex this year. However, a handful of midstream MLPs and corporations are targeting positive free cash flow for the first time in 2020. Crestwood Equity Partners (CEQP), which is slashing its growth capex by over 70% this year, expects to become free cash flow positive in the first half of the year. CNX Midstream Partners (CNXM) is guiding to $130 million of free cash flow before distributions for 2020 driven by recent project completions and reduced capital spending. Incorporating CNXM’s 15% distribution growth guidance for 2020, the partnership may also be free cash flow positive after its distribution payments. Finally, at its December 2019 Analyst Day, The Williams Companies (WMB) announced that it expects to deliver positive free cash flow in 2020, even without the aid of proceeds from asset sales. Additionally, WMB will not need to access debt or equity markets to fund its growth capital or dividend.

While a few energy infrastructure operators are set to reach a free cash flow inflection point in 2020, more could potentially follow suit in 2021. Once the long-delayed Line 3 Replacement project is completed, Enbridge (ENB) expects to generate $3 to $4 billion of post-dividend free cash flow annually. The US portion of Line 3 is currently slated to enter service in 2H20. On its most recent earnings call, MPLX (MPLX) management emphasized its disciplined approach to capital spending and desire to grow free cash flow, backed up by its $600 million reduction to 2020 growth capex guidance relative to guidance from the December 2018 Investor Day. If management teams continue to prioritize capital discipline, these improved cash flow profiles could become the norm for the industry.

How can investors benefit?

With free cash flow generation on the horizon, investors stand to benefit in a few key ways. Free cash flow generation implies that midstream companies will have more means to return capital to shareholders to supplement their already substantial yields. Share buyback programs have continued to become an increasingly common topic of discussion for management teams (read more). Buyback programs have been rare so far due to limited free cash flow and plenty of growth opportunities that offer high returns. At its 2019 Investor Day, ENB restated its commitment to growing its dividend, but noted that it will more actively consider buybacks once Line 3 in placed into service. Some names, such as Kinder Morgan (KMI) and Enterprise Products Partners (EPD) have buyback programs in place, while others have discussed the potential for buybacks on recent earnings calls, including Energy Transfer (ET) and WMB. Additionally, midstream companies could use excess cash flows to raise their dividends. In recent investor presentations, CEQP noted that free cash flow will allow for distribution increases or unit buybacks this year, and MMP discussed potentially using a special distribution or unit buybacks to return capital to shareholders.

Free cash flow could also be used to enhance balance sheets. Most companies have already made strides to reduce leverage, but excess cash flows could be used for further improvements. During CEQP’s 3Q19 earnings call, CEO Robert Phillips stated that reducing capex and generating free cash flow for the first time will allow the partnership to achieve sub-4x leverage in 2020. In general, companies would be expected to prioritize balance sheet health and leverage targets before pursuing buybacks or dividend increases.

Bottom line

Significant declines in 2020 capital spending likely signal the end of a period of breakneck growth for midstream infrastructure and a shift towards harvesting cash flows as major projects come online. The combination should drive a free cash flow inflection this year and next, which paves the way for shareholder-friendly returns and continued balance sheet improvements – positives that should not go unappreciated by the market.

{kind=link}