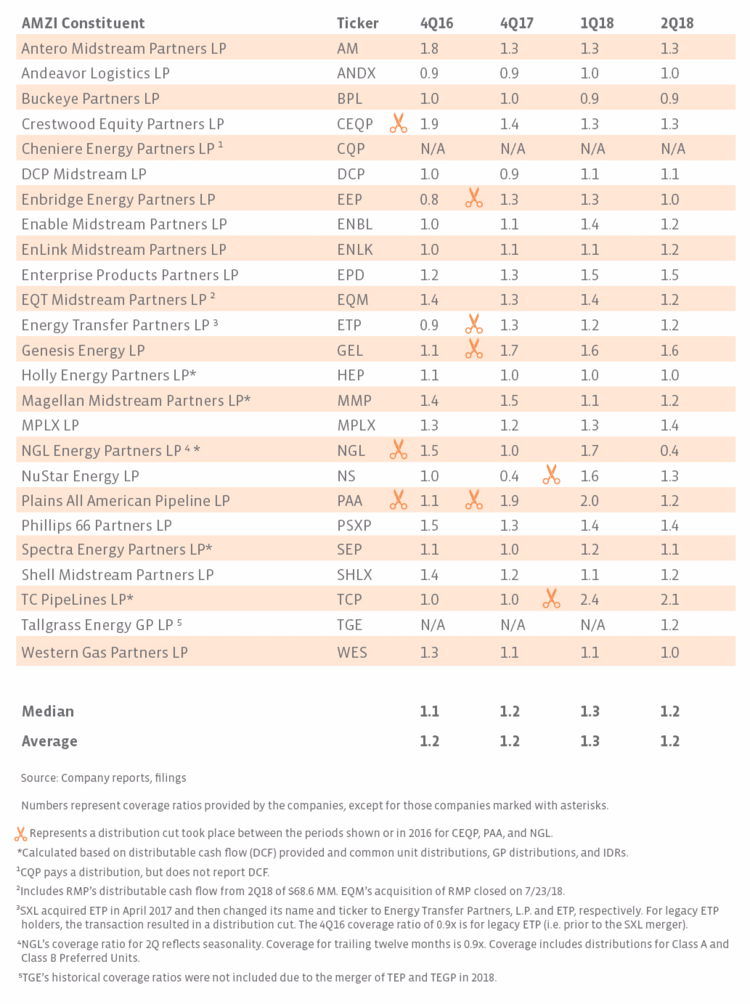

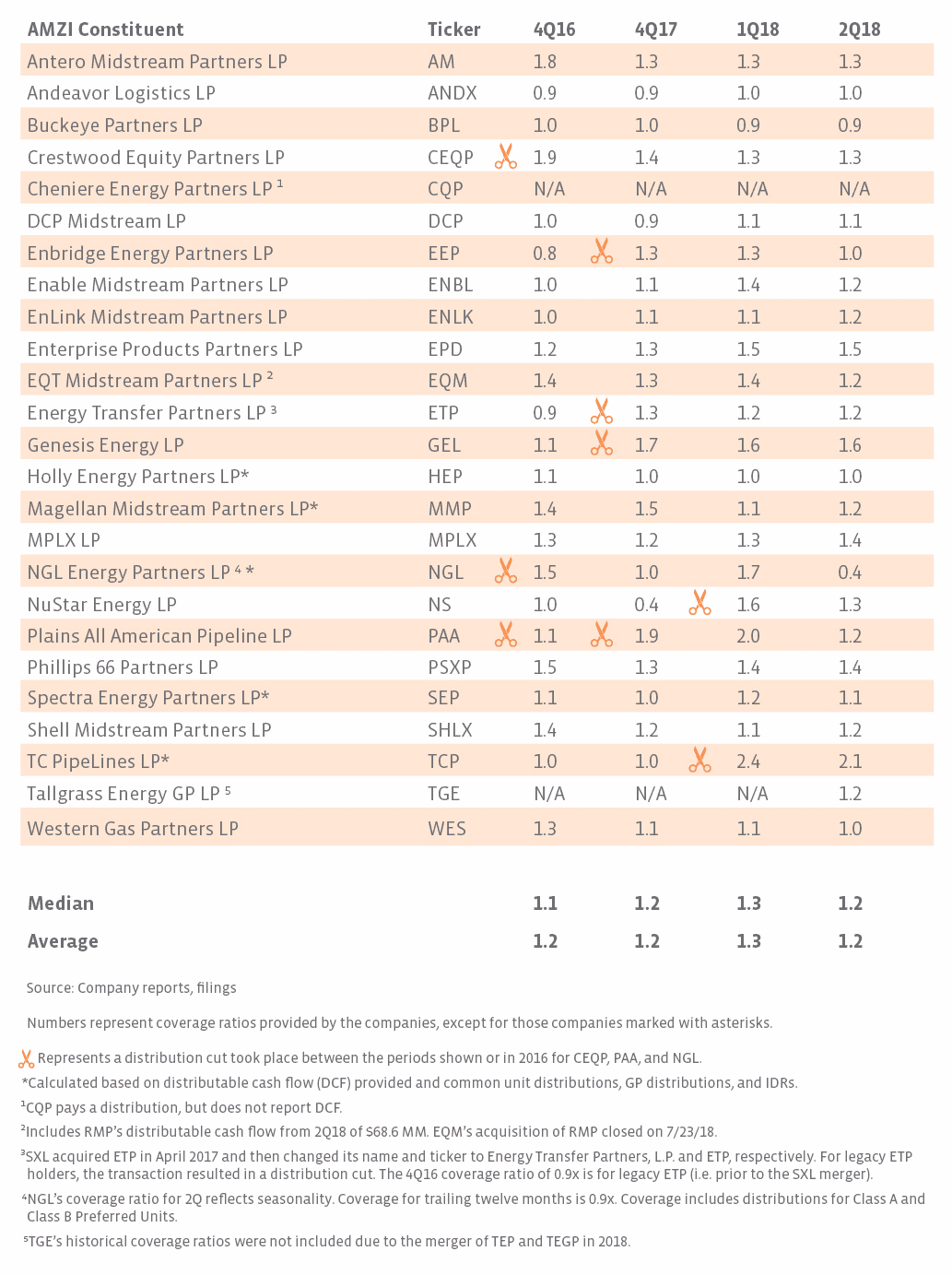

What are the takeaways for the group more broadly?

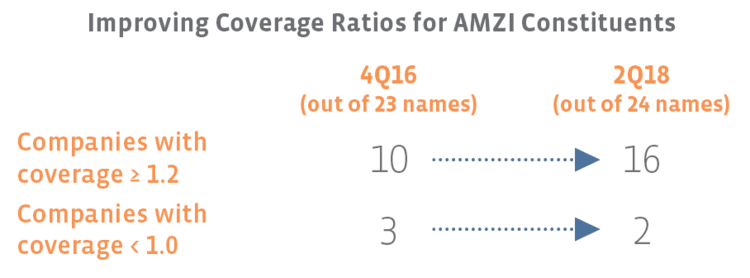

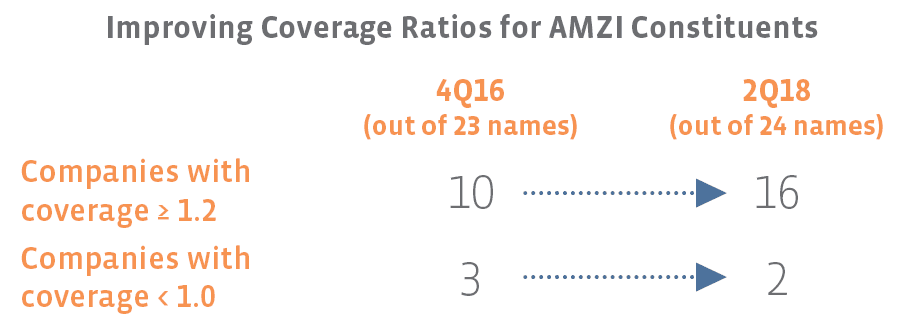

Comparing 4Q16 to 2Q18, the average for this group has remained steady, while the median has slightly improved. That said, the data below seems more telling of the improvement for the group. In summation, the number of companies with coverage of 1.2x or better has increased from 4Q16, while the number of names with coverage below 1.0x has decreased. For investors, these numbers are both trending in the right direction in terms of providing more comfort around the ability of these MLPs to pay their distributions or increase them. The table above shows the simple average for each quarter, but the weighted average coverage ratio for 2Q18 is also 1.2x based on the index weightings as of the August 10th special rebalancing.

Cautions to keep in mind

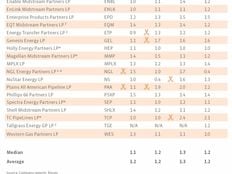

As a metric that does not comply with Generally Accepted Accounting Principles (GAAP), MLPs have latitude in how they calculate DCF. Among different MLPs, DCF may not be calculated in the same way, implying that the coverage ratios shown are not all apples to apples. That said, comparing coverage ratios over time for the same company should provide a clear comparison for that individual company. For businesses with seasonality, coverage may fluctuate between quarters making an annual or trailing 12-month coverage ratio more meaningful. As noted in the table, NGL Energy Partners’ (NGL) trailing 12-month coverage ratio is 0.9x – much higher than the 0.4x shown for 2Q18. NGL has moved to reduce the seasonality of its business with the sale of its retail propane business, which closed last month.

Rounding coverage to the tenths place also smooths the data. However, we think presenting the data to the hundredth place implies more accuracy for the data broadly than is warranted given the caveats mentioned above, namely that DCF is not a standard measure.

Bottom line

Looking at the current AMZI constituents, distribution coverage has generally improved from 4Q16 to 2Q18, though in some cases that improvement was the result of painful cuts to lower the distribution to a more sustainable level. Each MLP’s coverage trends are somewhat unique, whether coverage was steady, decreased due to distribution growth, or coverage improved because of cuts, a shift to self-funding, or an effort to be more conservative. However, for MLP investors, the improvements discussed or the absolute numbers for 2Q18 hopefully help address concerns about coverage and the ability of MLPs to pay and potentially grow their distributions.

{kind=link}

{kind=link}