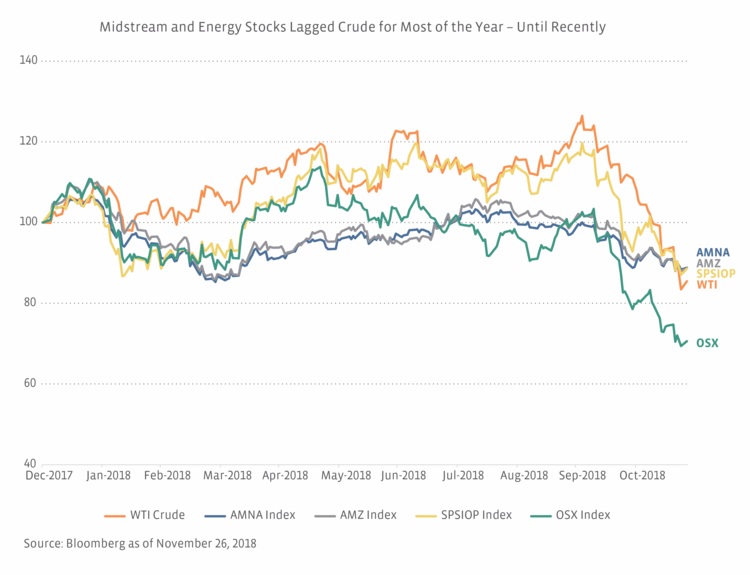

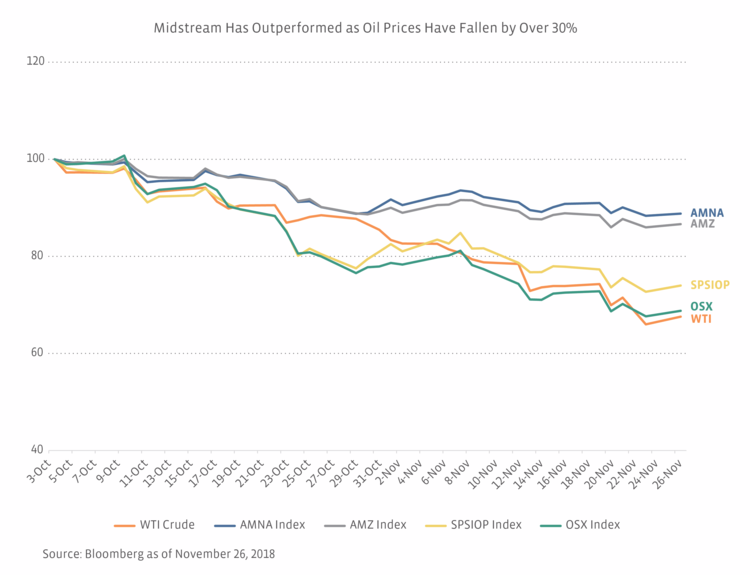

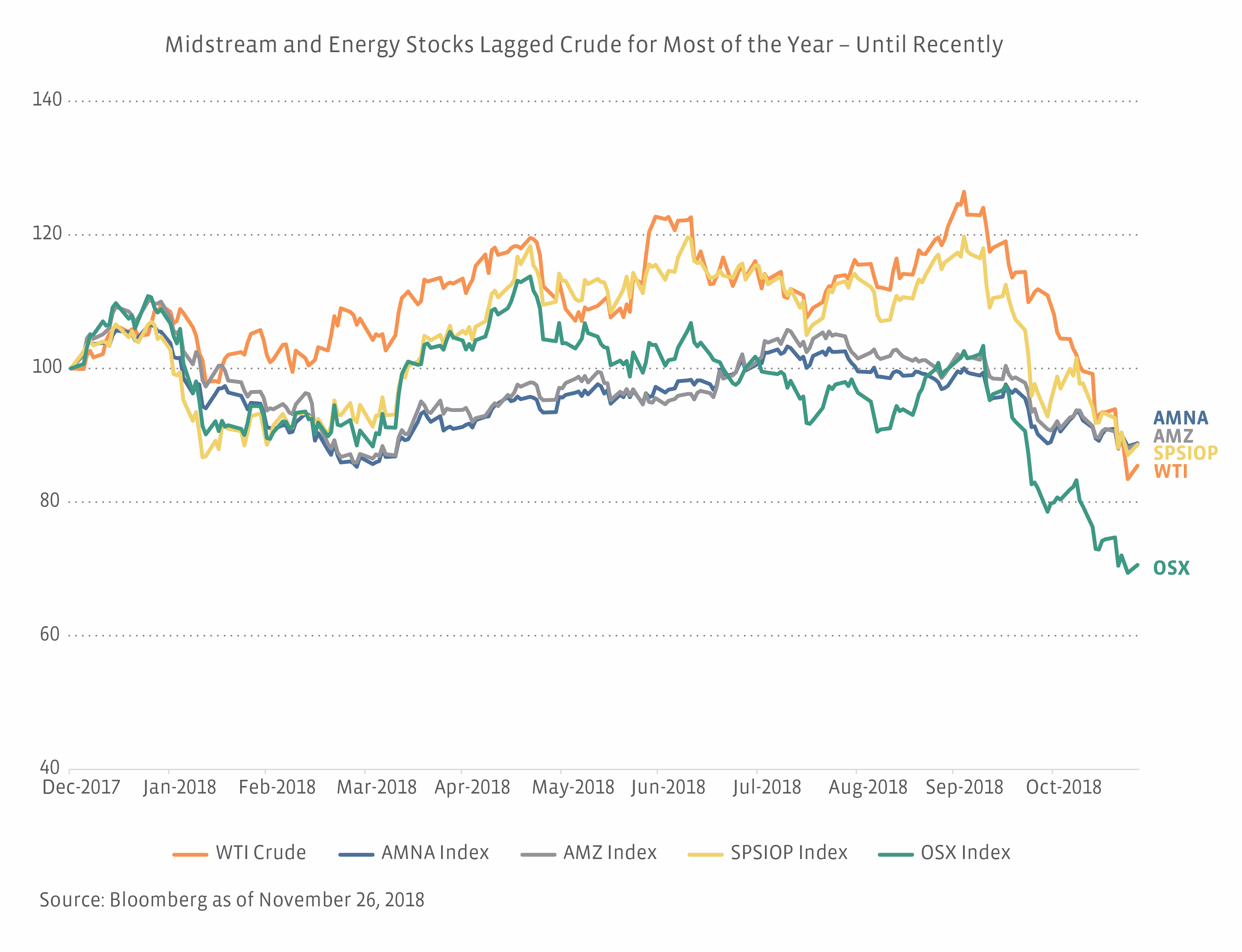

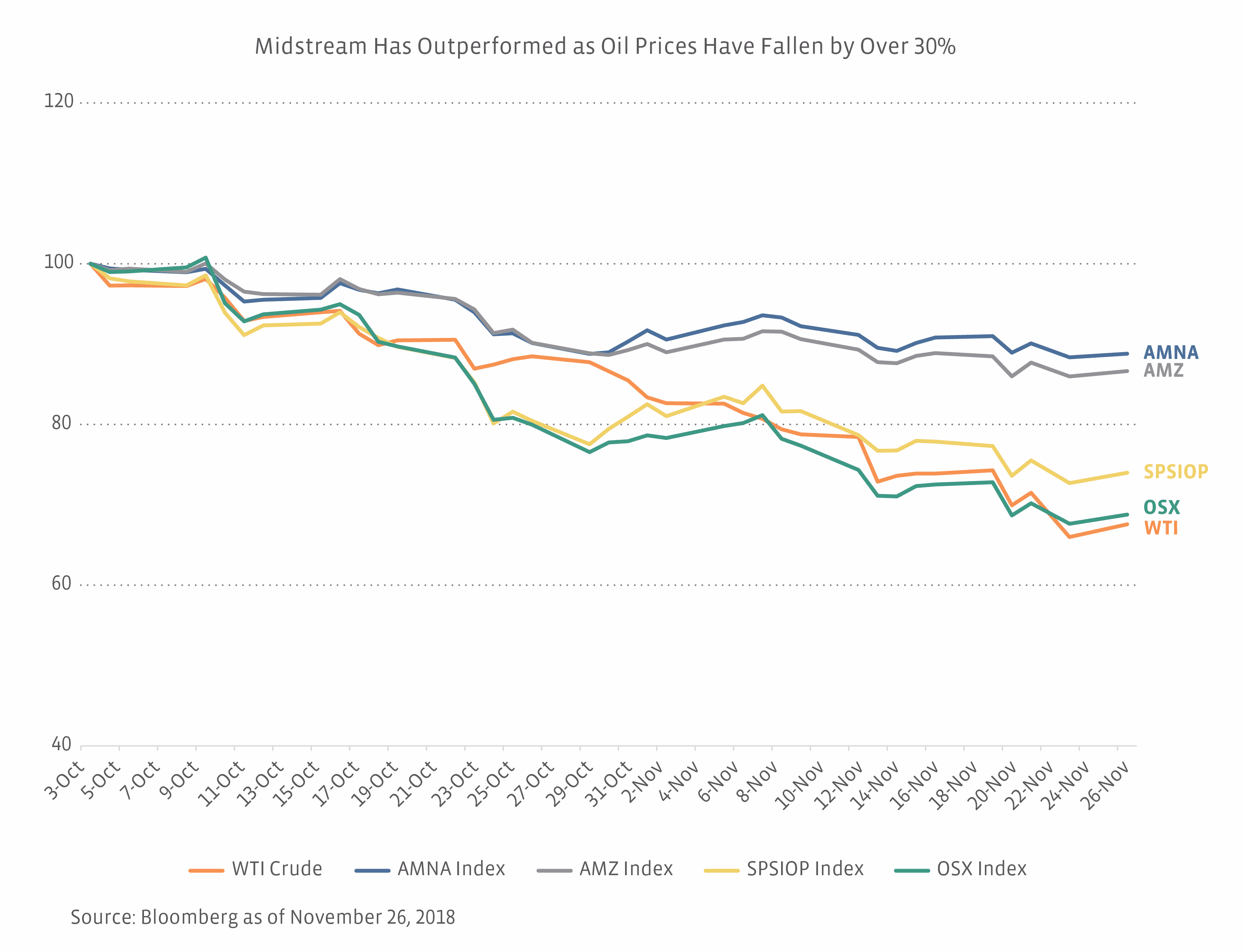

As an explanatory note, in the chart, we use the AMZ and AMNA to represent MLPs and midstream, respectively. We compare performance with the S&P Oil & Gas Exploration & Production Select Industry Index (SPSIOP) as a proxy for E&P companies and the PHLX Oil Service Sector Index (OSX) as a proxy for oilfield service companies.

It may feel like ancient history now, but WTI crude closed above $76 per barrel on October 3. Since then, oil prices have declined more than 30% through November 30, dragging down energy stocks. The midstream space has been negatively impacted, but it is holding up much better than its energy counterparts, as shown below. Setting aside price performance, the yield on the AMZ and AMNA was 8.3% and 6.4% as of November 30. We would expect midstream to be more defensive in a falling price environment, and that is holding true.

Why has midstream held up (besides the nature of the business)?

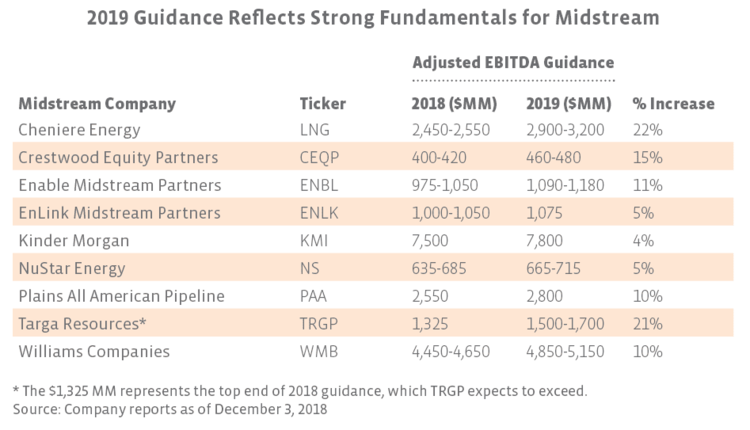

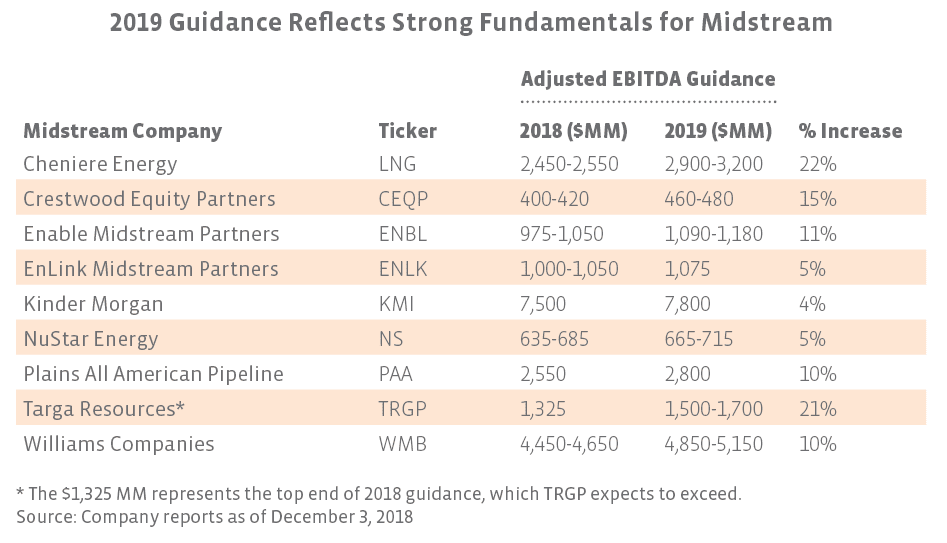

MLPs and midstream are more defensive by nature of their fee-based business models, but other factors have been supportive as well. Record high (and growing) US oil and natural gas production is positive for the space as largely volume-driven businesses. Oil price weakness has in part been a function of the rapid growth in US oil production, which was up nearly 2 million barrels per day (MMBpd) year over year to 11.5 MMBpd in September 2018. As we have discussed in the past, production growth creates more demand for new energy infrastructure assets and supports high utilization on existing assets. Inadequate takeaway capacity has led to widened crude differentials in several regions. Solid 3Q earnings results and positive outlooks for 2019, as shown below, further differentiate midstream from its more commodity-sensitive peers involved in production.

Beyond fundamentals, the removal of some uncertainty for specific companies is positive and bodes well for attracting potential investors to midstream broadly. Uncertainty has been an overhang for companies discussing structure changes and for MLPs where distribution cuts were anticipated. Resolution of those issues in the form of firm announcements provides helpful clarity to investors.

Additionally, we continue to see midstream asset sales (often to private equity firms) at attractive multiples, which highlights the value of these underlying assets. For example, First Reserve recently agreed to buy Dominion Energy’s (D) 50% stake in Blue Racer Midstream at a 14-16xmultiple of estimated 2018 EBITDA. Similarly in August, SemGroup (SEMG) announced the sale of a 49% interest in the Maurepas Pipeline to Alinda Capital Partners at a multiple of 13x EBITDA. For context, the weighted average forward EV/EBITDA multiple for the Alerian MLP Infrastructure Index (AMZI) constituents was 10.2x as of November 30.

Where do we go from here?

Continued oil price weakness is a risk and would be negative for the midstream space in terms of both investor sentiment and duration, especially if the weakness persists long enough to slow production growth. WTI at Cushing is trading around $53/bbl, but benchmark prices are in the mid-$40s in the Permian and the Bakken due to inadequate takeaway capacity (read more). We think any significant production response (i.e. a decline not just due to winter weather) would be a matter of months rather than weeks, assuming oil prices continue to weaken. For reference, WTI Midland crude, the Permian benchmark, averaged just under $46/bbl for May through September 2017, and production grew by 200,000 barrels per day from May to September. History would suggest that Permian production can grow in a mid-$40s oil price environment.

Could lower prices be a risk for pipelines under construction? MLPs and midstream companies build pipelines with firm commitments for capacity that will support a desired return. Spot shipments (shipments made ad hoc or without long-term commitments) could be impacted, but those are really icing on the cake. Spot shipments are like getting $55 for your birthday from your grandparents instead of the $50 they have given you for prior birthdays – a pleasant surprise that you weren’t budgeting. Keep in mind the addition of new takeaway capacity would support pricing in producing regions to the benefit of producers, improving their netbacks.

We would be remiss if we did not acknowledge the significant gains in natural gas prices as oil prices have fallen. Since early October, Henry Hub natural gas has gained more than 30%. The price increase reflects seasonality and low gas inventories entering winter, among other factors. While improving natural gas prices don’t hurt, we don’t think the price rise has been the determining factor in MLP and midstream outperformance.

Bottom Line

Midstream is more defensive than other sectors of energy because cash flows are largely fee-based and thus more insulated from moves in commodity prices. While any negative performance is understandably frustrating for investors, midstream is performing as one would reasonably expect given the ~30% decline in oil prices since early October. Oil price weakness is a risk, but midstream is still the defensive place to invest in energy against the backdrop of a tough oil tape.

{kind=link}

{kind=link}

{kind=link}