Summary //

- MLPs are becoming more total-return oriented through the shift to self-funding equity, prioritizing balance sheet strength over distribution growth, and increased discussion of buybacks.

- The transition towards a total-return focus reflects lessons learned during the 2014-2016 oil downturn and the evolving investor base for the space.

- Traditional MLP investors can still enjoy attractive yields, with the potential for capital appreciation to contribute to returns as well.

Historically, investors have been attracted to MLPs for their yields, which are not only generous relative to other income-oriented sectors but also often come with the added benefit of tax deferral. Beyond attractive yields, MLPs further provide real asset exposure and diversification, though these characteristics can sometimes feel like afterthoughts. While yields remain appealing for income-seeking investors – the Alerian MLP Infrastructure Index (AMZI) was yielding 8.1% as of May 31 – the MLP space is increasingly becoming more total-return oriented through the shift to self-funding equity, prioritizing balance sheet strength over distribution growth, and increased discussion of buybacks. These factors bode well for traditional yield-focused MLP investors, while also potentially laying the ground work for capital appreciation.

What’s the difference between yield and total return?

Before getting into how MLPs have become more total-return focused, it is helpful to delineate between yield and total return. Yield simply refers to the income generated by an investment. For MLPs, this income consists of quarterly distributions. As we discussed in our white paper on MLP valuations, the historical focus on distributions resulted in the widespread adoption of yield-based valuation metrics. Often, yield plus distribution growth would be used to estimate total return. However, total return in practice should encompass both yield and capital appreciation (i.e. the price of the stock increasing). With MLPs becoming more total-return oriented, as we discuss below, yield-based valuation metrics become less suitable (see the white paper for more on this topic).

How are MLPs becoming more total-return focused?

1) MLPs are moving toward self-funding equity.

Self-funding is a term often used by MLPs, the sell-side, and Alerian but not always defined. For our purposes, self-funding refers to using retained cash flows to fund the equity portion of growth capital. To be clear, MLPs are (and will continue to be) reliant on debt financing.

Prior to the oil price downturn of 2014-16, MLPs had been somewhat notorious for issuing equity to fund growth projects or acquisitions, albeit in the pursuit of value creation. Amid the oil volatility and general energy aversion since then, equity markets largely closed on the space, and issuing equity was cost prohibitive (yields were too high). As a result, MLPs had to become more creative with their financing, making use of preferred equity and other financing tools, as well as bringing on joint venture partners or selling assets to help fund projects. In some cases, MLPs cut their distributions to redirect cash flow to growth capital or debt reduction. MLPs’ shift towards self-funding equity has largely been borne out of necessity but is positive. Self-funding instills greater capital discipline given limited financial resources, and a potential overhang is removed from units if equity is not expected to be issued. Please see the appendix to this piece for company-level detail around self-funding equity.

2) Distribution growth has taken a backseat to balance sheet strength.

Prior to the oil downturn in 2014, MLPs were largely focused on achieving distribution growth as that was what investors wanted and rewarded. Additionally, incentive distribution rights, which many MLPs have now eliminated, further encouraged distribution growth. Normalized distributions for the Alerian MLP Index (AMZ) grew by 5-7% annually for 2010 – 2013 (read more). For some, growth was pursued at the expense of the balance sheet, with these companies finding themselves overextended when oil prices plummeted. Distribution cuts and asset sales are some of the tools that have been used to repair balance sheets, with distribution cuts contributing to a decline in AMZ normalized distributions in recent years.

With lessons learned from the oil downturn, financial flexibility is likely to remain a priority for the space going forward. Take Plains All American (PAA) as an example. At the end of 2Q 2017, long-term-debt-to-last-twelve-months-adjusted-EBITDA was 5.0x, and PAA subsequently cut its distribution for a second time in 3Q 2017. Today, PAA is targeting a range of 3.0-3.5x for the same ratio and has noted that future distribution increases are contingent on achieving targeted leverage and coverage ratios, having recently raised its distribution by 20%. On the other hand, Genesis Energy (GEL), which also cut its 3Q 2017 distribution, intends to keep its distribution flat (after four quarters of growth since the cut), with management noting that they are seeking the highest and best use of capital. GEL plans to use excess cash to fund growth or reduce debt.

The emphasis on balance sheet strength over distribution growth is a function of what happened in the oil downturn as many MLPs found themselves overextended or over-reliant on raising equity, but it also reflects the evolving investor base for MLPs and what is being rewarded today. Many MLP management teams have expressed that distribution growth has not been rewarded in terms of equity price performance. Amid distribution cuts, many retail investors exited the space, and institutional ownership has directionally increased. Institutional investors are more likely to care about balance sheet strength, while retail typically cares more about distribution growth. With MLPs and energy broadly focused on attracting new investors, institutional investor preferences for improved leverage ratios are likely to continue to take precedence over distribution growth. That said, generous distributions will continue to attract retail, and the quality of the income is improving given financially healthier MLPs.

3) MLPs are talking more about buying back units than issuing them.

On recent earnings calls for MLPs and midstream companies, buybacks have become a prevalent topic (read more), particularly since Enterprise Products Partners (EPD) announced a $2-billion buyback program in late January. The discussion of buybacks marks a notable reversal from the days of prolific MLP equity issuances. In the near term, buybacks are expected to be limited given plentiful organic growth opportunities offering attractive returns. That said, if midstream capex is in the process of peaking as we suspect, that could lay the groundwork for greater free cash flow generation going forward, which could potentially be used for buybacks. With many MLP management teams frustrated by their equity performance, buybacks could be used to potentially support performance.

Implications of a more total-return focus – both retail and institutional investors can be pleased.

For MLPs, the paradigm has shifted from focusing on distribution growth to more of a total-return focus as self-funding equity, capital discipline, and balance sheet strength have become greater priorities. The shift reflects lessons learned during the 2014-2016 oil downturn and the evolving investor base for the space. For retail investors primarily interested in yield, MLPs still provide attractive distributions, even if the growth of those payments may be more subdued than in the past. The positive implication for retail investors is that the income is coming from a higher quality MLP than in the past, with leverage ratios improving, distribution coverage increasing (read more), and less risk of equity dilution as self-funding gains traction. These company-level improvements have the potential to drive improved equity performance as they are appreciated by the market and as new capital from institutional investors may be put to work in the space. In the future, buybacks may also support stronger equity performance. In short, retail investors can still enjoy attractive yields, with the potential improving for capital appreciation to contribute to returns as well.

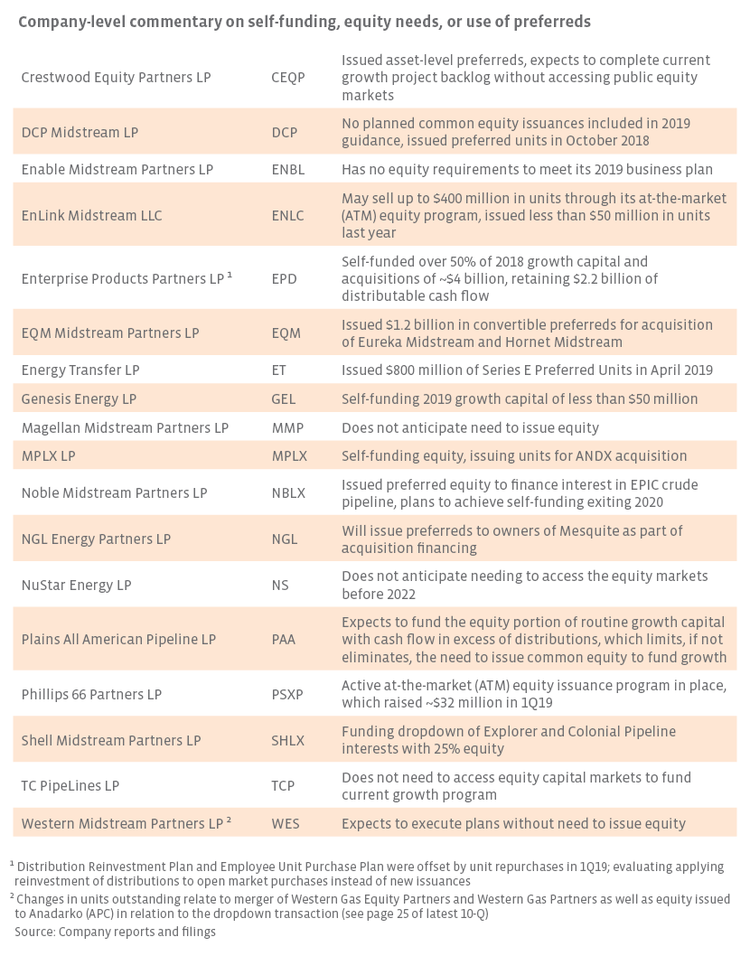

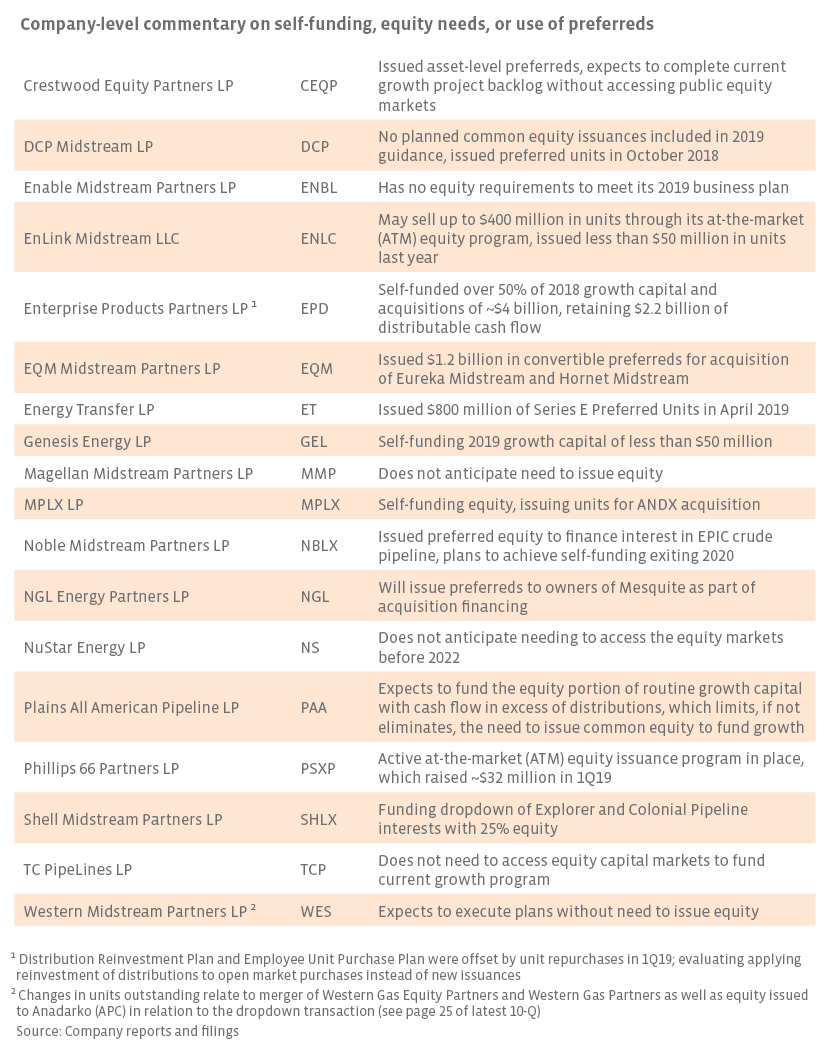

Appendix: Company-level self-funding commentary

On the surface, investors may expect self-funding to be evidenced by a stable count in units outstanding. In practice, it’s not as simple as looking at common units outstanding at points in time. MPLX (MPLX) is committed to equity self-funding as noted in its investor presentation, but its units outstanding will increase as a result of its unit-for-unit acquisition of Andeavor Logistics (ANDX), which is expected to be immediately accretive. On the other hand, MLPs with relatively static common unit counts may be using preferred equity instead of common equity. Crestwood Equity Partners (CEQP), EQM Midstream (EQM), NGL Energy Partners (NGL), and Noble Midstream (NBLX) are examples of companies that have or will use preferred equity to finance acquisitions announced this year. Even though preferred equity issued at the company or asset level is more palatable than a common unit offering, using preferred equity would not constitute self-funding in the strictest sense.

The table below provides a list of MLPs and commentary related to self-funding, equity needs, and use of preferreds.

{kind=link}