Recent guidance updates from midstream companies have mirrored this relative stability, with several names maintaining or slightly adjusting full-year estimates (read more). Aggregating 2020 EBITDA guidance updates from 23 MLPs and C-Corps, the average downward revision to 2020 EBITDA guidance was 9.0%, and the median revision was 7.8%. Cheniere Energy (LNG), Pembina Pipeline (PBA/PPL CN), and Williams (WMB) all restated prior EBITDA guidance alongside their 1Q20 earnings reports. After forecasting no change to its initial EBITDA guidance in its March 17 presentation, Energy Transfer (ET) lowered its full-year EBITDA expectations to $10.7 billion at the midpoint earlier this week. This represents a 4.5% downward revision from the midpoint of initial guidance. Management also noted that it expects 90-95% of 2020 EBITDA to be driven by fee-based contracts, further underscoring cash flow stability. The partnership continues to target positive free cash flow after its distribution in 2021 driven by project completions and a decline in growth capital spending. ETRN stands alone as the only midstream company to raise prior EBITDA projections. This morning, ETRN updated its 2020 financial expectations, which included increasing its full-year EBITDA guidance. All financial guidance is dependent on the company’s merger with EQM closing in June. Management also noted that it no longer has financial guidance past 2020, implying that the forecasts provided in February out to 2023 are now no longer applicable.

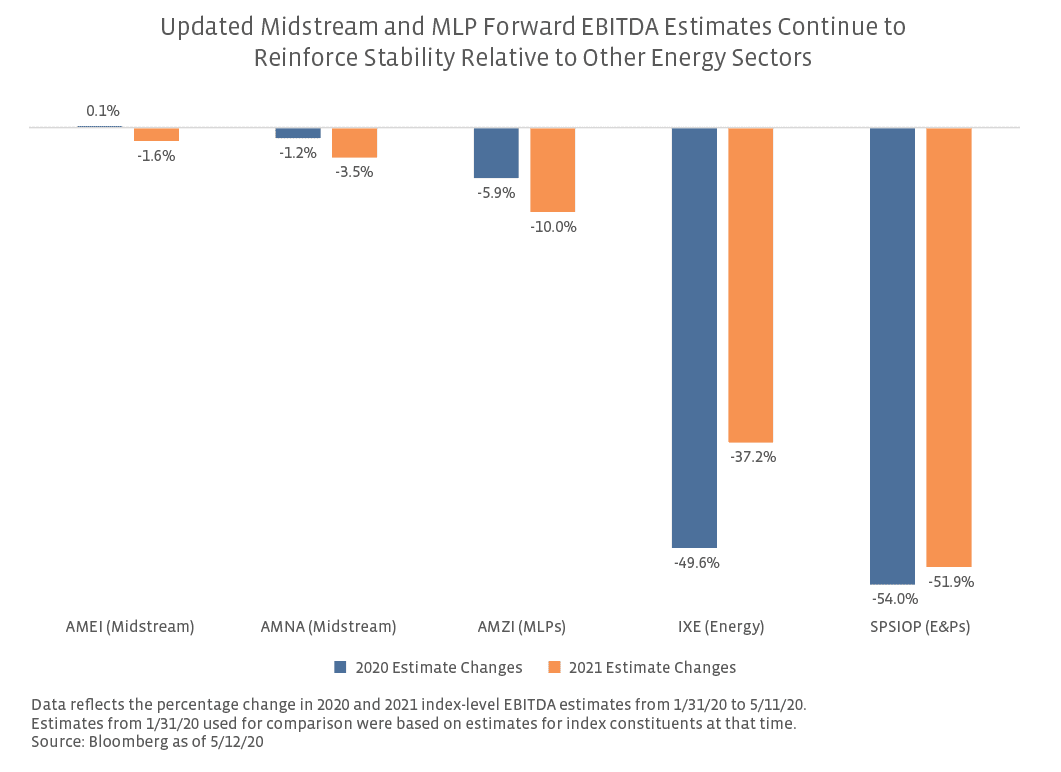

The decline in oil prices does not impact all energy companies in the same way. The relative defensiveness and stability of midstream cash flows is clearly evident in a comparison of forward EBITDA estimate revisions for midstream relative to broader energy and E&Ps. Despite the greater stability of midstream cash flows, the space has largely sold off in line with broader energy and moderately outperformed E&Ps. While the impact of negative energy sentiment and forced selling (for example, closed-end fund deleveraging for MLPs) are difficult to quantify, there seems to be a distinct disconnect in midstream equity performance relative to broader energy and E&Ps when considering the relatively mild revisions to midstream forward EBITDA expectations.

{kind=link}