Given the choice, shouldn’t I always invest in the GP over the LP?

We’ve been getting this question a lot since Tesoro Logistics (TLLP) announced last week that it would be acquiring the midstream assets of independent E&P QEP Resources (QEP). The two LPs involved – TLLP and QEP Midstream Partners (QEPM) – traded down 14% and 13% the next day, respectively, while the two GPs – QEP and Tesoro Corp (TSO) – traded up 4% and 8%, respectively.

The answer is, as you might expect from an organization that equips investors to make informed decisions about MLPs and energy infrastructure, it depends.

In favor of the GP

Like the US federal government’s take via its progressive income tax system, IDRs entitle their holder(s) to a higher percentage of incremental distributions above certain tiers, despite an economic interest of 2% or less. At the “high splits”, the GP take is 50% of incremental distributions paid. So the first argument in favor of investing in the GP is leverage, assuming you strongly believe in the fundamentals of the LP.

It’s worth reiterating that the GP take is 50% of incremental distributions paid. It is not, as sometimes believed, based on LP distributions per unit. So there’s actually two ways to grow the amount of cash paid to the GP: raising the LP distribution per unit, and increasing the number of units. While it is unlikely that a GP would issue LP units solely for this purpose, it does mean that in an acquisition, a deal may be near-term dilutive for the LP but still enable the GP to receive more cash immediately. So a second argument in favor of investing in the GP is being on the winning side of a potential conflict of interest between the GP and LP. This is also true if the company is the target as opposed to the acquirer, as the buyer typically pays a higher multiple of cash flow to the GP than its leveraged exposure would imply as compared to the LP. This is known as the control premium.

And third, some investors are firm believers in following the equity, i.e. investing alongside management whenever possible. Most executives have their bread buttered by the GP when both the GP and LP entities are publicly traded.

In favor of the LP

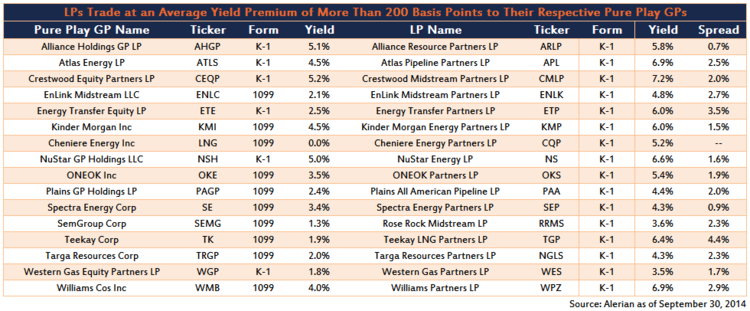

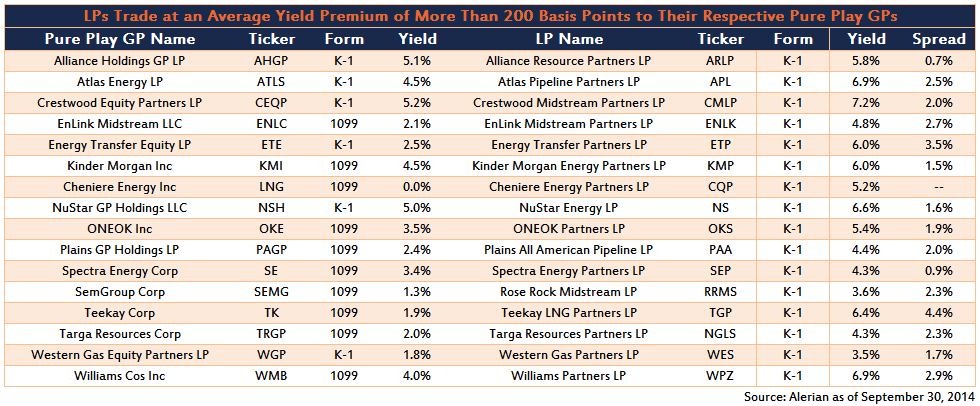

If the above paints a pretty grim picture for LPs, there are some counterpoints. First, sometimes the GP is not a pure play on the underlying LP. As we’ve recently seen more C Corporations take all or a portion of their midstream assets public to highlight the value of those assets in a sum-of-parts analysis, investing in the GP may mean exposure to different types of business risks that aren’t at the LP level, such as commodity price fluctuations in the case of E&P companies, or local regulatory dynamics in the case of utilities.

{kind=link}