Is it true that, for an entire week, you did not utilize Alerian Insights to comment on one of the highest-profile transactions in the history of the MLP structure despite your organization’s stated objective to equip investors to make informed decisions about MLPs and energy infrastructure?

Yikes. When you put it like that, we feel kind of bad. But yes, it’s true. As mentioned in a post last Thursday, we’re not trying to break news here. Think FiveThirtyEight, not CNN. We’d also just as happily point you to a great piece written by someone else that already says everything that needs to be said as write it ourselves. So to that end, seven links to understanding the Kinder Morgan transaction:

The Source

Kinder Morgan: “Kinder Morgan, Inc. to Purchase KMP, KMR and EPB; 2015 KMI Dividend to Increase to $2 per Share”

The Optimists

Simon Lack, SL Advisors: “Valuing Kinder Morgan in Its New Structure”

Jim Cramer, Real Money: “Kinder’s Triumph”

The Pessimists

Victor Fleischer, The New York Times: “Kinder Morgan Is Playing Tax Arbitrage with Itself”

The Economist: “The Reversion of a Species”

The Accountant

Laura Sanders, The Wall Street Journal: “Q&A: How the Kinder Morgan Deal Affects Investors’ Taxes”

The Historian

Hinds Howard, CBRE Clarion: “The Big Rich”

What are your thoughts on the Kinder Morgan transaction?

Prior to the restructuring announcement, KMI had been the worst performing pure play C Corporation general partner over the previous 12 months. KMP had underperformed the AMZ on a trailing one-year, three-year, and five-year basis by 14%, 33%, and 53%, respectively. EPB needed the assistance of a relatively cheap dropdown just to maintain a flat distribution over the next few years. Rich Kinder publicly acknowledged his frustration with the market’s valuation of his family of companies. Suffice it to say, it wasn’t a question of if a transaction would happen, but rather when and in what form.

It was rightly assumed that something had to be done about the IDRs in order to lower the surviving entity’s cost of capital, eliminating the option of taking KMI private again to address Kinder’s irritation with his stock price. It was also rightly assumed that KMI could not permanently give up any portion of its IDRs without compensation, as Enterprise did in 2002, given its public ownership base. Finally, it was assumed that the second largest tenant in the MLP building would never consider ending its tenancy, especially given its CEO’s role in the evolution of MLPs from pure yield investments to total return vehicles. Most of the rumors among the stakeholder community consequently focused on KMP acquiring KMI or resetting its IDRs in exchange for units.

It turns out that the last assumption was wrong, and the announced restructuring creates the best pre-tax outcome across the four entities, which is why all four securities traded up meaningfully last Monday. The words “pre-tax”, of course, are necessary because the structure of this transaction creates a taxable event for KMP and EPB unit holders. We feel particularly sympathetic toward retail owners with a low cost basis in either of these two securities, many of who have taken to the comments section of national media articles concerning the deal to air their grievances. Certainly, one can make the argument that these unit holders have a low cost basis because they’ve been long-time owners and have made plenty in price appreciation along the way. But an unexpected tax bill is still just that.

So what are the implications of this restructuring? One, the rest of the MLP universe trades up. Almost everything traded higher after the announcement because Kinder referred to the 120 energy MLPs and their $875 billion in enterprise value as “a fertile field to do a little grazing in.” On a related note, some portion of after-tax proceeds to KMP and EPB unit holders will find their way into other MLPs. Two, the cost of capital can has been kicked far enough down the road to be out of sight to most stakeholders, which should help KMI’s valuation for the next 3-4 years. What happens when the can reappears in the future remains unknown. Three, we will not see a flock of MLPs rush to restructure in the same manner. Kinder Morgan’s size requires bigger projects and acquisitions to move the needle. Its high splits create a long-term, relative (and absolute) cost of capital problem. Its CEO is acquisitive. It has four publicly traded securities outstanding. Take away any of these four factors, and this particular way of restructuring becomes at least somewhat less likely. That said, this transaction does give management teams and their financial advisors another option to consider should they find themselves in a similar situation in the future.

We certainly can’t speak to Kinder Morgan’s wish list as far as acquisitions are concerned. The possibilities most frequently mentioned by stakeholders are US LNG liquefaction projects, domestic energy value chain businesses in which Kinder Morgan is not currently involved (in order to avoid antitrust issues), Canadian energy infrastructure companies, and other foreign assets.

We leave this mailbag question with two points of speculation to consider. One, if KMI acquired the general partner of a publicly traded MLP, what would Kinder do with the vehicle? And two, if KMI remains undervalued, will activists point the finger at the CO2 business and agitate for a spin-off?

What are the transaction’s implications for the Alerian Index Series?

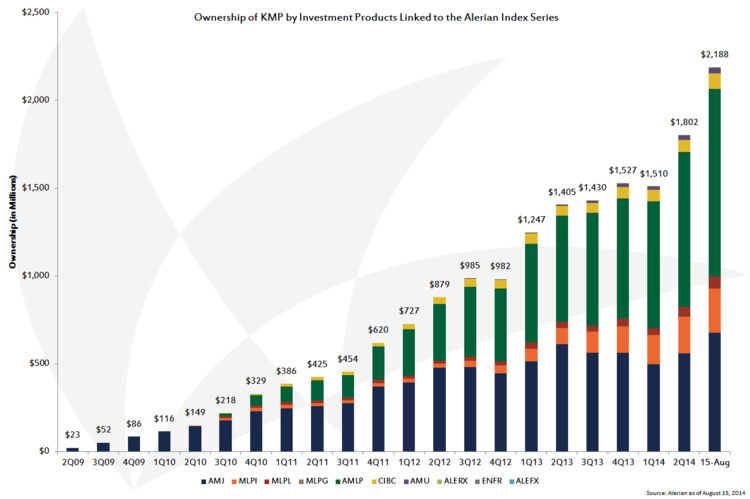

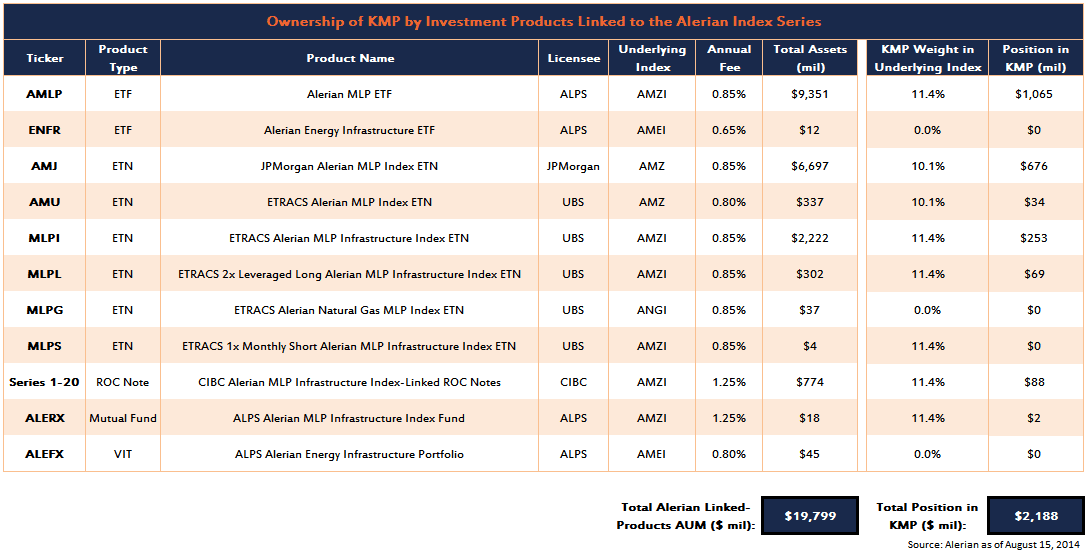

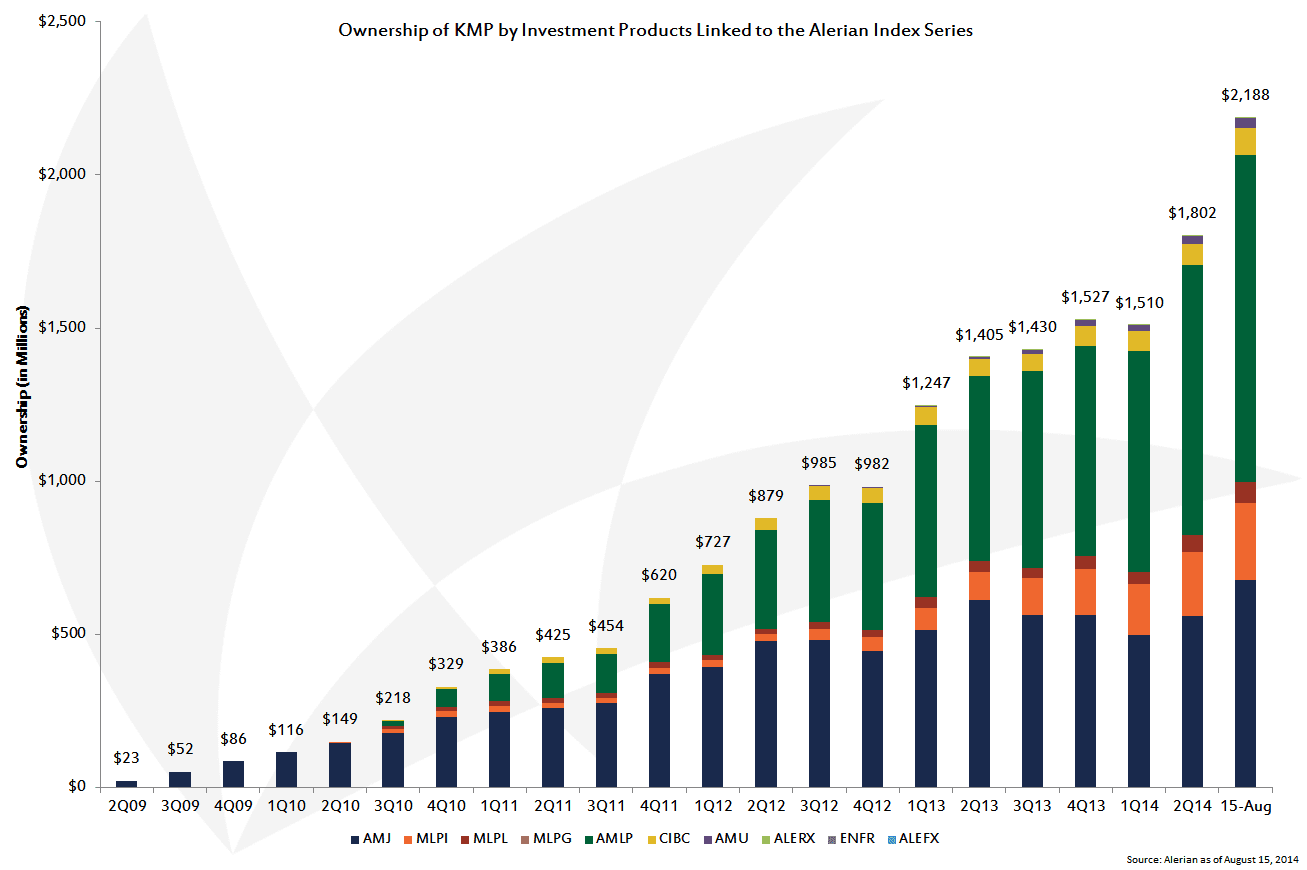

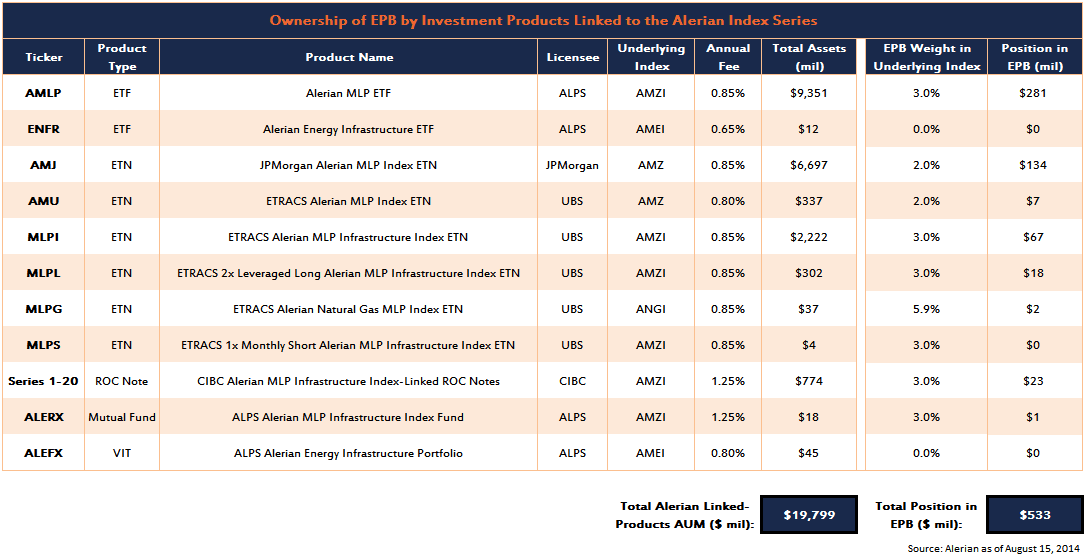

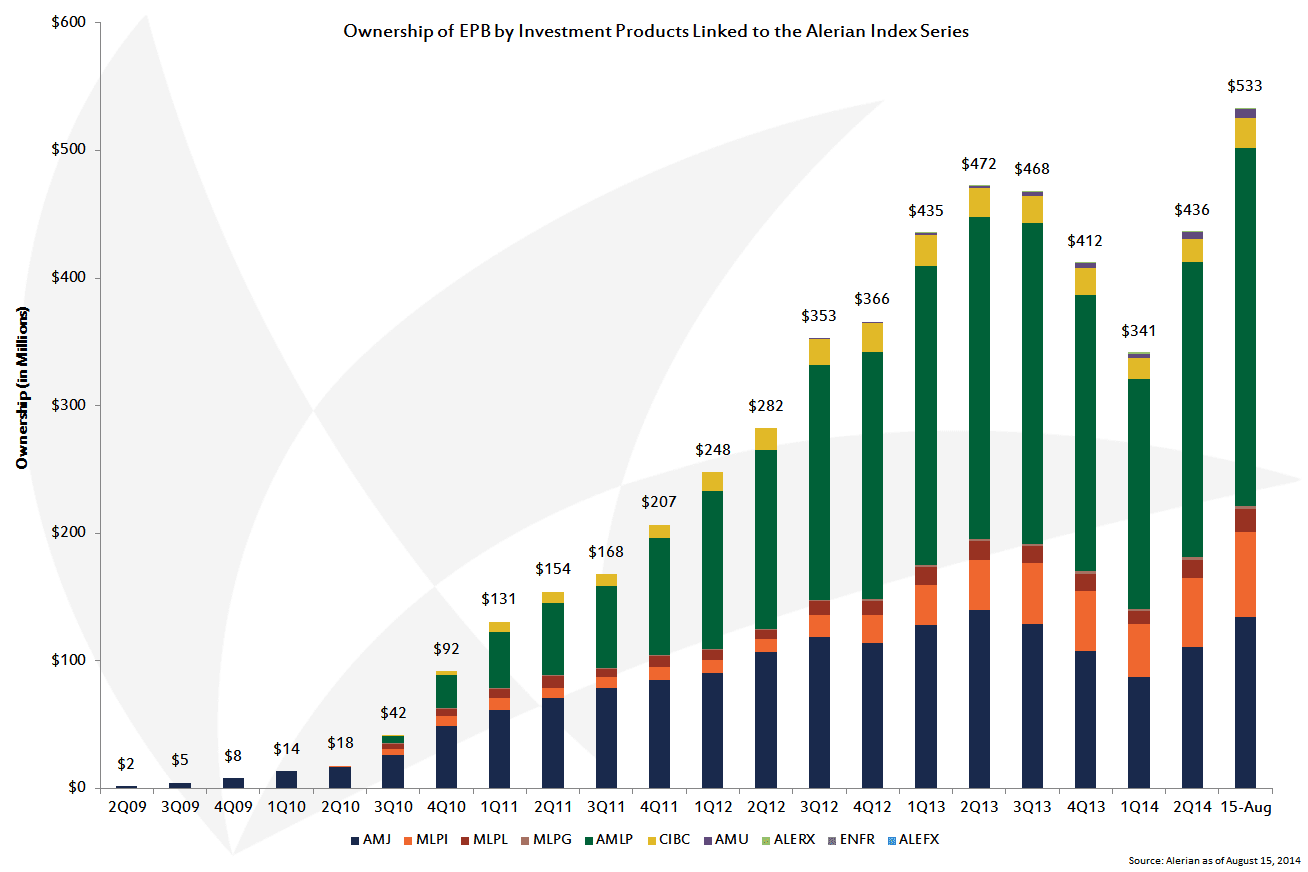

The tone with which most stakeholders have asked this question over the past week suggests that the real prompt is, “Are you aware that your licensees own more than $2 billion in the Kinder Morgan family of securities, and that your index methodology, as it currently stands, will wreak a mild form of volatility havoc on KMI?”

Yes, we are aware of the possibility of which you speak. Our four largest licensees own almost $2.2 billion of KMP as of August 15:

Since we launched the first real-time MLP index on June 1, 2006, the methodology guides for the Alerian Index Series have gone through various revisions in order to clarify confusing statements, but just as importantly, to evolve with the industry. Again, our vision is to equip investors to make informed decisions about MLPs and energy infrastructure. Future revisions, if any, will be motivated by this vision. As such, all we can say at the moment as it relates to this transaction is that, as always, we will rebalance each of our indices in accordance with the publicly available index methodology guides at that time. We welcome your questions, comments, and suggestions (and complaints too, I suppose) at [email protected].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}