Thanksgiving is a dramatic family holiday. In Rockwell’s America, we sit down with our loving families and the family patriarch carves a turkey. There is as much pie as we can eat, conversations are pleasant, and no one gets fat. But the stories we actually tell come Monday morning generally involve culinary disasters and awkward (if not explosive) conversations. Here’s one thing I’ve learned: people will always live up or down to expectations. When I preface my news with, “I have something really exciting to tell you!” and not “Please don’t be upset,” I’m much more likely to hear “Congratulations!” than “Are you sure that’s the best idea?” And then next year, they’ll ask how it’s going, instead of how I’m coping. At least, that’s always the hope and the plan.

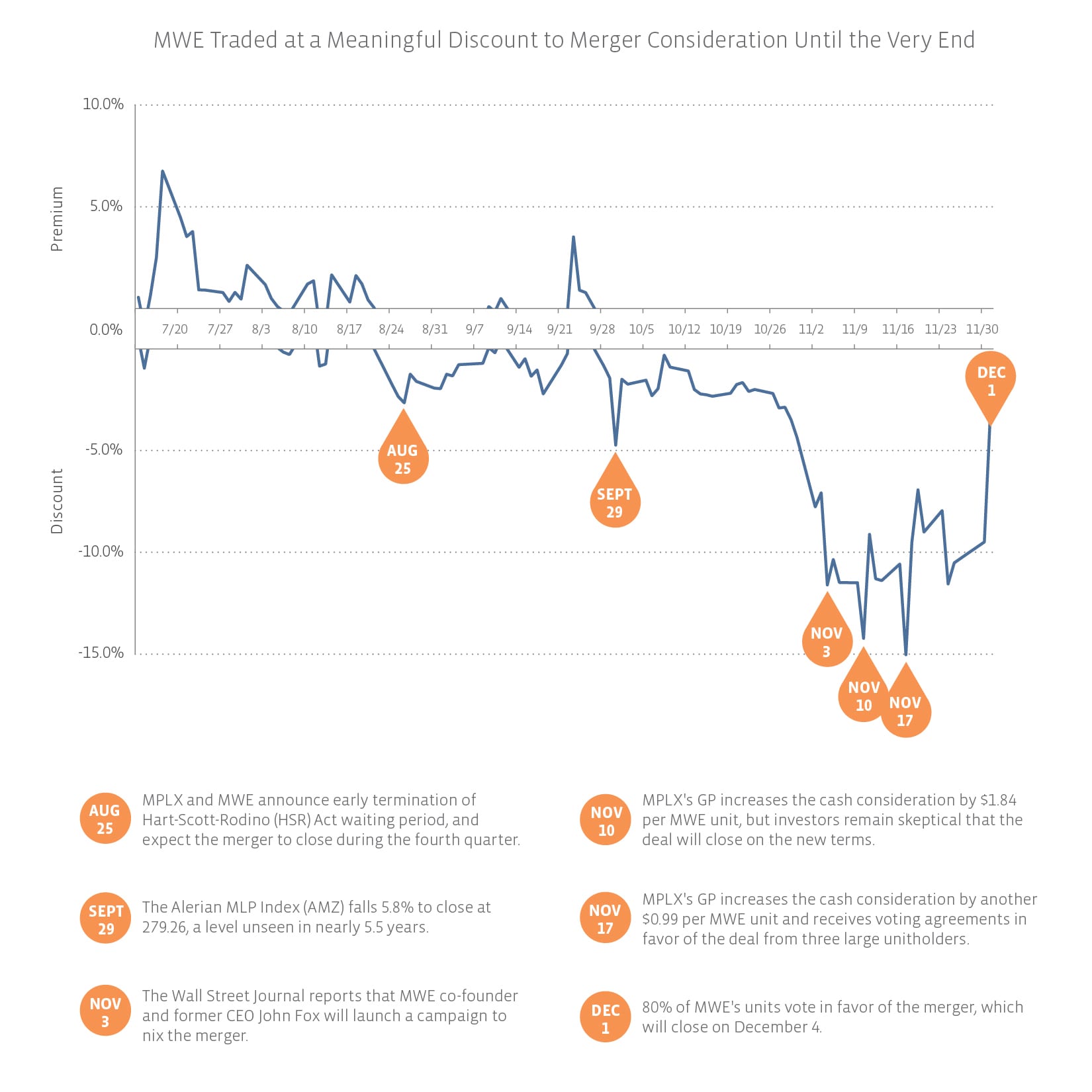

MLP merger announcements usually work in much the same way: once a deal is announced, the to-be-acquired-company’s units trade to approximately the consideration that unitholders will get once the transaction closes. The merger between MarkWest Energy Partners (MWE) and MPLX (MPLX) followed that script in the beginning, but took a decidedly different turn during the month of November.

The original agreement announced on July 13th offered MWE unitholders 1.09 MPLX units and $3.37 in cash for every MWE unit owned. Using the prior day’s closing prices, this represented a 31.6% premium over the then-current MWE price. But MPLX unitholders thought that the deal ruined their dropdown story and consequently sent the acquiring company’s stock tumbling 14.5% on the day of announcement, resulting in MWE trading up only 15.6% that same day.

MWE largely traded within a band of plus-or-minus 2% against the consideration over the next few months until the Wall Street Journal reported on November 3rd that co-founder and former CEO John Fox would be mounting a campaign to nix the deal. Fox would go on to write four open letters to management (here, here, here, and here) over 2.5 weeks and take letter writing into the 21st century with a website, the self-explanatory iamvotingno.com. His main criticisms are that (1) unitholder distributions will drop significantly, (2) the IDRs owed to MPLX GP Marathon Petroleum (MPC) will create a drag on growth, and (3) MWE is better as a standalone company.

By market close on November 10th, MWE traded to a 14.2% discount against the consideration offered by MPLX, reflecting a high degree of investor skepticism that the deal would close. MPC responded that evening by increasing the cash portion of the consideration to $5.21. But the spread remained wide. Despite increasing the cash consideration a second time to $6.20, noting the support of three of MWE’s largest unitholders, and receiving the recommendations of not one, not two, but three proxy advisory firms, MWE stubbornly remained at a 9.4% discount to merger consideration on November 30th, the eve of the vote.

As it turned out, the vote was anticlimactic, with the special meeting lasting less than 10 minutes and 80% of units voting in favor of the merger. The discount subsequently shrunk to 3% as of yesterday’s close.

{kind=link}