Adding to market oversupply was aggressive growth in US oil production, which was up 1.9 million barrels per day (MMBpd) or 19.4% year over year in 2H18 vs. 2H17. Coinciding with a shift to market oversupply were rising concerns for the demand outlook as the global economy seemed to be losing its footing with US-China trade relations continuing to languish at the time. A strengthening US dollar also contributed to weakening oil prices (a strong dollar makes oil, which is priced in USD, more expensive).

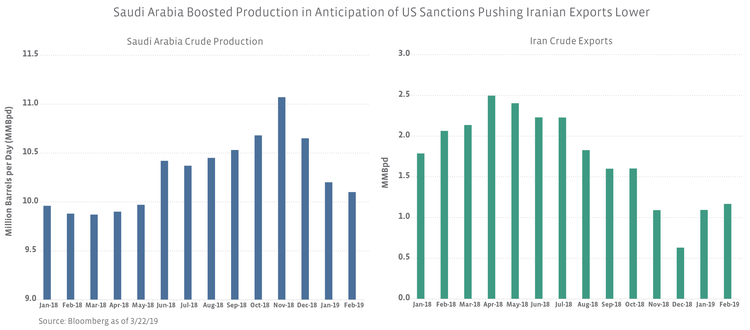

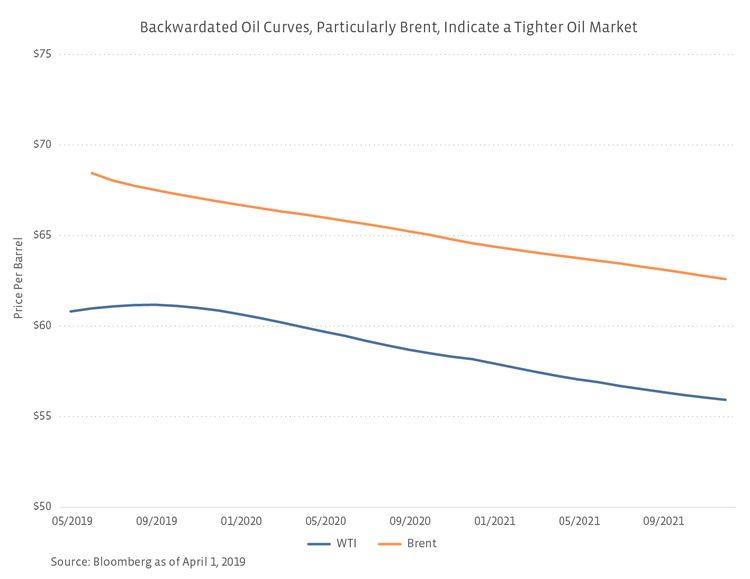

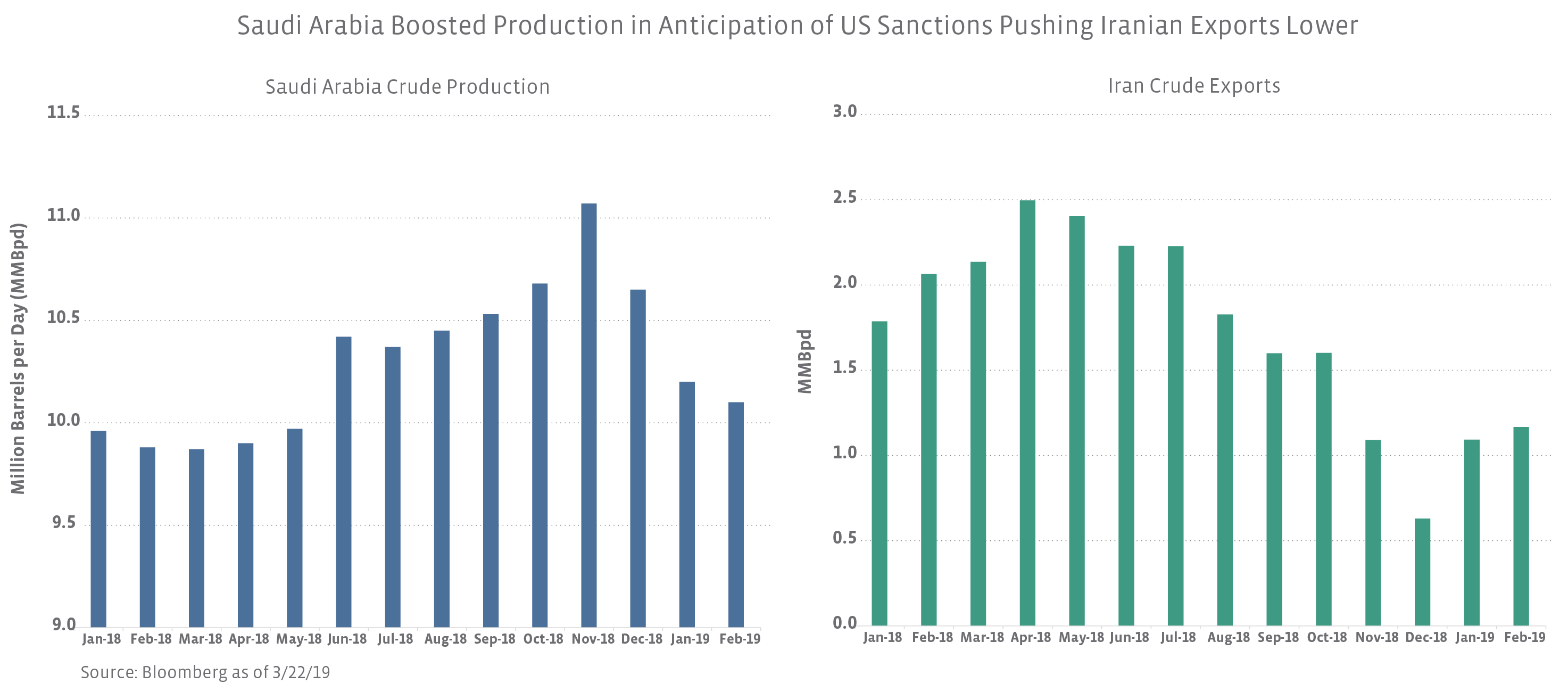

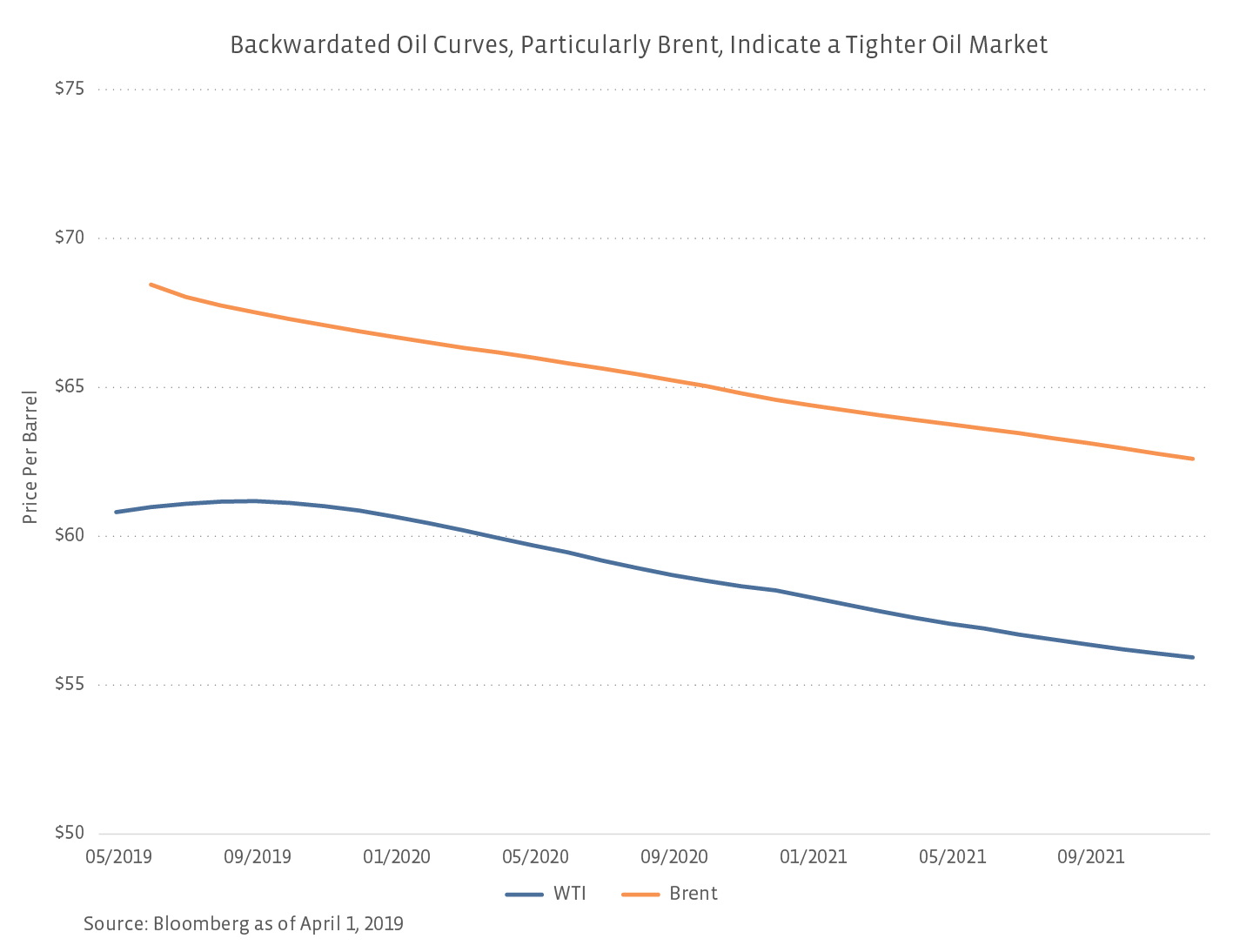

Amidst tumbling prices (and a worsening oversupply), OPEC and its non-OPEC counterparts, namely Russia, agreed in early December to cut production by a combined 1.2 MMBpd for six months beginning January 1, 2019. Saudi Arabia went above and beyond its agreed upon cuts by further slashing exports and production. For example, though it agreed to produce 10.3 MMBpd, Saudi Arabia expects April production to come in below 10 MMBpd. Saudi Arabia doing more than its fair share in terms of OPEC and allies’ production cuts combined with continued declines from Venezuela, anticipation of a US-China trade deal, and an improved outlook for the overall economy have underwritten the improvement in oil prices year to date. As shown below, backwardation in the Brent and WTI futures curves, particularly the steeper backwardation for Brent, are indicative of a tighter (undersupplied) oil market. Where could oil prices go from here? We lay out bull and bear scenarios below, as well as potential wildcards.

The bull case: Supply interruptions worsen in the near term, potential supply gap long term.

Today, the most compelling bull case for oil lies on the supply side in our view, though the fate of production cuts remains a wildcard. In the near-to-medium term, the potential for supply impacts would be largely around geopolitical issues – a la declining Venezuela production or Iran sanctions having more teeth as a result of fewer waivers. In the long term (i.e. over the next few years), the bull case from a supply perspective is that an underinvestment in oil projects globally in recent years will lead to a supply gap. Specifically, from 2014 to 2016, global upstream capital spending fell 44%, and annual spending since 2016 has remained more than $300 billion below the 2014 level according to the International Energy Agency (IEA). The IEA estimates that production needs to grow by an amount equivalent to total North Sea production (~2.6 MMBpd in 2018 per Bloomberg) to offset declines in producing fields and keep global production flat. If underinvestment leads to a supply gap and US shale cannot fill that gap, an undersupplied market could result, driving prices higher.

The bear case: Demand a greater concern than supply for now.

The bear argument for oil prices is largely wrapped up in demand concerns stemming from the potential for a global recession. In the wake of the financial crisis, global oil demand fell by 1.1 MMBpd (-1.3%) in 2009, as growing demand from non-OECD countries could not offset a 2.2 MMBpd decrease from OECD countries. Keep in mind that OPEC and its partners are already restraining production by a similar amount (~1.2 MMBpd) with the IEA forecasting demand growth of 1.4 MMBpd for 2019. An important difference to note between today and 2009 is that non-OECD demand has eclipsed OECD demand, which could lead to different demand sensitivities in a recession and less of an impact to demand than seen in 2009.

On the supply side, assuming existing production cuts are maintained until no longer needed (and phased out in a measured way), the threat to oil prices stems from US oil production growth leading to an oversupply. We believe this is less likely in 2019 given US E&Ps’ focus on capital discipline and the fact that annual budgets were established during or shortly after the oil price pullback in 4Q18. We expect more measured US oil production growth in 2019 relative to 2018 (read more). Over the next few years, US oversupply could be a potential threat if prices were to rise more meaningfully from today’s levels, thus incentivizing greater growth.

Wildcards and known unknowns

There are more moving parts to oil prices than we have real estate to discuss, but we briefly touch on some of the potential drivers for prices in the coming months.

- Cut continuation or not — OPEC and its partners will discuss the future of production cuts at the OPEC meeting scheduled for late June.

- Iran sanctions — As six-month sanction waivers begin to expire in May, markets will be watching to see whether renewals are granted or other actions are taken. Media reports indicate that the near-term goal is to reduce exports to less than 1 MMBpd, but the ultimate objective is to bring exports to zero, while also trying to avoid causing an oil price spike.

- US-China trade deal — If a deal is not reached, the implications for demand would be negative due to less physical trade but also in terms of the potential impact to the global economy.

- Currency moves — Because crude is priced in dollars, a stronger dollar puts negative pressure on prices, while a weaker dollar is supportive. Stronger emerging market currencies make USD-priced oil more affordable, supporting demand.

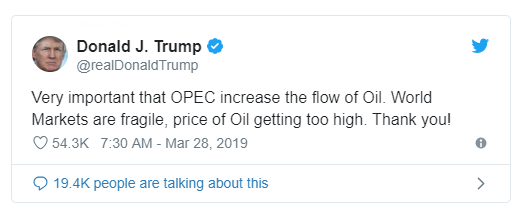

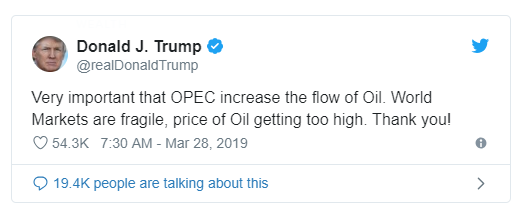

- Politics — The impact to oil prices this fall from the US issuing Iran sanctions waivers serves as a reminder that political actions can meaningfully move markets. Commentary from President Trump further exemplifies the impact that politics can have on oil. For example, Brent oil prices fell 3.5% on February 25 when the below tweet was posted. Brent rebounded by 0.7% the next day and gained a further 1.8% on February 27 as OPEC members reiterated their commitment to cuts.

Last Thursday, President Trump again tweeted about oil prices and the need for OPEC to increase production. While Brent prices dipped after the tweet, the impact on the day was negligible as losses were erased.

- NOPEC – Congress is currently considering legislation that would ban foreign nations from collaborating to manage fossil fuel markets. If implemented, the US Department of Justice could potentially sue countries for actions violating antitrust laws. Arguably, the primary beneficiaries of OPEC and non-OPEC cuts have been US oil producers, and they may be the most negatively impacted in a world without OPEC (and its partners) taking action to support prices.

Where are prices going? That’s the $50, $60, $70, or maybe $80 or $100 (per barrel) question.

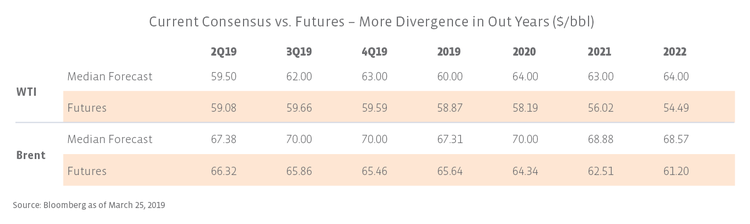

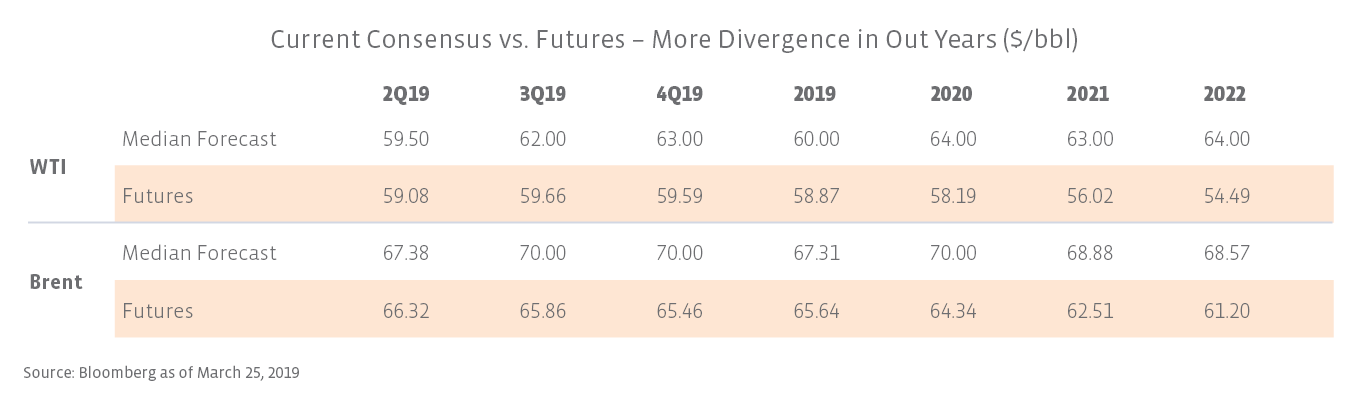

In this piece, we do not provide an oil forecast. Often, forecasts tend to be reactionary and more akin to a mark to market. Other times, forecasts reflect such a wide range that they become less useful – a $20 or $30 per barrel range for an oil forecast is a bit like a golfer putting into a hole with a 2-foot diameter. As is often said in the industry, if someone could accurately predict oil prices and do so repeatedly, they would probably be on a beach somewhere instead of writing research. We include current consensus below and futures for those interested in the market view on oil. Forecasts for 2019 are relatively close to futures prices, but the difference between consensus and futures widens the further out the projection. Consensus is more bullish than the backwardated futures curves but is generally in line with today’s current pricing environment.

Bottom line

While supply and demand should fundamentally drive oil prices, a myriad of factors can influence the balance between the two over time, and headlines impact prices on a day-to-day basis. Assuming OPEC and its allies stay the course on production cuts until they are deemed to no longer be needed, the primary downside risk in oil comes from the potential for a global recession and the negative impact that could have on demand. Longer term, the potential for a US-driven oversupply is also a risk. On the other hand, the upside to prices would likely be unexpected or worsening supply interruptions and a potential supply gap in the long term. Of course, any of the wildcards discussed in this piece has the potential to contribute upside or downside pressure on prices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}