Source: Plains All American Investor Day Presentation

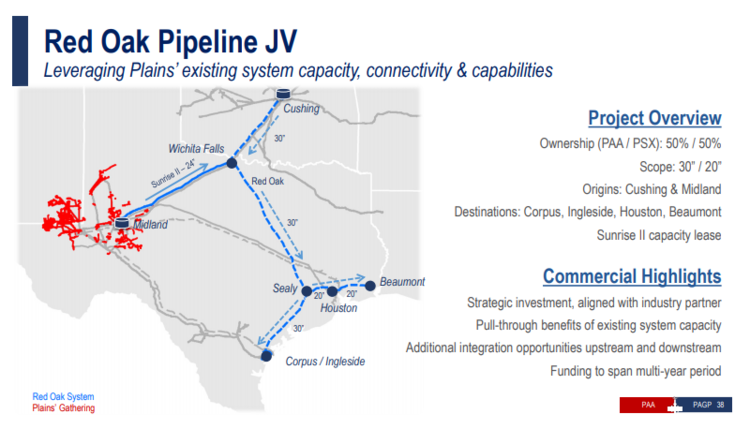

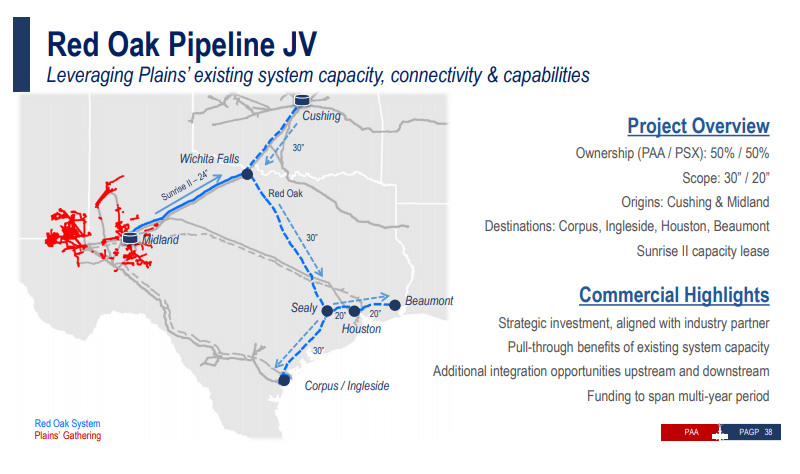

As a result of the new JV, capital expenditures will not decline as quickly as some investors may have anticipated. Management restated its 2019 growth capex guidance of $1.35 billion (~80% of which is Permian-related) but is now no longer expecting a material decrease in spending in 2020, as most of Red Oak’s $1.25 billion cost to PAA will hit next year’s budget. Management still expects capex to decline after 2020, citing a future annual run rate of $750 million to $1 billion.

While Red Oak garnered most of the attention, PAA provided updates on other key projects in its backlog. On May 28, PAA announced an expansion and new JV on its Red River Pipeline, which runs from Cushing to Longview, TX. The 150 thousand barrels per day (MBpd) pipeline system will be expanded to 235 MBpd. Delek Logistics Partners (DKL) purchased a 33% ownership interest in the system for $128 million and increased its throughput and deficiency agreement to 100 MBpd from 35 MBpd, supporting the expansion. PAA also gave an update on its Permian crude and condensate pipeline Cactus II, which is on schedule to begin initial service by the end of the third quarter of 2019. Additionally, both a potential Capline Pipeline reversal and an expansion to the Diamond Pipeline are still being considered. PAA is targeting light crude service on the Capline reversal as early as the second half of 2020 and heavy crude service in 2022.

PAA embracing “Midstream 2.0.”

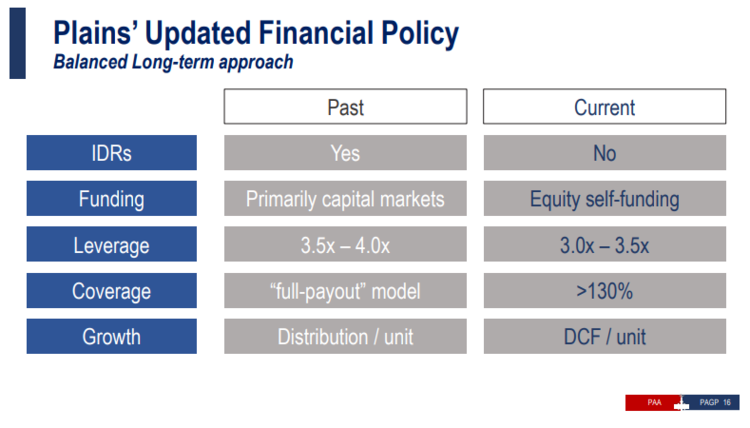

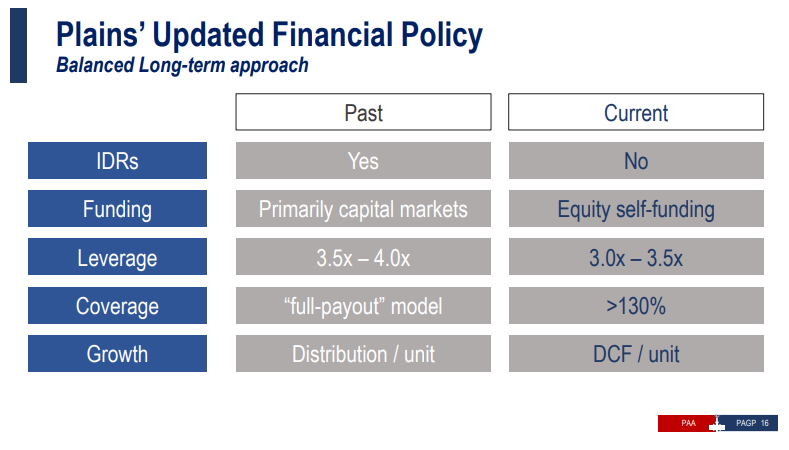

As is the case with other large MLPs, PAA continues to highlight its shift to a more balanced, long-term approach to the business founded on a stronger balance sheet, ample liquidity, self-funding equity capital expenditures, and sustainable distribution coverage in order to appeal to a broader investor base. In the table below, PAA has highlighted its progress towards these “Midstream 2.0” initiatives. This discussion was similar to the traditional financial model discussed by Enterprise Products Partners (EPD) at its analyst day (read more).

Source: Plains All American Investor Day Presentation

Maintaining a strong balance sheet and financial flexibility remains a priority for PAA. Going forward, the partnership is targeting a mid-BBB/Baa credit rating (currently BBB-/Ba1) and a long-term debt/adjusted EBITDA ratio of 3.25x at the midpoint. Management is also targeting an annual distribution growth rate of 5% over the next few years, contingent on meeting leverage goals. Since the third quarter of 2017, PAA has reduced its leverage ratio by roughly two turns, primarily due to the execution of its 2017 deleveraging plan and growth of its fee-based businesses. Strength in the supply and logistics (S&L) segment since 2018, stemming from favorable basin differentials, has pushed PAA’s current leverage ratio to the lower end of its target guidance; however, management expects 2020 S&L earnings to be meaningfully lower than they are this year, resulting in lower EBITDA and a higher leverage ratio. Regardless, PAA is well-positioned to continue executing on its deleveraging plan, with management noting the possibility of achieving a credit rating upgrade.

In terms of capital allocation, PAA will continue to prioritize the use of excess cash flows to reduce leverage or fund capital expenditures for now. However, management also discussed the possibility of eventual opportunistic share buybacks. Commentary on the potential for buybacks is welcome given the significant shift unit repurchase programs represent from the historical MLP model of regular equity issuances (read more).

Environmental, social, and governance (ESG) topics were also discussed at length. Roy Lamoreaux, Vice President of Investor Relations, Communications, and Government Relations, noted that historically PAA has focused on “doing good and being good, but not necessarily looking good” from an ESG perspective. To remedy this, the partnership will be increasing the number of ESG metrics disclosed this year. These disclosures have become increasingly important to energy and generalist investors alike and may help to broaden PAA’s investor base along with the partnership’s other “Midstream 2.0” initiatives.

Plains is well-positioned to benefit from Permian macro trends.

The Permian basin is currently the fifth largest global producer of crude oil in the world and is expected to overtake Iraq to become the fourth largest by the end of the year. At the same time, an increasing portion of global demand is expected to come from Asia, requiring more exports of Permian crude from the Gulf Coast. Management noted that even though the combined population of China and India is nearly ten times greater than that of the US, India and China consume approximately the same amount of oil as the US. PAA’s existing assets and planned projects position the company to take advantage of Asian growth, especially given the partnership’s crude quality segregation capabilities. Most of PAA’s systems are capable of segregating different grades of crude at the lease which, when combined with dedicated terminalling, allows for segregated shipping to the market. Quality segregation has become increasingly important recently as API gravity in the Permian migrates higher, meaning that crude is becoming lighter. Since complex Gulf Coast refineries prefer heavier grades of crude, PAA expects that incremental light crude production will need to be exported, primarily to Asian markets. Management views the segregation capabilities of PAA’s systems as a competitive advantage that will become increasingly important going forward.

Bottom Line

As one of the largest MLPs, PAA provides yet another example of midstream shifting toward a more balanced business model, emphasizing self-funding equity, lower leverage, financial flexibility, and healthy distribution coverage. Investors should welcome the transformation across midstream to a greater focus on capital discipline, financial strength, and ensuring the long-term sustainability of the business.

{kind=link}

{kind=link}