Narrowing crude spreads reduce spot shipment upside.

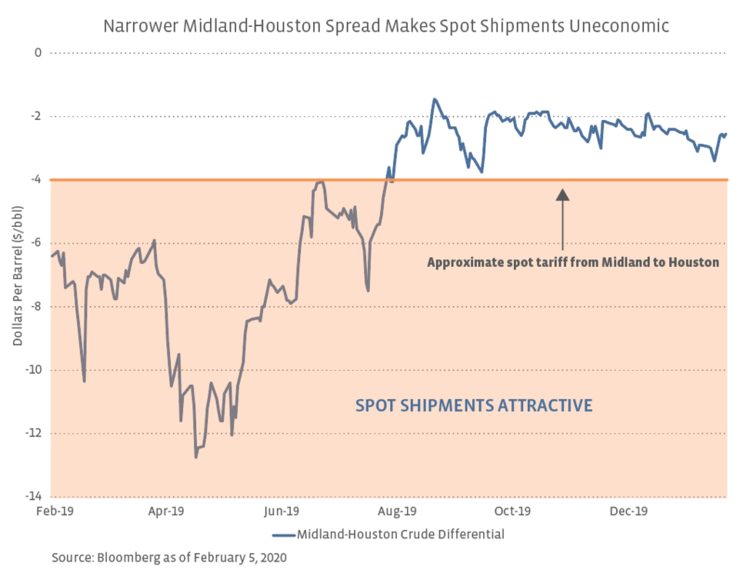

The large spread between Permian and Houston crude prices seen during most of 2019 allowed midstream companies to take advantage through uncommitted shipments at advantageous rates. Midland crude traded at an average discount of nearly $9 per barrel relative to crude in Houston in 2Q19, reflecting pipeline capacity constraints out of the Permian and stranded barrels. However, by 4Q19, the discount had narrowed to ~$2 per barrel as PAA’s Cactus II Pipeline came online and EPIC’s NGL pipeline began interim crude service, and it remains near that level now. With new pipelines in operation, narrowed differentials seem here to stay, which is impactful for spot shipments and rates. While most pipeline capacity is committed under long-term contracts, a small percentage of capacity is left available for ad hoc shipments at generally higher rates.

How much higher are spot rates? To use an example, Magellan Midstream Partners (MMP) charges over $4 per barrel for spot capacity on its Permian pipelines. For comparison, the average committed rate for capacity on MMP’s Longhorn Pipeline is expected to be $1.95 per barrel in 2020. The difference in the two rates demonstrates the supplemental revenues generated by spot nominations; spot volumes are proportionally smaller given that most capacity – as much as 90% or more – is committed. Cactus II, for example, had 90% of its original capacity of 585 MBpd contracted prior to beginning service. As shown in the chart below, the wide WTI Midland-Houston price spread made spot shipments economic until August 2019 when new pipeline capacity began to come online. Note that a $4 spot tariff, while useful for the purposes of this example, could change over time given narrower differentials.

Companies guiding to lower marketing revenue in 2020.

Pipeline operators were able to temporarily benefit both in 2019 and over the last few years from wide crude price differentials by exploiting arbitrage opportunities on spot shipments or through marketing businesses (termed Supply and Logistics or S&L by some companies). Marketing in this case involves purchasing crude at the origin of a pipeline and reselling the crude at the destination, making a margin on the price difference that is offset by transportation and logistics costs. In addition to providing flexibility for customers, these businesses can capture market opportunities resulting from price volatility or large price spreads between two different areas, generating incremental revenue. PAA and EPD were among the companies that outpaced their initial 2019 EBITDA guidance at least partially as a result of favorable contributions from marketing, with PAA nearly doubling its expected segment EBITDA for Supply and Logistics in 2019. However, given narrower Permian differentials, Plains is guiding to S&L segment earnings of $75 million in 2020, a decline of more than 90%. Similar commentary has been provided by other MLPs with pipelines out of the Permian. On its 4Q19 earnings call, MMP management noted that the Permian-Houston spread is not expected to be sufficient for spot shipments on the BridgeTex and Longhorn pipelines, assuming a spot tariff of $4 per barrel. Similarly, EPD suggested less favorable spreads across their assets – among them Permian crude pipelines – could reduce marketing earnings by $500 million in 2020.

While increased S&L earnings were a nice boost for companies that were able to take advantage, they were not expected to last and are not the basis for building budgets. Each of the companies discussed above had warned previously that the narrowing Midland-Houston spread could make spot shipments uneconomic as soon as 3Q19, which aligns with when differentials shrunk as pipelines came online. The benefit for companies with interests in the newbuild pipelines is fee-based cash flows. As volumes ramp on new pipelines, companies involved will realize a corresponding increase in steady cash flows that could offset a decrease in variable S&L or marketing revenue.

What do additional pipelines mean for tariff rates?

Over time, tariff rates out of the Permian have moved directionally lower as a result of increased competition for takeaway capacity and the anticipation of new pipelines coming online. Spot tariffs were cut by about half on Energy Transfer’s (ET) Permian Express 2 and 3 crude pipelines and the EPIC Crude Oil Pipeline in 3Q19, while PSXP proposed lower tariffs on both spot and committed rates on its Gray Oak Pipeline in November. On its 4Q19 earnings call, Magellan recently noted they were seeing lower contracted rates in the range of $1.10 to $1.50 per barrel available in the market as they worked to recontract the 275-MBpd Longhorn Pipeline. Despite the competitive environment for crude pipelines, MMP CEO Mike Mears highlighted the MLP’s new 10-year take-or-pay agreement with a quality counterparty, with more than 80% of Longhorn’s capacity contracted for 2020. The pipeline’s new average committed rate of $1.95 per barrel for 2020, while lower than in the past, provides increased visibility to investors on future cash flows from the asset.

Bottom Line

New pipelines continue to transport increasing amounts of crude from the Permian to the Gulf Coast, and more takeaway capacity is on the way. Narrowing spreads have largely eliminated the temporary earnings boost provided by S&L arbitrage, so now the focus shifts back to the bread and butter of the midstream space – fee-based cash flows from pipelines. Permian takeaway capacity is likely sufficient for the next few years, which has led to increased competition and downward pressure on tariffs. That said, new pipelines will produce steady cash flows for companies involved and facilitate the growth of Permian crude production to come.

{kind=link}

{kind=link}