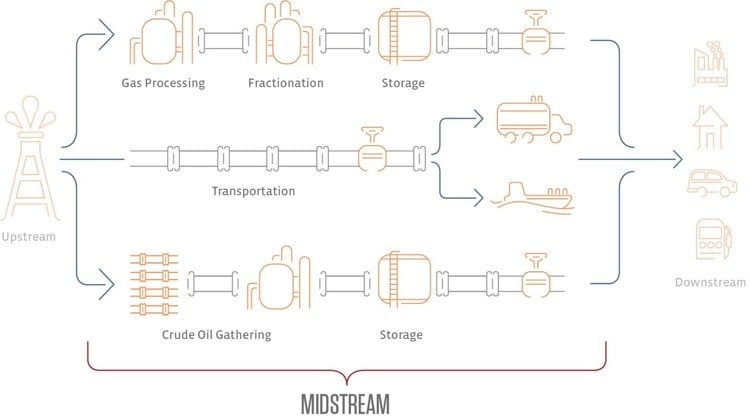

Petrochemical processing plants take a hydrocarbon input, such as oil, natural gas, or natural gas liquids (NGLs), and convert them into a usable product through complex chemical and engineering processes. Typically, petrochemical plants apply a high level of heat and pressure to break a long chain of hydrocarbons into a smaller chain in a process called cracking. The products of petrochemical processing include the key components of consumer goods like plastics, rubber, and textiles, as well as the feedstocks for major industrial processes that create basic chemicals in items such as fertilizers, detergents, and dyes.

Petrochemicals: In the driver’s seat for oil demand growth?

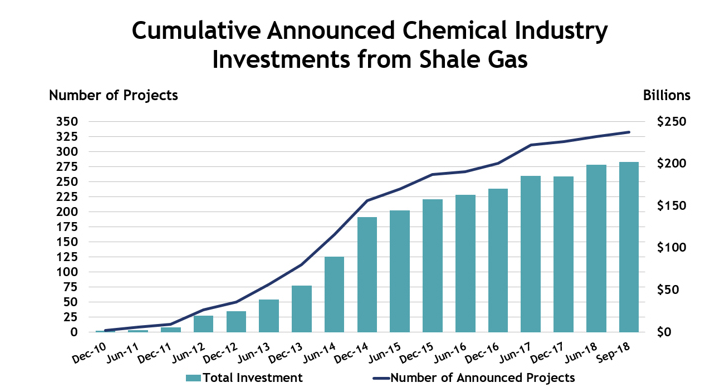

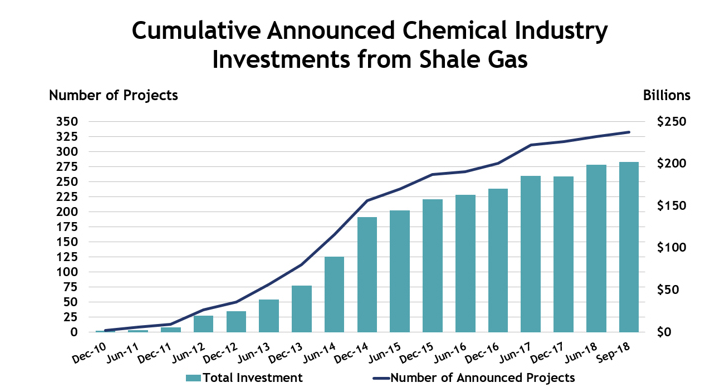

When you think about oil demand growth, you probably picture the burgeoning use of cars and motorcycles in developing countries. However, according to an analysis by the International Energy Agency, petrochemical products are expected to account for more than one-third of global oil demand growth by 2030 and almost half of demand growth by 2050. One reason for this is the mushrooming demand for plastics and other industrial end products in developing economies. In terms of supply, the rapid growth in crude, natural gas, and NGL production related to the shale revolution has boosted opportunities in the North American petrochemicals market. An analysis from the American Chemistry Council shows that US chemical industry investment related to the shale boom has surpassed $200 billion across 333 projects (see chart below). Cheap and abundant natural gas and NGLs represent cost-advantaged feedstock for North American petchem projects. As we will discuss more below, companies have capitalized on this opportunity by building out propane dehydrogenation (PDH) and ethylene plants (read more) to meet worldwide demand for chemicals. Ethylene is used to create polyester in clothes, rubber in tires, and plastics in milk jugs and other packaging.

Source: American Chemistry Council

Midstream taking advantage of positive trends in petchem.

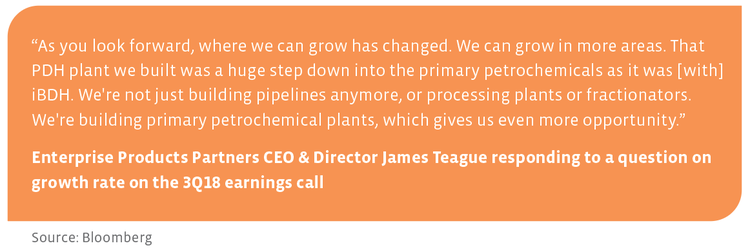

Expectations for robust demand growth have sparked interest in petrochemicals among select midstream companies, but petchem projects are not new in midstream. In August 1999, Enterprise Products Partners (EPD) formed a joint venture with Exxon Chemical Company to construct a propylene concentration unit that converts refinery-grade propylene into purer chemical-grade propylene, which serves as the raw material for lots of everyday items, including cosmetics, clothing, and blankets. Given EPD’s history, it’s unsurprising that they have been the leader in midstream when it comes to petchem projects. EPD has been clear about extending its value proposition into primary petrochemicals (see quote below). Per its latest presentation, the company has dedicated 23% of its $6 billion project expenditures backlog to petrochemicals. Petchem represents an opportunity to diversify EPD’s revenue stream while retaining stable cash flows.

In fall 2018, EPD ramped up its first 750,000 metric ton per year PDH facility to full capacity. The project’s expected completion date was originally late-2016, but construction was slowed due to cost overruns and Hurricane Harvey. In August, CEO Jim Teague suggested the firm is considering building a second PDH plant to take advantage of continued supply tightness and growing demand for propylene, and the company has continued to mention building a second and third PDH in recent presentations. EPD is also constructing an isobutane dehydrogenation (iBDH) unit in Mont Belvieu, which will be capable of producing 425,000 metric tons per year of isobutylene. The plant will double EPD’s existing isobutylene manufacturing capacity and will come online by the fourth quarter of this year. The facility is expected to produce feedstock that will be utilized at other EPD petchem plants downstream that make MTBE, crude isobutylene, and high purity isobutylene, thereby strengthening the company’s reach along the butane value chain.

Not to be left out, Inter Pipeline (IPL) is constructing the Heartland Petrochemical Complex, the first integrated PDH and polypropylene complex in Canada. In 2016, IPL closed its acquisition of Williams Companies’ (WMB) Canadian NGL midstream businesses as a launching point for the project. The plant will cost $3.5 billion – the single largest capital investment in IPL’s history – and will be completed in 2021. Management believes the plant has timely value given the facility’s cost competitiveness and the supply-demand imbalance domestically in the polypropylene market. Strategically, the project is a step towards materially diversifying and integrating the company’s petrochemicals and NGL business.

Framing the petchem opportunity.

With new petrochemicals projects planned and coming online, EPD and IPL are prime examples of North American midstream companies moving down the value chain into petchem. Many midstream companies are involved in fractionating NGLs and creating petchem feedstocks (such as ethane and propane), but far fewer are involved in taking those feedstocks and converting them into petrochemicals (such as propylene and ethylene). It’s possible we may see other companies expand downstream into petrochemicals given the expectation for long-term growth in demand for petrochemicals from emerging markets. However, the backlog of potential projects in traditional midstream infrastructure remains plentiful, and not every company has the skill set or desire to expand further down the value chain. In other words, petrochemicals will be a natural extension for some midstream companies but will not be a fit for others.

Bottom line

Petrochemical demand is expected to grow as emerging market economies continue to develop. Cheap feedstocks present an opportunity for midstream within petchem, particularly for companies with complementary assets. It is likely that select midstream companies will venture into petchem given the runway of growth opportunities for traditional midstream oil and gas infrastructure in North America. Regardless, petrochemicals can serve as a diversified and stable source of revenue for the midstream companies who make the push downstream.

{kind=link}

{kind=link}

{kind=link}