Summary //

- While the initial impacts of COVID-19 in the US first appeared at the end of 1Q20, the most severe impacts in terms of demand and oil production were squarely in 2Q20, which could impact midstream results – though likely to a lesser degree than for oil producers or refiners.

- After several dividend cuts in 1Q, a few more cuts are possible for 2Q payouts, but we view cuts as less likely overall. Similar to 1Q, we would expect sequential dividend increases to be few and far between.

- For some companies, 2Q20 results will be an opportunity to highlight the resilience and strength of their fee-based business model, while weaknesses may be on display for other names that are less well positioned. That said, investors may be willing to look past any weakness in 2Q given the extraordinary circumstances in the quarter and macro improvements.

Energy earnings season is right around the corner, with Kinder Morgan (KMI) kicking off midstream earnings on July 22. With 2Q representing the brunt of COVID-19 impacts on energy markets, quarterly results may be an opportunity for some midstream names to showcase their resilience, while names with a less-advantaged asset base or fewer contract protections may have their weaknesses on display. At a high level, investors likely understand the macro headwinds in 2Q and may be willing to overlook lackluster results given more solid footing for oil prices and the return of previously shut-in production. Overall, midstream should fare better than other sectors of energy given greater stability in 2020 EBITDA guidance and relatively minor 2020 EBITDA estimate revisions from analysts following oil’s collapse. While the focus of earnings calls will likely be the outlook from here, today’s note provides context for midstream investors heading into earnings season, including the impact of COVID-19 on US energy markets in 2Q, expectations for midstream dividends, and key topics of interest for calls.

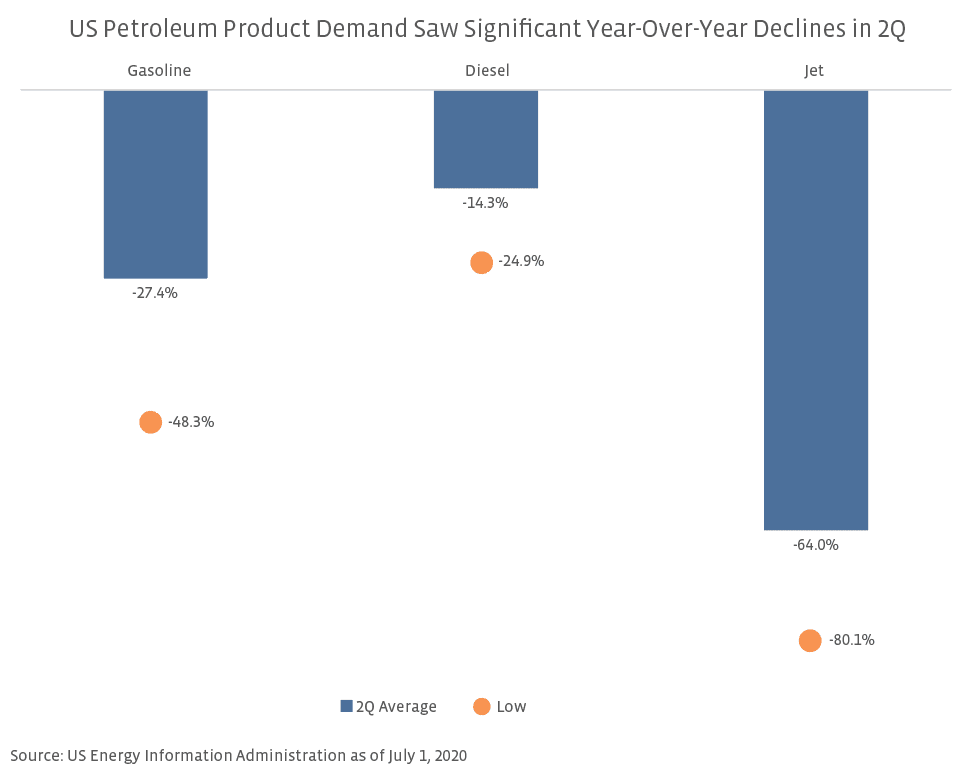

2Q represented the brunt of COVID-19 impacts on US energy.

While the initial impacts of COVID-19 first appeared at the end of 1Q, the most severe impacts in terms of demand and oil production were squarely in 2Q, which could impact midstream results – though likely to a lesser degree than for oil producers or refiners. Of course, the weakness in oil prices with WTI prices briefly trading in negative territory in April and production shut-ins will more profoundly impact the results of exploration and production (E&P) companies. However, lower volumes could weigh on midstream with the magnitude depending on contract protections like minimum volume commitments and trends in the basins served (read more). For the US in total, April oil production fell by 0.7 million barrels per day (MMBpd) sequentially to 12.1 MMBpd. As of July 7, the Energy Information Administration (EIA) is forecasting that May production fell further to 11.2 MMBpd and to 11.0 MMBpd in June. According to the second quarter Dallas Fed Energy Survey, 82% of the 165 oil and gas companies in the Eleventh Federal Reserve District responding shut in some production in 2Q20. Thirty-six percent of respondents expected to restore most of their production curtailments by the end of June, while 20% expected to restore the majority of shut-in volumes by the end of this month. To give one example, Noble Energy (NBL) indicated last week that most of its curtailed volumes would be brought back online by the end of July. Assuming oil prices do not backtrack significantly, shut-in volumes in the US should be largely restored in 3Q, though lower upstream activity is expected to result in annual oil production declines for the US in 2020 and 2021 per the EIA.

Turning to the demand side of the equation, US demand for petroleum products was down significantly in 2Q20 as COVID-19 countermeasures interrupted normal consumption patterns. Jet fuel was most severely impacted but only represented 10% of total US finished petroleum product demand in 2019. Gasoline and diesel also saw significant demand destruction as evidenced in the year-over-year numbers below. As discussed on their 1Q20 call on April 22, KMI management assumed in their revised 2020 EBITDA guidance that 2Q refined product volumes would be down 40-45% compared to prior assumptions. In their distributable cash flow sensitivity analysis from May 1, Magellan Midstream Partners (MMP) assumed a 25% decline in gasoline demand, 5% decline in diesel, and 70% decline in jet fuel for 2Q. On their 1Q earnings call, MMP management noted that their total refined product demand was down 26% in April, with their markets not suffering as much as other parts of the US. While demand impacts are clear for the US in total, earnings season will shed better light on impacts to companies given their unique footprints.

Could more midstream distribution cuts be on the horizon?

Several midstream companies responded to broader market headwinds by cutting their 1Q20 dividends to shore up their financial positioning. Altogether, 21 of 48 dividend-paying midstream companies reduced their payouts for 1Q20 (i.e. dividends paid in 2Q20 based on 1Q20 performance). While the absolute number of cuts was high, cuts were largely biased to smaller names in the space, with less than a third of the Alerian MLP Infrastructure Index (AMZI) and less than a quarter of the Alerian Midstream Energy Select Index (AMEI) reducing dividends by weighting (read more). Even with several cuts, the yields for the AMZI and AMEI remain elevated at 12.5% and 8.5% as of July 10, compared to the three-year averages of 8.8% and 6.5%, respectively.

Could more dividend cuts be on the horizon for 2Q20? Admittedly, the optics of cutting were better in April against the backdrop of heightened counterparty risk from plummeting oil prices, significant demand destruction, and headlines around oil production shut-ins, which made painful cuts more understandable and justifiable. If companies were in a position where a cut may have been needed, it was best to rip off the Band-Aid with the 1Q payout. We believe most companies recognized this dynamic while also wanting to take proactive steps to enhance financial flexibility given market headwinds and uncertainty at the time. In short, a few more cuts are possible for 2Q payouts, but we view cuts as less likely overall. Similar to 1Q, we would expect sequential dividend increases to be few and far between.

What are key focus areas for 2Q midstream earnings?

For some companies, 2Q20 results will be an opportunity to highlight the resilience and strength of their fee-based business models, while weaknesses may be on display for other names that are less well positioned. If the macro landscape and overall sentiment are improving, investors may be more willing to look beyond any weakness in 2Q results. Results may also not be as bad as feared. For example, Crestwood Equity Partners (CEQP) provided average 2Q throughput volumes on its Arrow System in the Bakken last week and noted that volumes significantly exceeded the company’s updated guidance from May. CEQP cited a 90% flow rate for the Arrow system currently and expects flow rates to reach 100% in 3Q.

Earnings season is about much more than the quarterly results, and this go-round will be no different. Investors will be interested in the outlook from here, updates or reaffirmations of past financial guidance, what companies are hearing from their customers, and how companies plan to address any challenges, such as recontracting in this environment (read more). Liquidity, leverage, and overall financial positioning are likely to remain in focus, though it bears noting that debt markets have been accessible for midstream (read more). Regulatory issues may be in focus given the recent cancellation of the Atlantic Coast Pipeline by Dominion Energy (D) and Duke Energy (DUK) and a court order to shutdown the Dakota Access Pipeline (read more), which Energy Transfer (ET) is actively appealing.

Beyond updates from energy infrastructure companies themselves, midstream investors will also likely be interested in production outlooks from exploration and production companies as well as refiner commentary on demand trends. With a dynamic macro energy backdrop, 2Q earnings season should be packed with interesting tidbits and helpful commentary to better understand the ongoing recovery across energy.

{kind=link}