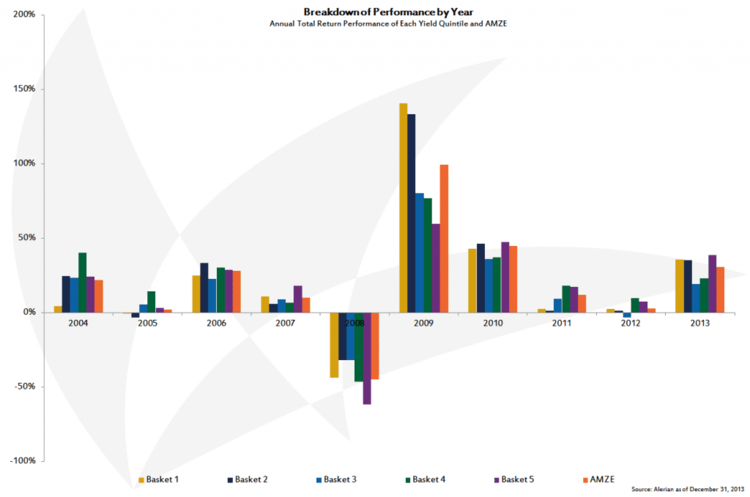

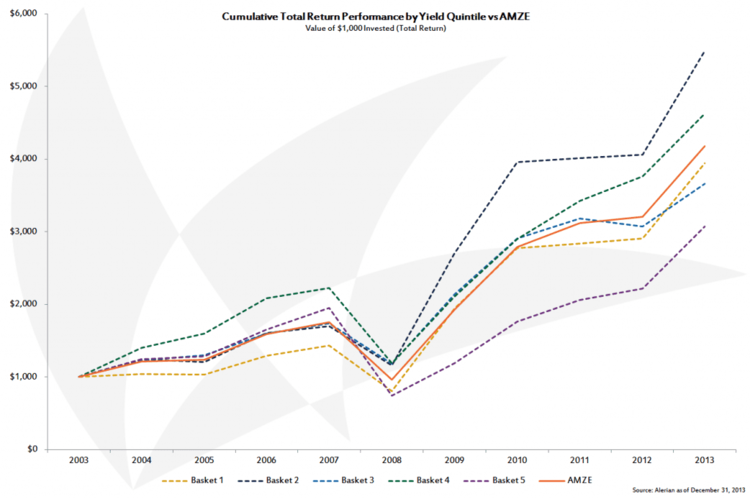

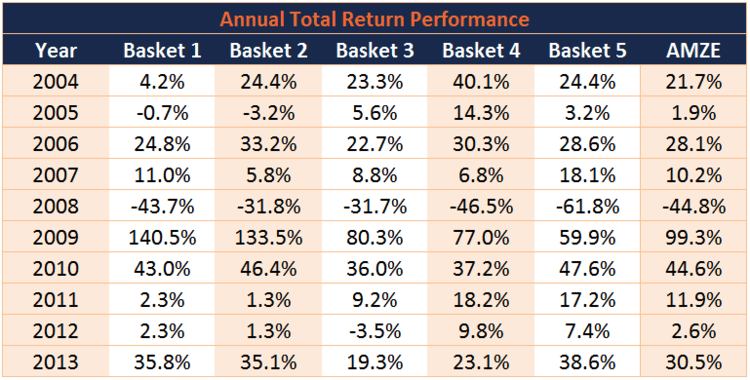

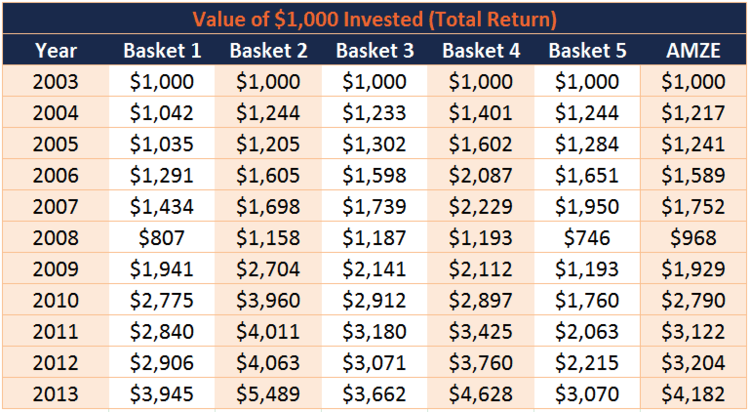

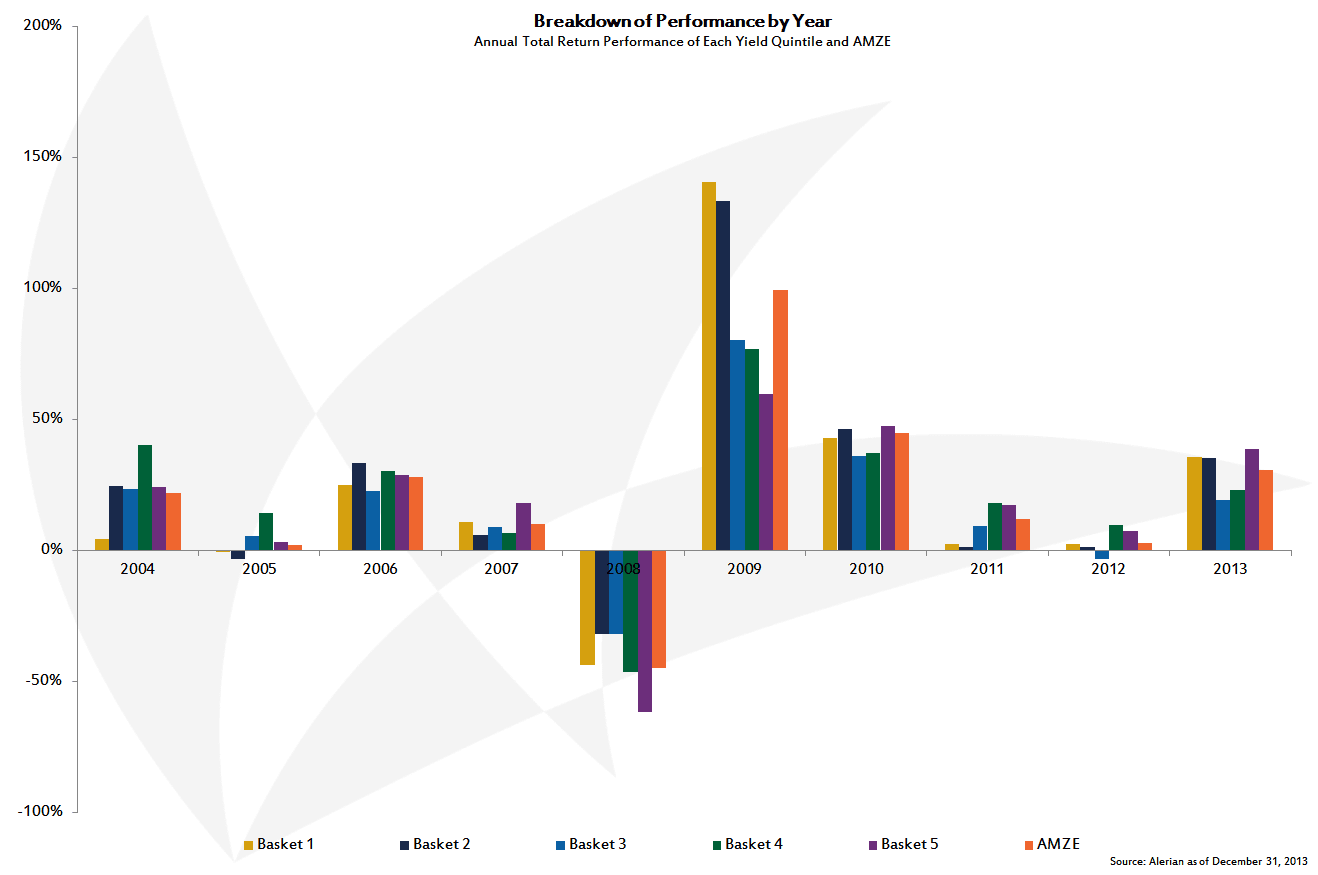

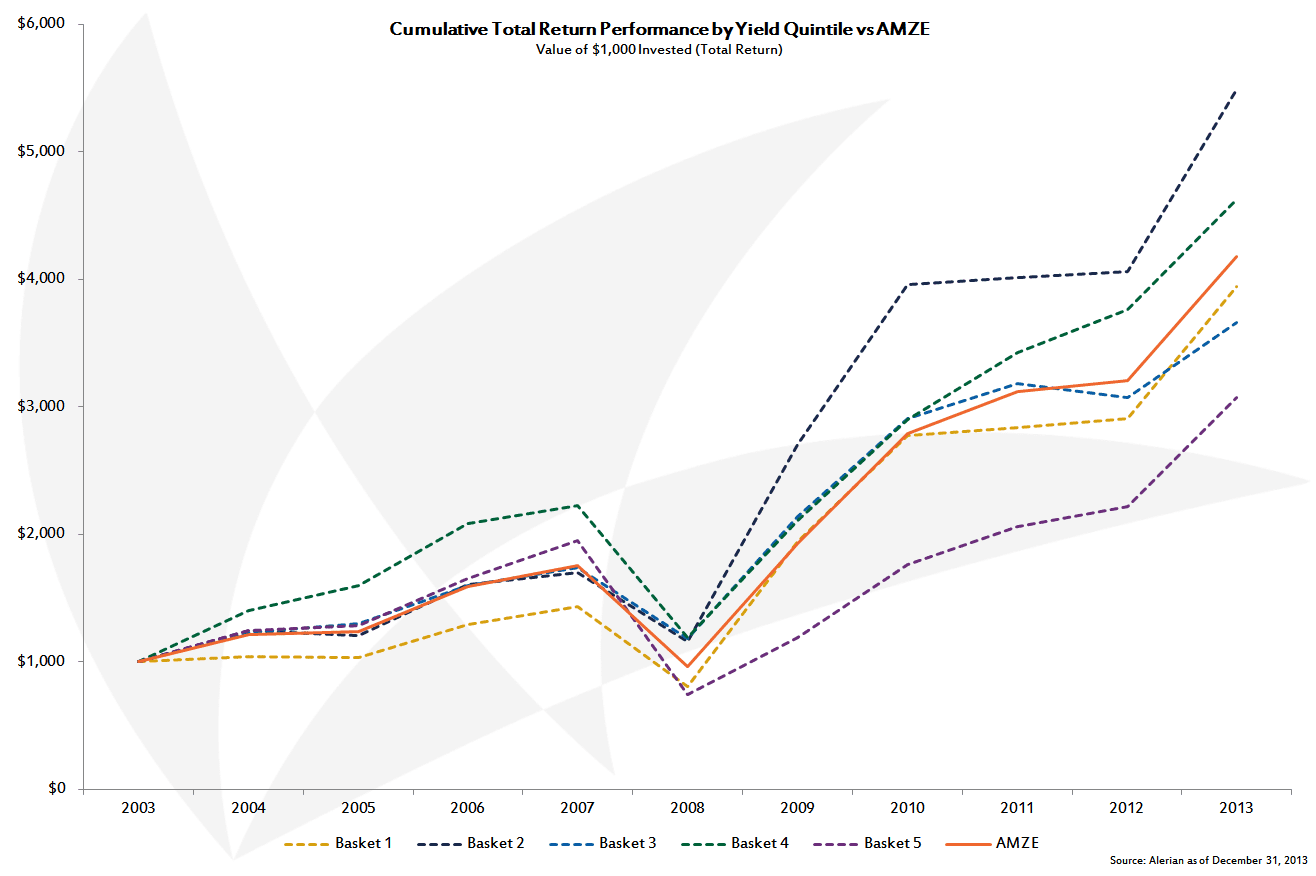

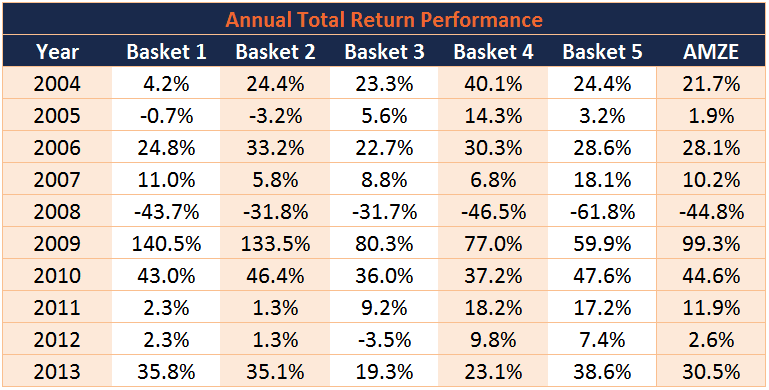

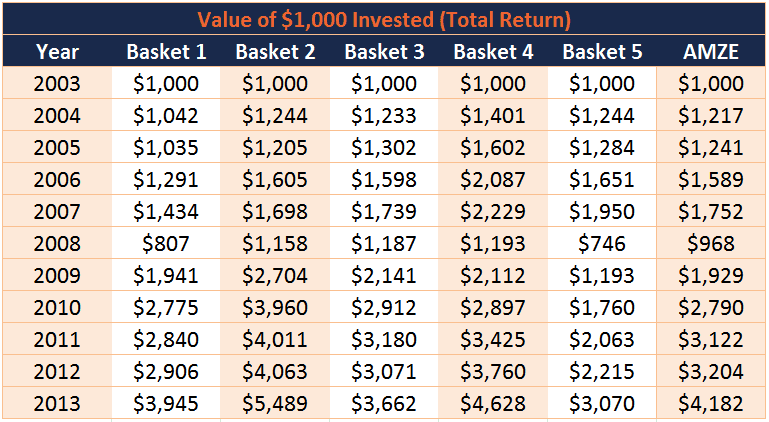

Looking at the performance from a total return perspective, we can see the effect of the risk of owning the highest-yielding names (Basket 1): namely, investors are taking on significant risk and sometimes the highest yields are signs of impending instability or low or no distribution growth, not success.

Compared to the simple price return chart, however, Basket 1’s performance pulls ahead of Basket 3, showing the reward potential of higher distributions. Basket 2, which is the second-highest quintile on a yield basis, outperforms even more dramatically. The outperformance is most notable during the recovery years of 2009 and 2010. Basket 4, the second-most conservative quintile, outperforms during years of steady growth. The lower yield can imply a lower cost of equity, which makes growth less expensive.

Interestingly, during the financial crisis in 2007-2008, Basket 5, containing what some consider to be the high-growth names, fell the most. Basket 5 lost 62% on a total return basis, compared to losses in the 30%-45% range for the other baskets. And despite being the best-performing basket during the four-year 2010-2013 period, Basket 5 failed to catch up to the other baskets and the AMZE. Again, investors in Basket 2 were rewarded for taking on additional risk without swinging for the fences.

In short, those MLPs with the highest yields will occasionally outperform, however, our data shows that they’ll more often underperform with added volatility. In fact, it is the MLPs with lower (but not the lowest yields) as well and those MLPs with higher (but not the highest) yields that outperform the index over the long term and for which investors are best paid for the amount of risk taken.

{kind=link}

{kind=link}

{kind=link}

{kind=link}