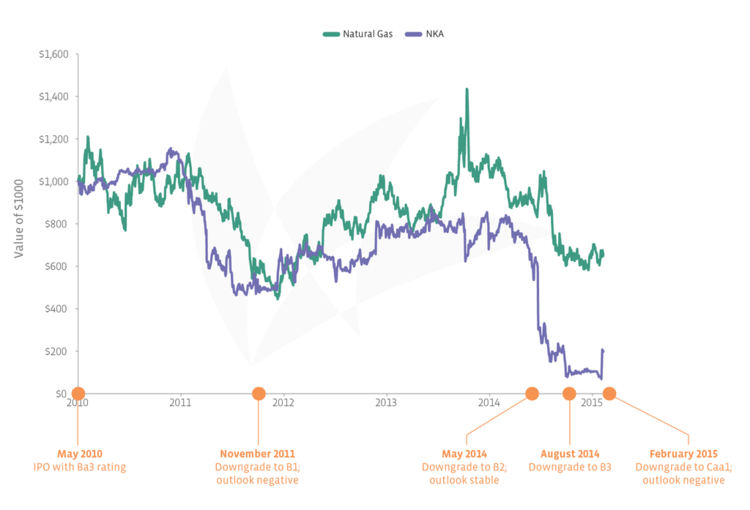

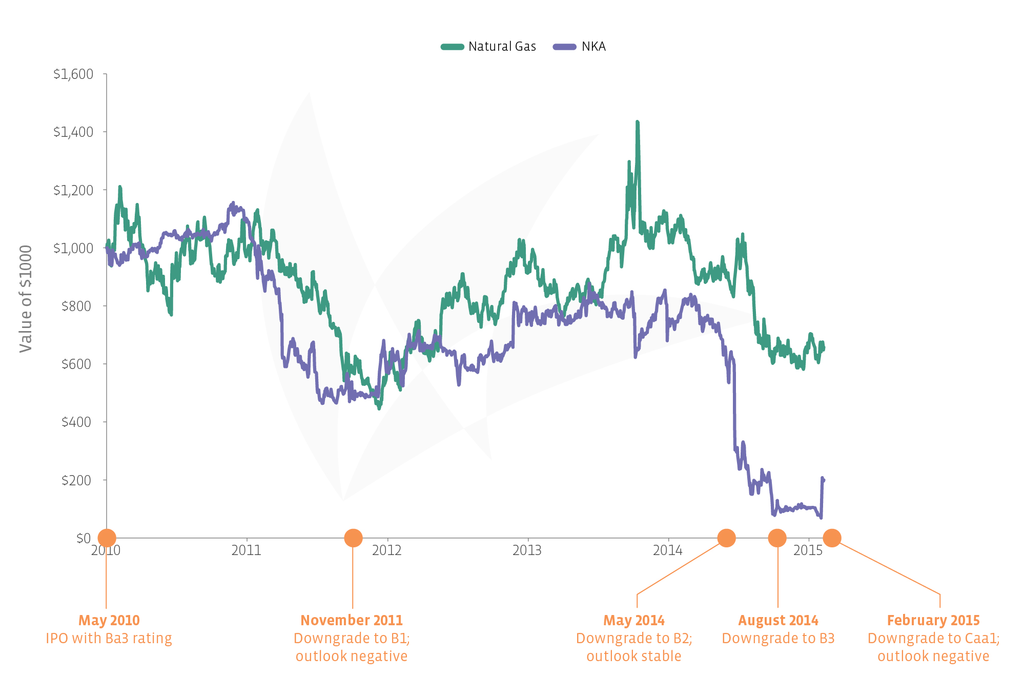

Take the example of Niska Gas Storage Partners (NKA). At the 2010 IPO, it had a Ba3 rating with a stable outlook. Moody’s warned that the MLP model required ongoing high payouts and an emphasis on growth. After 2011, expansion capital would need to be externally sourced, potentially leading to higher leverage. Commodity prices were tangentially mentioned as possibly restraining NKA’s rating due to its optimization business, and high initial leverage was noted.

At IPO, most of Niska’s working gas capacity was under firm contract—a quality that most MLP investors like. However, as the company added more storage capacity to their asset base, little of that incremental capacity was contracted. In a December 2010 presentation, Niska forecasted that total 2011 revenue would be 3% lower than 2010 revenue. However, this estimate hopefully assumed that seasonal gas spreads would improve throughout the year, since it was estimated that the first half of 2011 would contribute 38% of total 2011 revenue. Of this first half revenue, 47% would be from interruptible or short-term contracts. By March 2011, management forecasted that, on the low end, total 2011 revenue would be 8% lower than 2010. The low-end estimate was confirmed in May 2011, with 56% of total revenue now coming from interruptible or short-term contracts.

NKA’s share price then began to decline dramatically. Management reiterated their ability to grow organically and pay distributions, but would not provide guidance for 2012 due to concerns about the storage spread.

In November 2011, following a 50% decline in the unit price over six months, Moody’s downgraded NKA to B1 with a negative outlook. The agency was concerned about the compression of the summer/winter natural gas price spread, but the magnitude of the concern only resulted in a one-notch downgrade. The leverage ratio had crept up and was expected to be 6.2x in March 2012, up from 4.3x a year ago. Continued leverage above 6x could be cause for a further downgrade. NKA could only wait for the spread to improve, while continuing to pay those distributions so important to equity investors. The strategic location of their storage assets in California, Oklahoma, and Alberta, Canada was cited as supportive of the rating.

In November 2012, and then again in February 2014, Moody’s confirmed NKA’s B1 rating with a stable outlook. Moody’s downgraded NKA in May 2014 to B2 on lower EBITDA and an expected leverage ratio over 6x in fiscal year 2015, even though EBITDA was already falling in 2012 and 2013. Moody’s warned that a leverage ratio consistently over 6.5x could cause a further downgrade.

Three months later, with a leverage ratio at 7x due to sharply lower EBITDA, Moody’s downgraded NKA to B3 with a stable outlook.

NKA then proceeded to eliminate its distribution in February 2015, a huge negative for equity investors. Since no cash was being paid to equity holders, debt holders should have had greater confidence in their coupon payments. And yet, Moody’s again downgraded the company. The Caa1 rating reflected an expected fiscal year 2016 leverage ratio of 11×. Any upgrade would require significant, permanent EBITDA growth.

Last month, NKA announced that it would be acquired by Brookfield Infrastructure Partners (BIP). The seasonal gas spread never returned, partly due to gas-powered electricity generation increasing summer demand, and partly due to the shale gas revolution arriving in the Marcellus Shale, increasing supply and lowering winter prices for Northeast customers. NKA was not directly dependent on the price of natural gas, but the business model did depend on seasonal spreads. In this case, low volatility worked against an MLP.

By the time Moody’s downgraded NKA again and again, it was already too late for the equity investor. But not all companies that started with a speculative rating have fallen so dramatically. Can rating agencies help predict a company on the way up?

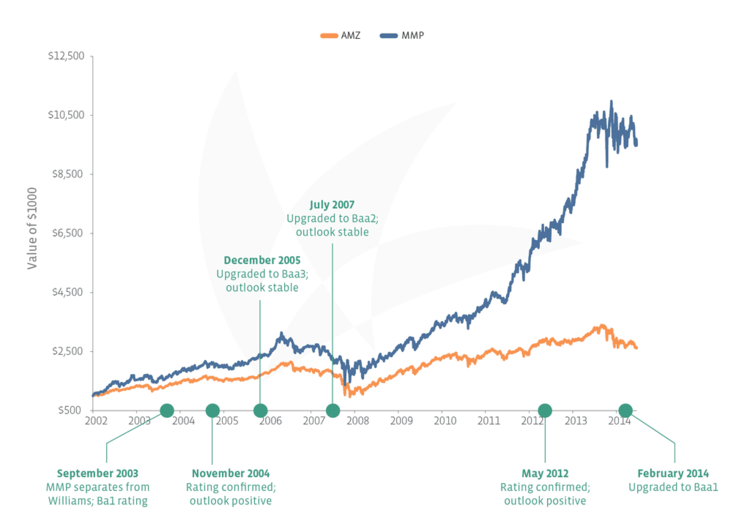

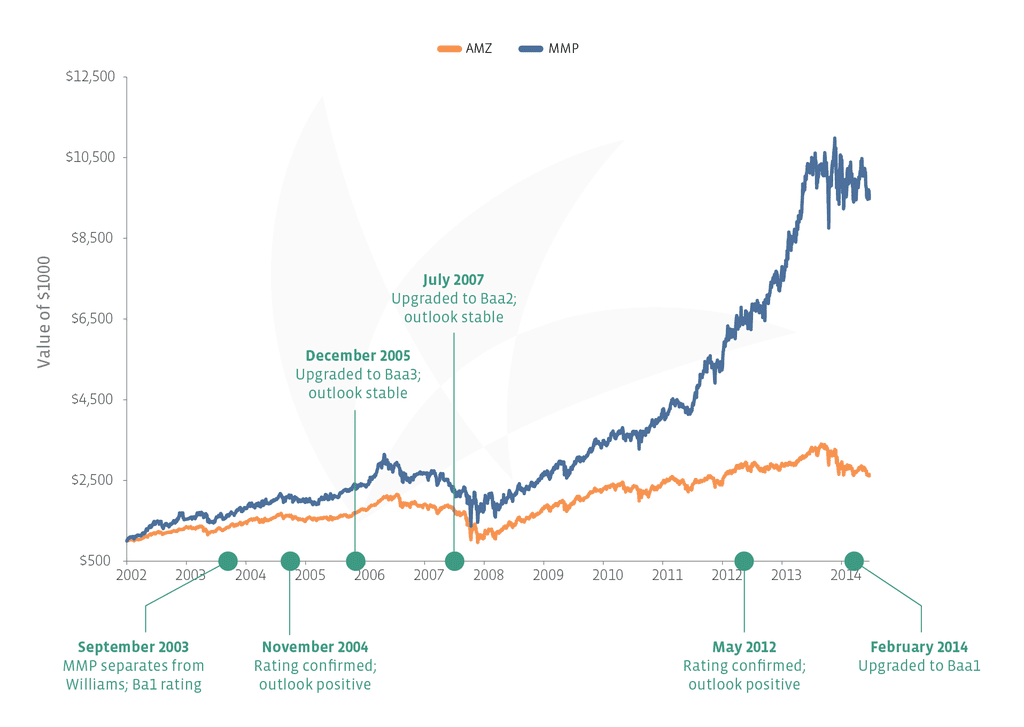

Magellan Midstream Partners (MMP)

In June 2003, Magellan Midstream Partners (MMP) became a standalone entity. In May 2004, Moody’s confirmed the previous Ba1 rating, noting that while Magellan had stronger credit metrics than its peers, it was still in transition and very young. Magellan also had a privately held GP in Magellan Midstream Holdings.

The initial rating was based on the stability and moderate growth in cash flows from the petroleum transportation and storage business, debt level relative to business risk and competition, and the size and geographic diversity of the company. However, Moody’s also took into account two factors that might introduce risk: (1) distributions were likely to increase, which would reduce available cash; and (2) a growth strategy that included acquisitions, which could introduce additional business risk. In other words, Moody’s considered MMP’s high cash balance to be a double-edged sword.

In November 2004, Moody’s changed MMP’s outlook to positive due to continued strong performance. Seven months later, Moody’s placed Magellan under review for a possible upgrade to Baa3, i.e. investment grade, and then upgraded the company with a stable outlook in December 2005. Magellan made the grade, but only after it had proven itself on the metrics mentioned earlier: performance, credit metrics remaining above peer average, and a five-year track record of consistent fiscal strategy and strategic focus.

In April 2007, Moody’s once again placed MMP under review for a possible one-notch upgrade. During this review, the rating agency took into account the change in ownership structure at its GP, which went public in February 2006 as Magellan Midstream Holdings (former ticker: MGG). Moody’s would also look at retired debt obligations at MMP affiliates and subsidiaries, margin growth, distribution increases, and business risk profile. In July 2007, Moody’s granted MMP a Baa2 rating, lauding the company for their organic growth, low exposure to commodity prices, and low leverage.

In 2009, MMP consolidated its general partner in an all-stock exchange, simplifying the corporate structure by remove the IDRs and the GP’s economic interest. The resultant lowered cost of equity is something that MLP investors love to hear, but there was no action on Moody’s part, as the agency simply affirmed the Baa2 rating in March with a stable outlook.

It wasn’t until May 2012 that Moody’s changed its outlook on Magellan from stable to positive. While Moody’s again reiterated the importance of track record, low business risk, and low leverage, the outlook change was due to MMP’s announced 2012-2013 capex strategy to expand its fee-based crude pipeline and storage businesses. Moody’s declared an upgrade to be possible provided the projects proceeded as planned with conservative distribution growth policies. Cost overruns or delays could be cause to return to a stable outlook, and additional business risk or rising leverage could be cause for a downgrade.

Moody’s upgraded Magellan to Baa1 in February 2014 based on the success of the plan mentioned above. The only mentioned caveats were that crude oil is subject to higher volume risk, and that there is declining demand for gasoline, which may affect MMP’s refined products businesses. Another upgrade was not expected unless MMP materially increased its size.

As implied by the narrative above, the rating upgrades were rewards for past operational and financial performance, not a prediction of things to come. In this way, debt and equity analysts value different things.

There are plenty of metrics Moody’s looks at when assigning ratings, but in the end, it almost always comes down to business risk and leverage. Solid growth prospects can help in achieving an investment grade rating, but there’s an emphasis on past performance, i.e. turning those prospects into reality. Geographic and asset diversity is important, provided it doesn’t raise the company’s overall risk profile. Cash hoards are tricky things. On one hand, they provide cushion. On the other hand, the rating agency worries that a company with a significant amount of cash will be itching to spend it. Distribution increases are great for equity investors, but they are viewed skeptically by rating agencies because less available cash flow puts bond coupon payments at risk.

If you are looking to make an investment decision based on a report from a rating agency, it’s probably best if that decision relates to your fixed-income portfolio. Otherwise, ratings moves tend to be retrospective, not predictive. As always, do your homework, get comfortable with the risks, and good luck out there.

{kind=link}

{kind=link}