The Runaway Success

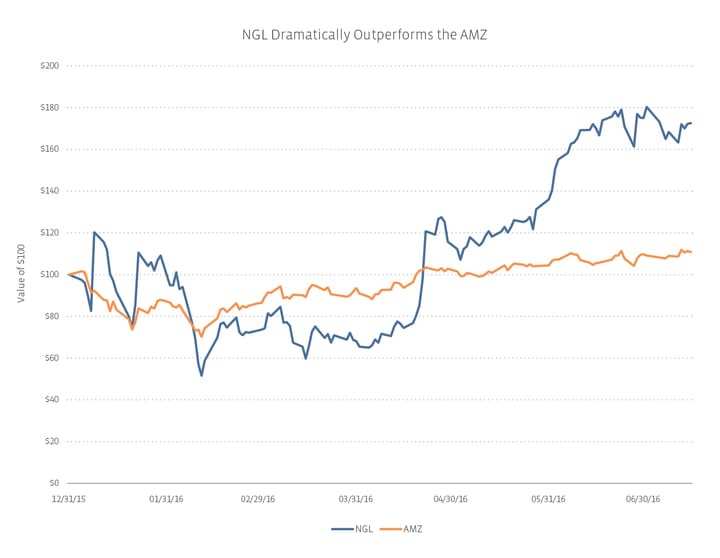

NGL Energy Partners (NGL) started 2016 with a declining unit price amid rumors of a distribution cut and in a disheartening macro environment. In December of 2015, management even felt the need to address the rumors. You’d hardly recognize it as a troubled, defensive company today and hardly believe how it got there. In early January, NGL sold a good asset, which is never an MLP’s first choice, but given the 75% return on a two-year investment, the stock jumped 30% that day. Still, it couldn’t escape general sentiment but did hire a new CFO. Within two months, it cut the distribution, and unit prices doubled. The announcement of fourth quarter results cemented its place as the highest returning MLP (in the AMZ) so far this year. (Results were generally in line with expectations, despite the pressure on commodity prices and warm winter. Additionally, the announcement reiterated previous 2017 guidance.) In the past six months, management took calculated risks that went against MLP conventions, but investors have quietly rewarded it for bold steps towards liquidity.

When the Growth Was Already Priced In

I’ve spoken before in this space about how, given a difficult macro environment, having a strong and supportive general partner can significantly benefit the MLP—it seems that dropdown stories have held up the best in the past two years. Imagine my surprise to realize that Shell Midstream Partners (SHLX) had lost about 20% so far during 2016. A major part of their growth story is dropdowns from the GP, Royal Dutch Shell (RDS), but despite the most recent acquisition being done at 8.8x EBITDA, and a recent 6.4% distribution increase quarter over quarter, the AMZ is still outperforming SHLX year-to-date. With RDS having an additional $30 billion of assets to divest over the next three years worldwide, and SHLX a natural home for those assets in the US, perhaps investors have already priced in the incredible amount of growth available here? Alternatively, perhaps investors took their SHLX gains to be redeployed into other MLPs.

The underperformance for 2016 is surprising in a vacuum, but consider, SHLX is still trading around a 2.8% yield as of July 15, 2016, implying that (using a valuation short-cut) investors are still very interested in owning SHLX. To explain 2016 performance, we look back to 2015, when the stock hit such a surprising year-end near-term peak that we should at least consider the possibility that it was traded up to boost portfolio performance results.

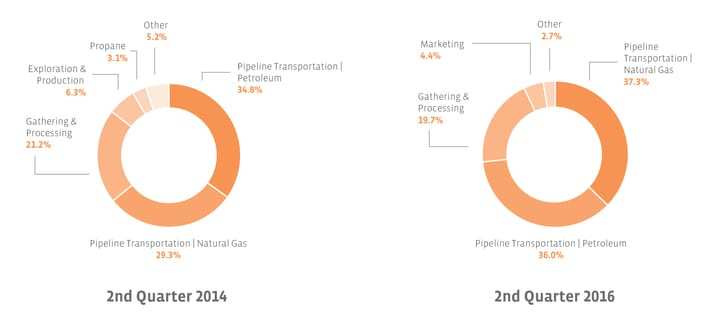

Investors Made Infrastructure Great Again

The difficulties of 2015 have forced the industry to be more streamlined and have more financial flexibility. The end result, in some ways, is a return to an asset class of yesteryear. We’re back to transportation MLPs overwhelming the smaller niche categories. E&P, Propane, and Other MLPs still exist, but investors have flocked to infrastructure MLPs. The comparative pie charts illustrate just how much the pipeline transportation MLPs have again begun to dominate the market cap of MLPs. Of course, we should note that these charts are not directly comparable; however, they do illustrate how much the contribution from non-infrastructure MLPs has shrunk.

We are almost certainly out of the woods in terms of the recovery, but the cycle has changed the industry. Amid the noise of distribution cuts and new projects and whether an MLP can raise capital, there is the signal of a stable, back-to-basics asset class.