Gasoline also experiences seasonal increases in demand during driving season – the period of high car usage in the US from Memorial Day to Labor Day. Gasoline inventories typically build in anticipation of driving season and draw through the summer. Refining utilization tends to be highest in the summer, increasing crude demand and refined product (gasoline, diesel, jet fuel) supply. Refineries in the US will typically perform maintenance in the fall and spring, which will lead to lower crude demand and lower production of fuels during those periods.

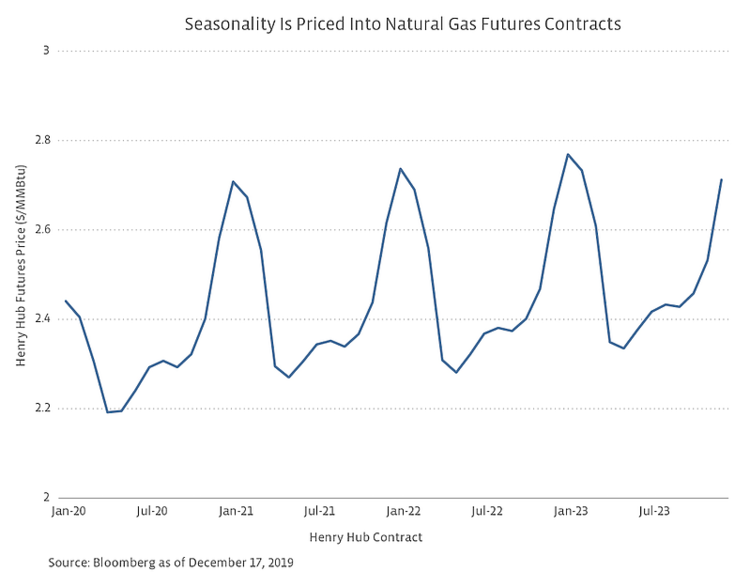

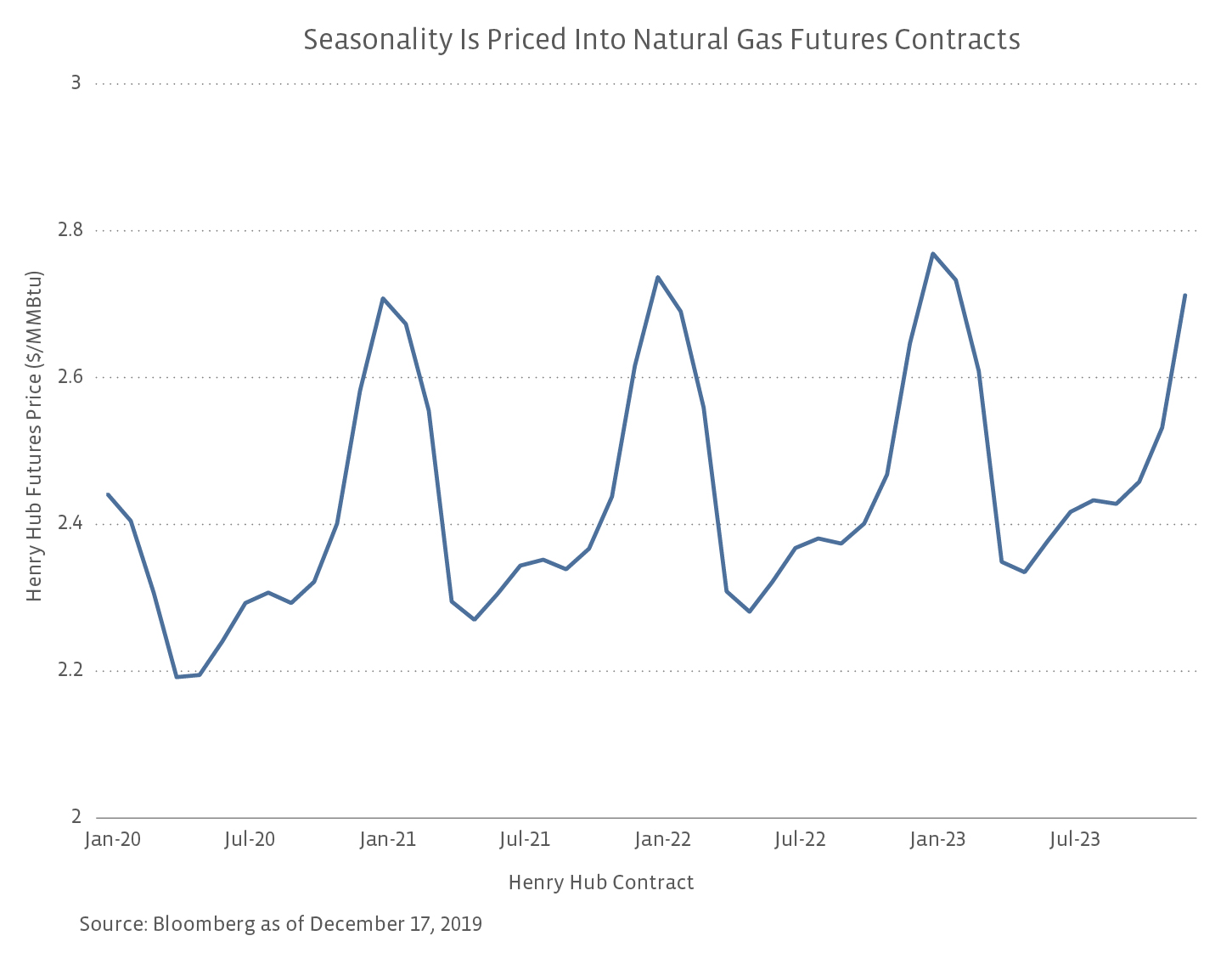

Natural gas liquids (NGLs) are also impacted by seasonality. Butane is a relatively cheap NGL that can be blended into gasoline to increase octane. However, due to environmental safeguards, butane is primarily blended into gasoline in the winter, with only nominal volumes blended from May 1 to September 15. Greater demand tends to drive higher butane prices in the winter. Higher gasoline prices in the summer are a factor of both increased demand from driving season and less butane blending as more expensive blendstocks must be used. Propane is another NGL impacted by seasonality, with demand increasing in September/October and winter due to its use in crop drying and as a space heating fuel.

In terms of oil and gas production, volumes tend to be more consistent throughout the year or generally growing for the US broadly. Barring a depressed pricing environment, producers will be incentivized to produce as much as is economically feasible at attractive returns. However, production can still be affected by seasonal factors. For example, hurricanes in the Gulf of Mexico can interrupt production as employees are evacuated from offshore platforms. In 2017, Hurricanes Harvey and Nate accounted for a combined loss of 12 million barrels of crude production. Setting aside oil and gas production, hurricanes can lead to refinery shutdowns, interrupting supplies of fuels. (As of January 2019, the Gulf of Mexico was home to 46% of US refining capacity.) In the winter, natural gas wells may experience freeze-offs, which is when liquids in gas wells freeze and block volumes from coming out of the well, thus lowering natural gas production.

Does seasonality matter for midstream?

To what extent does the seasonality of commodity prices and inventories impact midstream? In general, midstream is less susceptible to the financial impacts of seasonality as compared to its upstream and downstream counterparts. This is due to the fee-based business models of midstream companies. For example, the fees collected by pipelines are based on the volume moved and are independent of the commodity price. Often, pipeline contracts will include take-or-pay provisions or minimum volume commitments, ensuring the pipeline can collect specified fees even if the customer does not fully utilize its capacity. Similarly, customers agree to pay a fixed fee to access a certain amount of storage under a long-term contract, and fees collected are independent of price and the actual amount of storage used.

While perhaps less commonplace, some midstream businesses can be influenced by the seasonality of commodity prices or seasonality of demand. For example, Magellan Midstream Partners (MMP) provides butane blending services, with profits mainly generated in the first and fourth quarter of each year when butane can be more widely blended. Similarly, NGL Energy Partners (NGL) experiences seasonality in cash flows from its Liquids business, with operating losses or low operating income in the second and third calendar quarters, as the company builds inventories of natural gas liquids ahead of heating season.

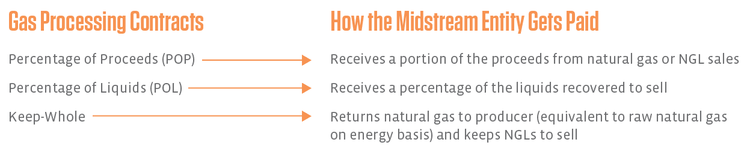

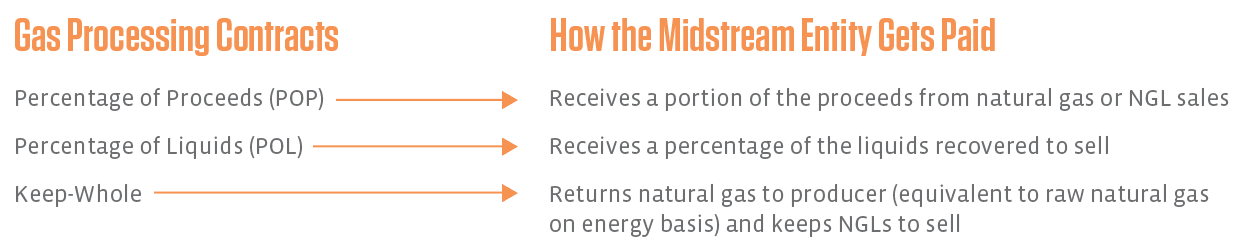

Midstream names involved in gas processing may be susceptible to commodity price exposure – and thus the seasonality of natural gas and NGL prices – depending on their contracts. While companies have tried to increasingly shift to fee-based processing contracts, there are multiple contract types with commodity exposure as explained in the infographic below (more detail here) with agreements varying by company. For example, 27% of Enable Midstream’s (ENBL) natural gas processing volumes in 2018 were under POP (percentage of proceeds) or POL (percentage of liquids) contracts and 6% under keep-whole contracts. For EnLink Midstream (ENLC), 9% of 2018 gross operating margin was related to POP and POL contracts. In 2018, 87% of MPLX’s (MPLX) gathering and processing net operating margin was from fee-based contracts. Midstream companies will likely continue to prefer fixed-fee contracts to limit exposure to commodity prices. When exposed to commodity prices, midstream companies will often employ hedges to mitigate the risk to cash flows.

Conclusion

Seasonality in demand for hydrocarbons is one of many factors that affects prices across the energy value chain. Midstream tends to be less exposed to price seasonality given its largely fee-based business model, though natural gas processing and NGL business lines can be areas with commodity exposure.

{kind=link}

{kind=link}