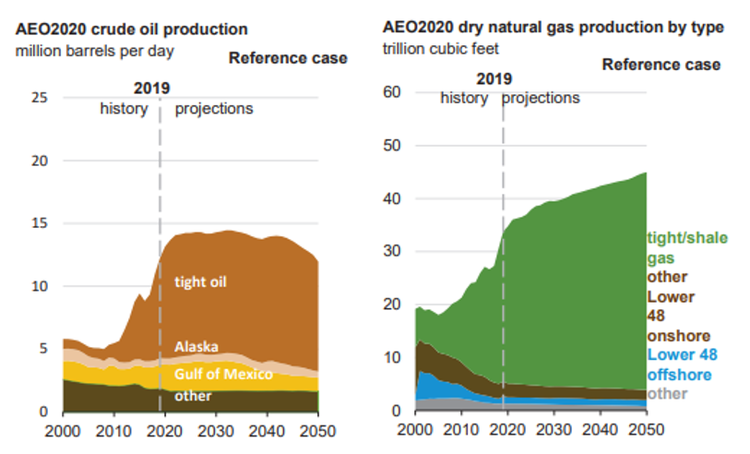

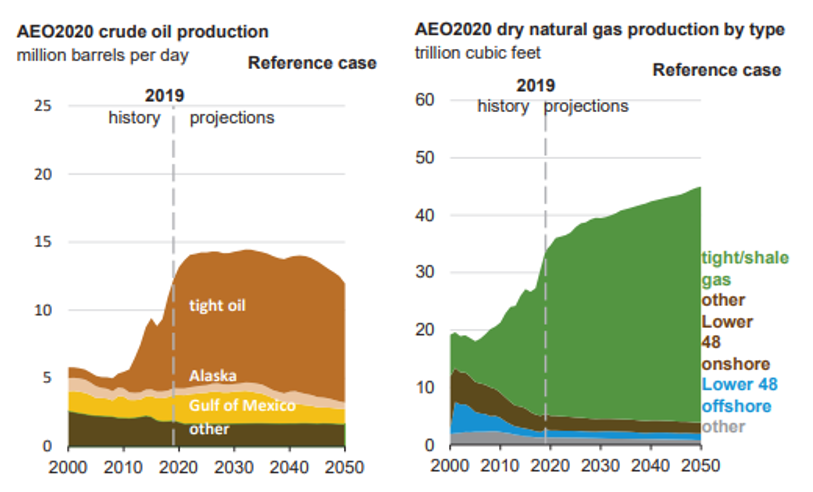

In the near term, oil and natural gas production growth is expected to moderate in 2020. Specifically, the Energy Information Administration is forecasting oil volume growth of 9.0% or 1.1 million barrels per day (MMBpd) this year. On an exit-to-exit basis, oil production growth is forecasted to be 0.5 MMBpd (comparing December 2019 to December 2020), which is less steep than the 0.9 MMBpd estimated exit-to-exit growth for 2019. Dry natural gas growth is forecasted at 2.9% or 2.7 billion cubic feet per day (Bcf/d) for 2020, which compares to estimated growth of 9.8% (8.2 Bcf/d) in 2019.

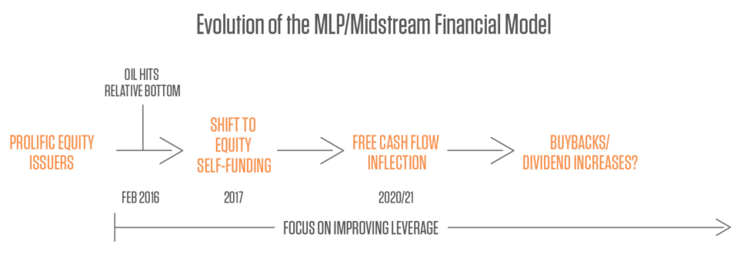

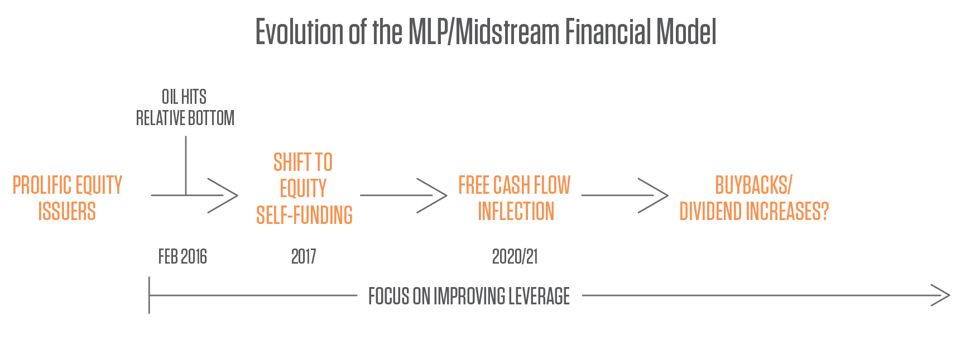

Financial Strategy: Self-funding equity to free cash flow to shareholder returns.

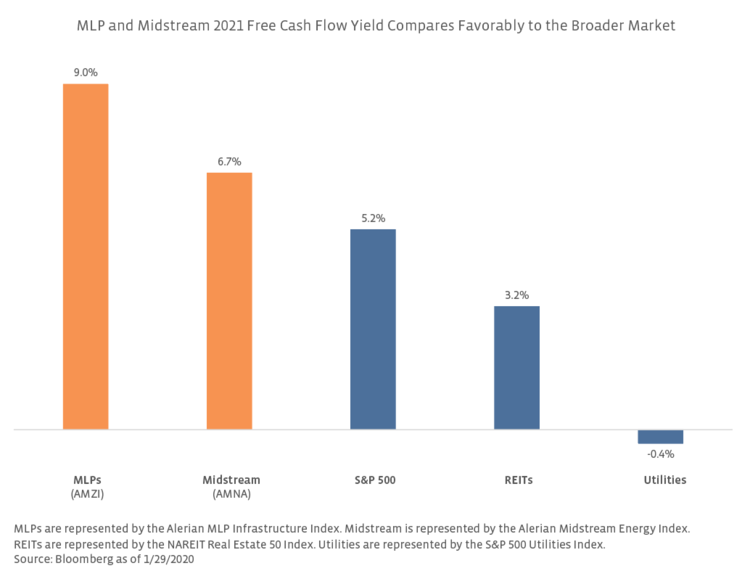

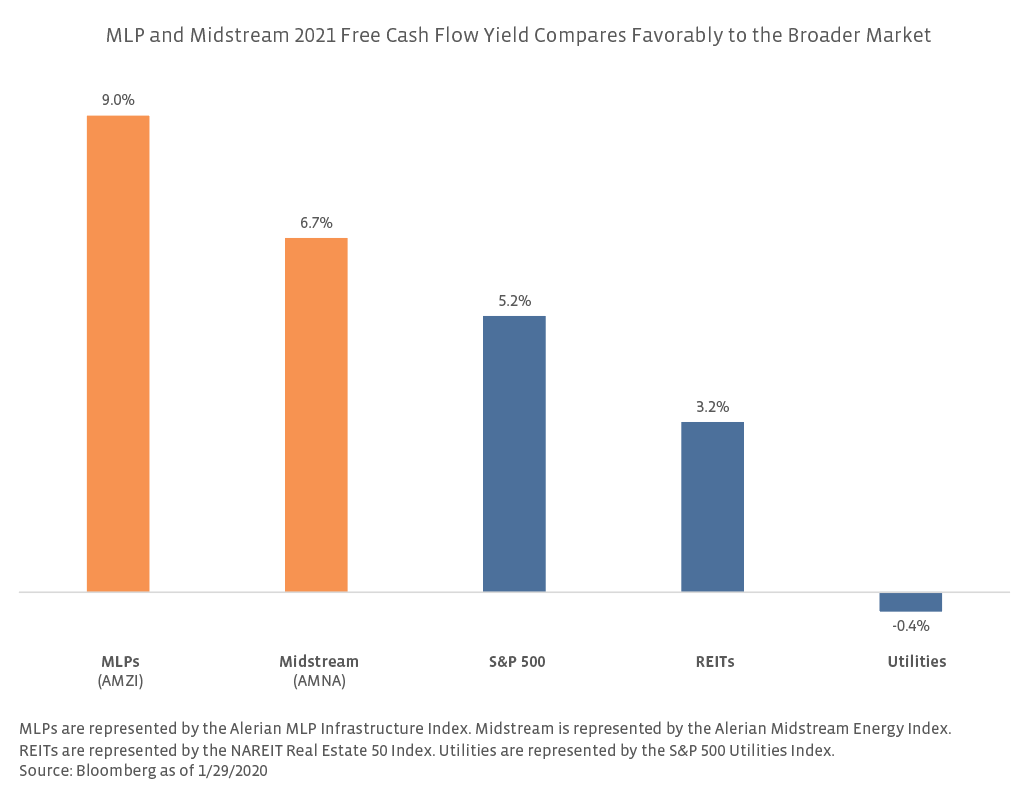

With US production growth moderating, midstream growth capital spending is declining and free cash flow has come into focus (read more). Free cash flow is the next step in midstream’s financial transformation, which has seen the space shift from a heavy reliance on equity markets prior to oil’s collapse to now largely self-funding equity. Midstream is beginning to reach an inflection point of generating free cash flow after dividends, with a few names likely to mark the milestone this year and more names following next year. This should pave the way for improvements like leverage reductions and potential increases in shareholder returns through buybacks or dividend hikes, similar to what was observed in the refining sector in recent years (read more).

Clearly, company progress on this roadmap varies, but many names are moving towards generating free cash flow after dividends, with a focus on increasing shareholder returns. Williams Companies (WMB) expects to generate excess cash flow this year after capital spending and dividends and has guided to a 5% dividend increase this year. With its 4Q19 earnings release last week, MPLX (MPLX) announced a goal to achieve free cash flow after distributions in 2021, noting the potential to reduce debt or pursue unit repurchases. Magellan Midstream Partners (MMP) has been self-funding equity for years, having not issued equity since 2010, and announced a $750 million buyback program last month. Enterprise Products Partners (EPD) plans to grow its distribution by 2.3% in 2020 and use 2% of its 2020 cash flow from operations for unit buybacks. These are just a few examples of a broader trend in the space.

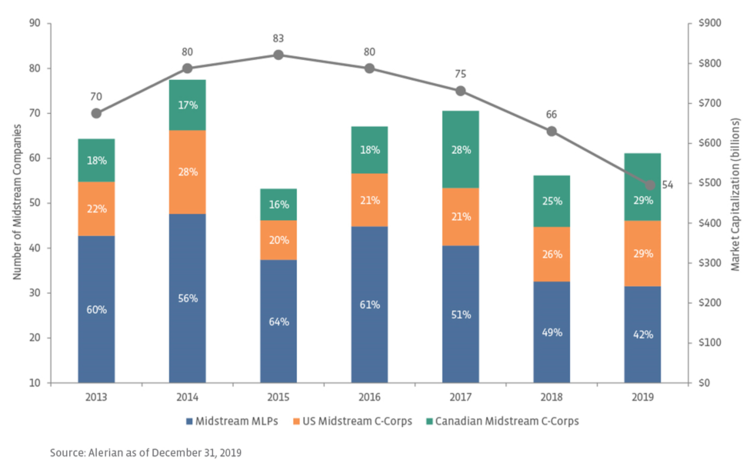

Midstream Universe: The evolving MLP and C-Corp mix.

The portion of the energy infrastructure market cap represented by MLPs continued to decline in 2019 due to C-Corp consolidations of MLPs, the acquisition of Buckeye Partners by private equity, and relatively weaker performance among MLPs compared to US and Canadian corporations. While we think MLP consolidations by C-Corp parents are largely behind the space, several other factors could impact this mix going forward. These include new midstream entrants to public markets (MLPs or C-Corps), private equity transactions, such as the pending acquisition of Tallgrass Energy (TGE), and underlying performance (will MLPs play catch-up to C-Corps after lagging in 2019 or continue to lag?). Of course, midstream investors are also watching to see if any large MLPs decide to convert to a C-Corp, which could have a notable impact on this mix.

While we can’t predict how this chart will change in coming years, it is important to note the implications of the current landscape for investors. With MLPs less representative than in the past, a 100% MLP product no longer provides broad midstream exposure. However, for investors primarily interested in yield, a predominately MLP ETF or mutual fund would maximize tax-deferred yield. A RIC-compliant fund, which includes 25% MLPs, would provide broader exposure to energy infrastructure, assuming the holdings in the other 75% are midstream corporations. A RIC-compliant product also tends to be more total-return focused, given that the 25% cap on MLPs results in a lower yield (read more on MLP access products).

Valuation: Midstream should focus on mainstream metrics.

With the evolution of the midstream space, valuation metrics are also shifting away from an overemphasis on yield and use of MLP jargon like distributable cash flow to more widely used metrics. To that end, the chart comparing MLP yield to the 10-year Treasury was removed from Alerian’s website last year and replaced with an EV/EBITDA chart. (The need for a fresh approach to MLP valuations was discussed extensively in our white paper from April 2019.) With many midstream names approaching free cash flow generation after dividends, free cash flow yield may gain more traction for valuing midstream companies going forward. MLPs and midstream firms should continue to cite more widely accepted valuation and financial metrics to better accommodate a broad investor base.

ESG: Likely to remain a focus for investors and companies.

With ESG considerations factoring more into investor decisions, midstream has accordingly begun to focus on ESG principles and improving disclosures of ESG-related items (read more in our ESG white paper). Progress should continue to be made on this front. MLPs have made headway in eliminating incentive distribution rights (IDRs) to improve governance, but other areas for improvement include board independence and unitholder voting rights. Typically, MLP unitholders are not able to vote in board elections, with only a few MLPs allowing unitholders to vote. With the ESG emphasis likely here to stay, midstream should focus on being ESG-friendly by providing relevant disclosures. This could be helpful in potentially attracting new investors.

Bottom Line

To sum up the State of Midstream, the tailwinds for the space include a constructive long-term outlook for US energy production and exports and improving financial prospects as free cash flow supports potential increases to shareholder returns. The future makeup of the midstream universe remains a known unknown with many factors impacting the MLP vs. C-Corp mix. Regardless of structure, midstream should continue to adopt more user-friendly financial metrics and improve ESG-related disclosures. Progress in these areas would complement the space’s free cash flow profile and ideally help attract new investors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}