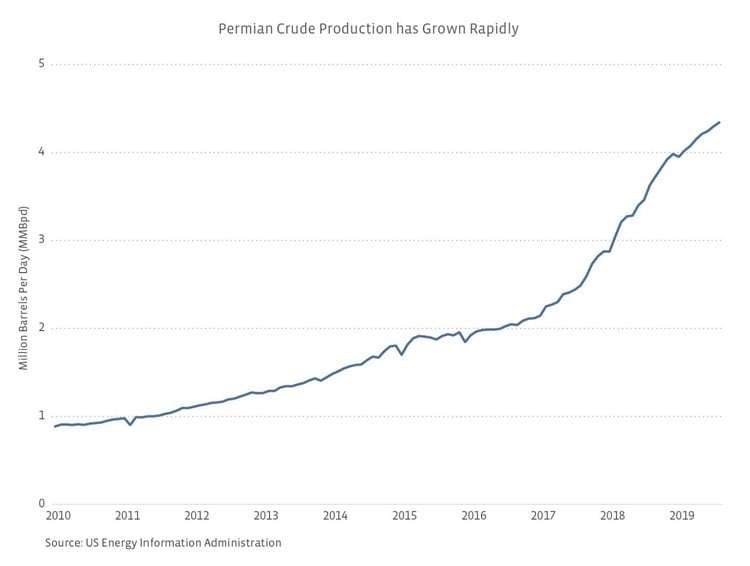

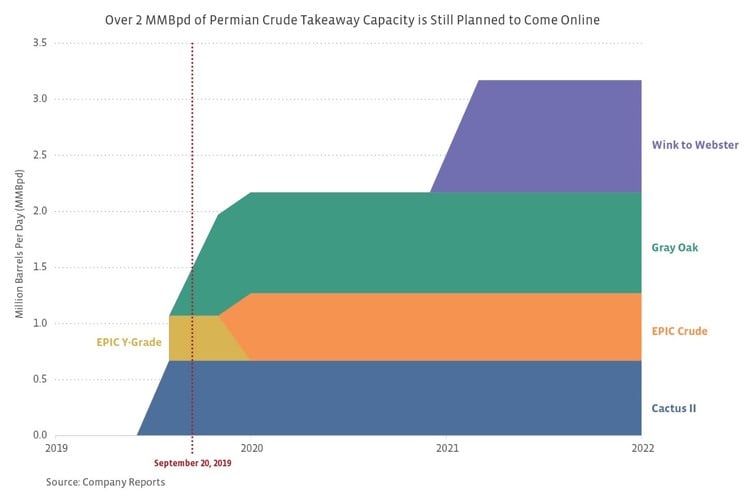

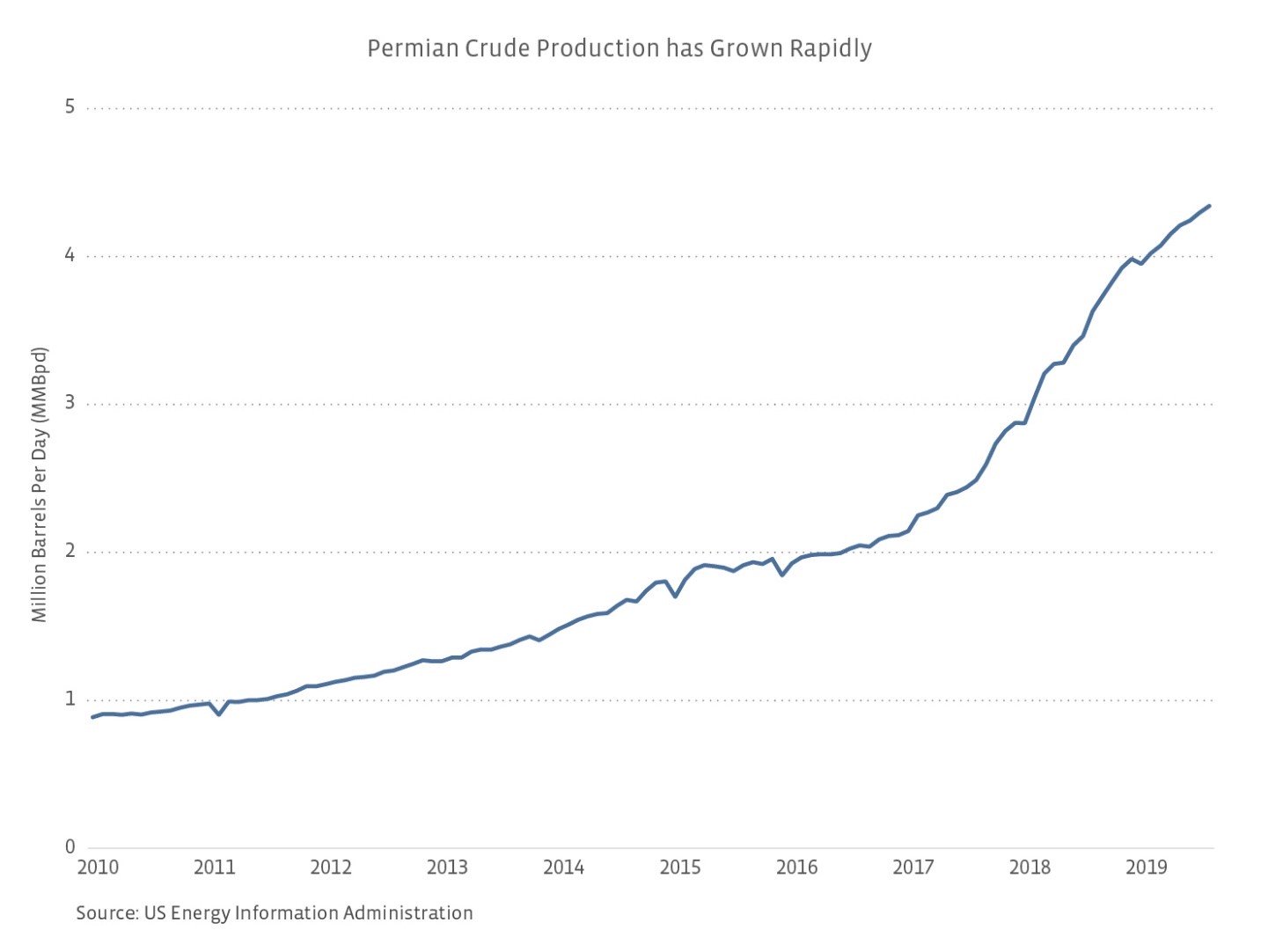

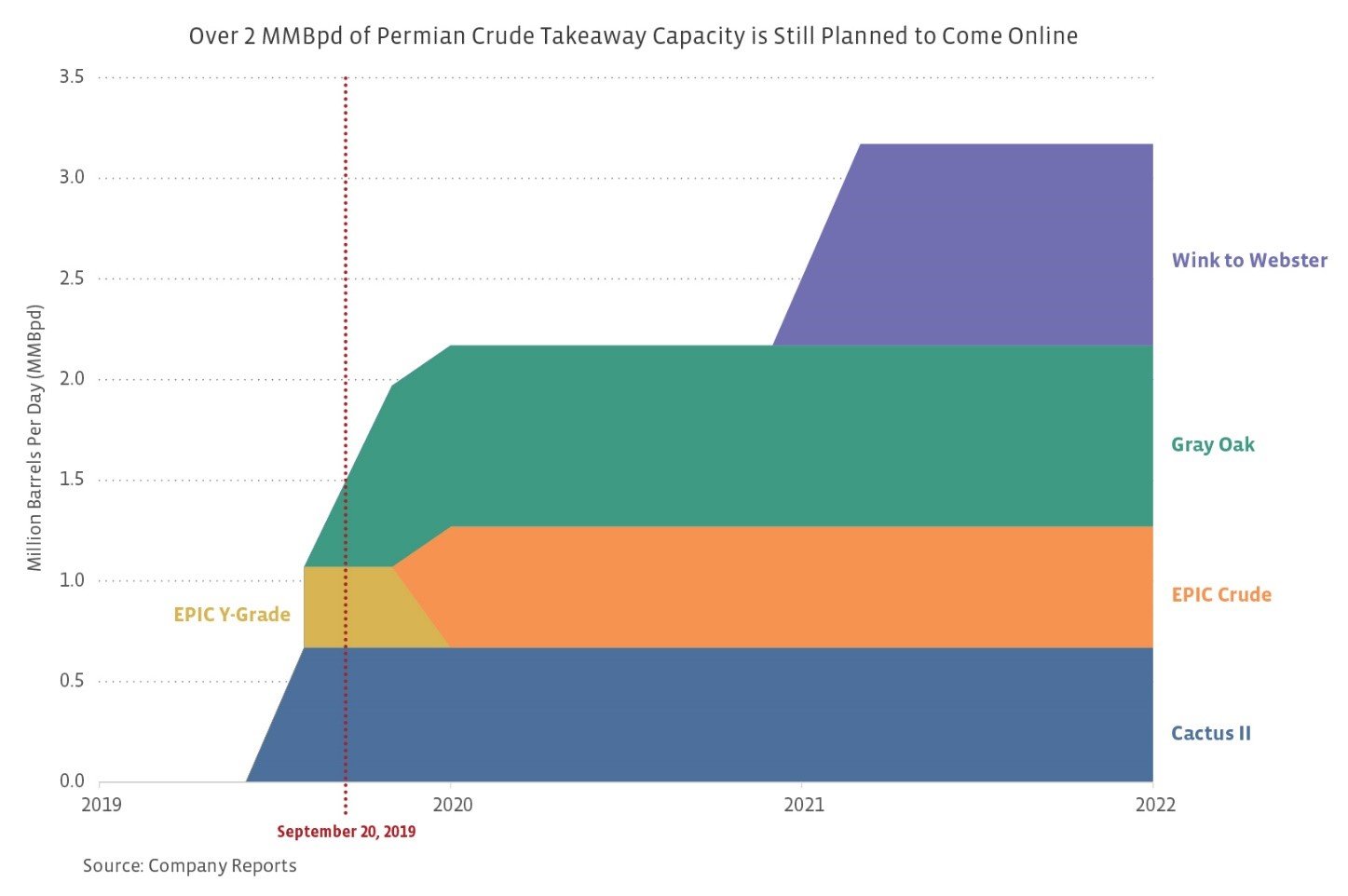

Things have begun to turn around as new infrastructure comes online. In August, crude shipments began on PAA’s Cactus II pipeline and EPIC Midstream’s EPIC Y-Grade Pipeline within less than a week of each other. These two projects have provided a much-needed outlet for West Texas crude, adding over 1 MMBpd of takeaway capacity from the Permian to the Gulf Coast. Looking forward, Enbridge (ENB) and Phillips 66 Partners’ (PSXP) Gray Oak Pipeline will add another 900 thousand barrels per day (MBpd) of takeaway capacity by the end of year. EPIC Y-Grade, which has been temporarily converted to crude service, will be converted back to NGL service once the 600-MBpd EPIC Crude Pipeline comes online in January. Further down the line, the Wink to Webster Pipeline, a joint venture between ExxonMobil (XOM), PAA, MPLX (MPLX), Delek (DK), Lotus Midstream, and Rattler Midstream (RTLR), will add another 1 MMBpd of Permian-to-Gulf Coast takeaway capacity in 2021. Altogether, more than 2 MMBpd of crude pipeline capacity will be added to the Permian Basin through 2022 on top of the 1 MMBpd takeaway capacity that went into service last month.

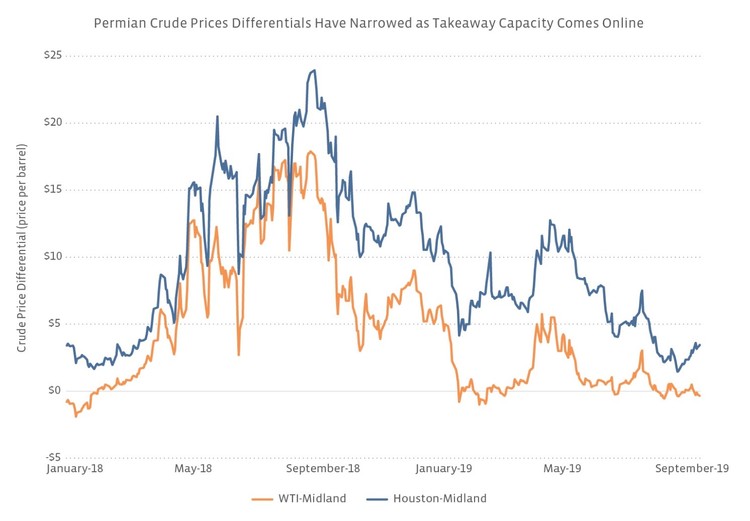

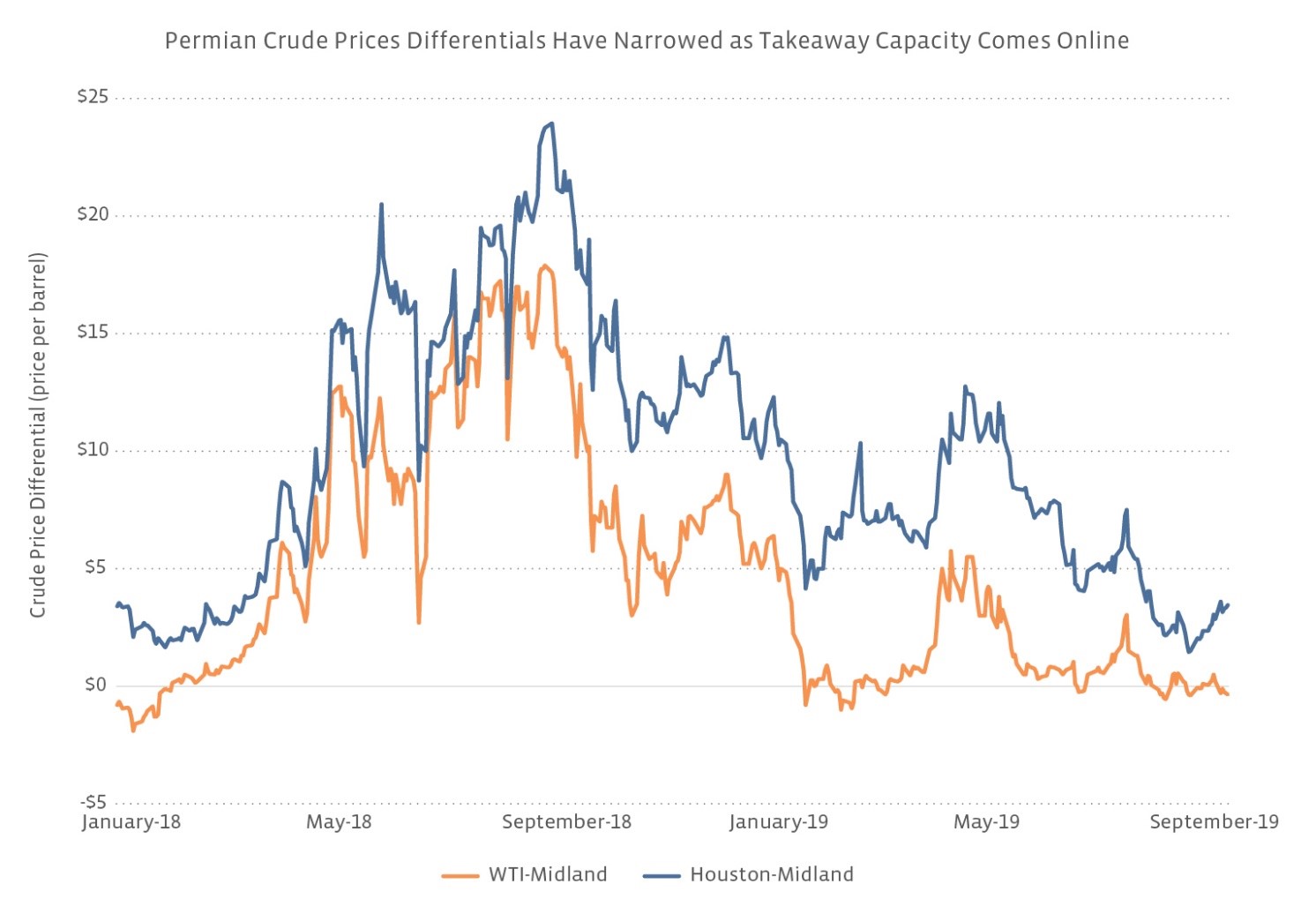

New infrastructure has supported Midland crude prices

Not only does additional infrastructure coming online benefit midstream companies, it has supported crude prices at Midland, Texas, as well. Crude spreads widened out significantly last year as a result of inadequate pipeline capacity and rapidly growing production but have since narrowed significantly. As of September 20, crude oil at Midland is trading at a $0.35 per barrel (bbl) premium to WTI Cushing, a dramatic shift from a nearly $18/bbl discount in August 2018. Houston-Midland differentials have also narrowed to $3.45/bbl after blowing out to nearly $24/bbl last summer. The chart below shows both the WTI-Midland and Houston-Midland crude price spreads since 2018.

While narrowed spreads are indicative of the end of takeaway constraints in the Permian, they don’t mean that opportunities in the basin no longer exist. PAA forecasts that production in the Permian will grow by 3.3 MMBpd from 2019-2023, accounting for more than 65% of total North American production growth. This growth will create further demand for energy infrastructure. On the downside, midstream companies that have capitalized on favorable Permian differentials cannot do so at current spreads. The Supply and Logistics (S&L) segment drove PAA’s outperformance in 1H19 thanks to arbitrage opportunities in the Permian, but the partnership expects a meaningful reduction in S&L going forward due to shifts in crude spreads. This reduction was anticipated, and the S&L segment is more of an added bonus for midstream companies rather than the backbone of their businesses.

Opportunities exist beyond crude oil as well. The Permian has also seen rapid growth in natural gas production; August 2019 production of 14.7 billion cubic feet per day (Bcf/d) is nearly twice that of production just 3 years ago. Natural gas prices at the Waha Hub, located in West Texas, have traded at an average discount of $1.81/MMBtu to Henry Hub this year and briefly fell into negative territory, signaling a need for additional takeaway capacity. Kinder Morgan (KMI) is currently planning 6 billion cubic feet per day (Bcf/d) of additional Permian natural gas takeaway capacity through three long-haul pipelines. The first of the three pipelines, the Gulf Coast Express Pipeline, is expected to come online within the next few days. The Permian Highway Pipeline will add another 2 Bcf/d of capacity in 4Q20, and the third pipeline, Permian Pass, has yet to reach final investment decision. The decision will be contingent on demand from producers, but KMI’s management has said that the project is moving along.

Additional Permian supply creates midstream opportunities further downstream

Not only does new infrastructure benefit midstream companies and Midland prices, it benefits crude exports. Outbound crude shipments from Corpus Christi, Texas, hit a record high of over 1 MMBpd in September, compared to a year-to-date average of 500 MBpd, as a result of additional volumes from Cactus II and EPIC Y-Grade. Energy infrastructure companies will facilitate the US’s increasingly important role as an energy exporter as incremental crude production from the Permian creates more opportunities for export infrastructure.

Several midstream operators have recently announced crude export projects. During its 2Q19 earnings call, Energy Transfer (ET) announced that it is in discussions to build a new crude export facility that would connect to its existing Nederland terminal. Additionally, the partnership’s acquisition of SemGroup (SEMG) will give ET ownership of the Houston Fuel Oil Terminal, a crude and refined products terminal at the Houston Ship Channel, which it plans to connect to its existing Nederland Terminal through the newly announced 500-MBpd Ted Collins Pipeline. EPD announced a slate of expansion projects at the Houston Ship Channel in July that will increase its export capacity for crude oil, among other hydrocarbons. Separately, the partnership announced long-term agreements with Chevron that will underpin construction of Sea Port Oil Terminal, an offshore crude export terminal in the Gulf of Mexico. Finally, NuStar Energy (NS) began loading Permian crude for export from its Corpus Christi North Beach Terminal in August and completed a short pipeline that connects Cactus II to its Corpus Christi terminal. Midstream companies will continue to benefit from additional Permian supply at the Texas Gulf Coast.

Bottom Line

New Permian takeaway capacity has helped to relieve the basin’s long-running takeaway constraints and provides midstream companies with additional sources of fee-based cash flows. As additional supply moves downstream, midstream companies are well-positioned to take advantage of crude export opportunities on the Texas Gulf Coast.

{kind=link}

{kind=link}

{kind=link}