In the Permian, natural gas prices have been particularly challenged, even reaching negative levels at times this year. Currently, prices at the Waha hub in West Texas are trading more than $1/MMBtu below prices at Henry Hub – the delivery point for the NYMEX natural gas futures contract. The discount is expected to narrow temporarily in the coming months based on futures, as Kinder Morgan’s (KMI) Gulf Coast Express Pipeline (GCX) is expected to enter service in late September, adding 2 billion cubic feet per day of takeaway capacity. On the crude side, some Permian producers have likely deferred activity in anticipation of additional pipeline takeaway projects such as Plains All American’s (PAA) Cactus II and the EPIC pipeline (read more), which are expected to begin providing takeaway this month. With crude prices being the bigger driver of Permian well economics, the addition of crude takeaway capacity could be supportive for activity levels going forward. Through August 9, Midland crude prices are up ~35% this year compared to high-teen gains for WTI Cushing and oil prices at Houston as crude discounts have narrowed.

What are the implications for midstream?

Combining weak natural gas prices with upstream’s focus on capital discipline and returns, it is not surprising to see producers pumping the brakes on activity in Appalachia or having deferred activity in the Permian in anticipation of pipeline capacity additions. Of course, this decline in activity can have implications for the growth outlook for midstream. Some midstream companies with gas-focused assets adjusted their 2019 volume or financial guidance with their 2Q results, reflecting changed expectations for gas volumes based on producer activity. The appendix to this piece provides company-specific updates for select midstream names with natural gas exposure. Much like their upstream counterparts, midstream companies are emphasizing capital discipline and cost-efficient operations in today’s gas price environment.

To be clear, not all gas pipelines are negatively impacted by weak prices. On their recent call, Williams (WMB) made a point of differentiating between “demand-pull” pipelines which benefit from low gas prices. Gathering pipelines can be thought of as supply-push and are more likely to be impacted by reduced producer activity as a result of lower natural gas prices. On the other hand, a gas pipeline supplying a utility customer or an LNG export facility would not be expected to see any impact from lower prices.

It also bears mentioning that midstream counterparties and geographic exposure matter. Exposure to one basin or one producer customer can be a disadvantage when headwinds arise. Midstream names with diversified asset bases across different basins and different commodities are better positioned to weather issues like the weakness in natural gas prices. For example, Energy Transfer (ET), which falls into Alerian’s Pipeline Transportation ǀ Natural Gas classification, raised its 2019 EBITDA guidance with its 2Q19 results, while WMB, which is classified as Gathering & Processing, reaffirmed 2019 EBITDA guidance.

What’s the long-term and near-term outlook?

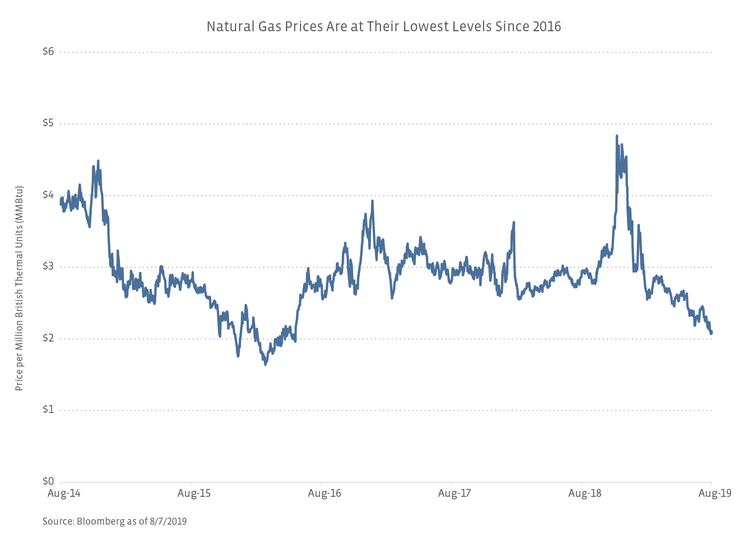

The long-term fundamental outlook for natural gas production growth in the US and global gas demand remain strong and are driven by the industrial sector and coal-to-gas switching. The current price environment reflects a combination of factors, including some that are transient (LNG export project delays, weather). It was only a few months ago that the Canada Pension Plan Investment Board invested in WMB’s Marcellus and Utica midstream assets at an estimated 14x multiple (read more). Current price weakness should not be interpreted to mean that existing midstream gas assets are distressed, but instead that the price environment has implications for near-term growth. The EIA forecasts that natural gas production will continue to grow this year but fall slightly in 1Q20 in a delayed response to today’s low price environment, with growth expected to resume in 2Q20. Producers reducing activity in response to low prices is a healthy step towards restoring balance to the market.

In the near term, midstream can continue to focus on cost efficiency and capital discipline. In general, lower volume or financial guidance is better received when accompanied by announcements of reduced capital spending in the impacted business. This is similar to what has been seen this earnings season with exploration and production companies being penalized for lowering production guidance but maintaining capital spending plans.

Bottom Line

Weakness in natural gas prices has caused producers to recalibrate growth plans, with some implications for midstream names. The long-term growth outlook for natural gas production remains intact, but prices may impact growth in the near term until balance is restored. For midstream, moderating production growth may result in slowing volume and EBITDA growth, requiring a focus on cost efficiency and capital discipline. Midstream names with a diversified asset and customer base are likely better positioned to weather the implications of near-term price weakness.

Appendix

Altus Midstream (ALTM) lowered its 2019 adjusted EBITDA guidance range to $70-85 million from $75-95 million. Lower gathering and processing volumes were reflected in the revision, though management noted the midpoint of guidance would have been unchanged if not for a $7 million expense related to the EPIC pipeline that was expected to be included in capital spending. Apache (APA), which deferred some gas production at Alpine High starting in April due to price weakness, plans to return deferred production to sales with the start-up of GCX and reiterated its 4Q19 Alpine High production target of 100,000 barrels of oil equivalent per day. Recall, ALTM lowered forward guidance in February 2019 as APA slowed investment at Alpine High. ALTM noted that activity at Alpine High could be reduced next year relative to its 2020 guidance if commodity prices remain weak.

Antero Midstream (AM) expects adjustments to Antero Resources’ (AR) completion techniques to require less water, resulting in a $25-35 million impact to AM’s adjusted EBITDA in 2020. However, cost savings will allow AR to maintain its 10% target compound annual growth rate for production. Continued production growth and an expansion of AM’s produced water business is expected to largely offset the $25-35 million EBITDA impact. On a separate note, in an 8-K filing yesterday, AM announced a $300 million share repurchase program.

EnLink Midstream (ENLC) lowered 2019 adjusted EBITDA guidance at the midpoint from $1.13 billion to $1.085 billion, citing more modest activity in Oklahoma and North Texas as well as a shift in timing for Permian producer activity. Moderating Oklahoma activity (namely in the STACK) was attributed to weaker commodity prices, including for gas and NGLs, given the mixed production profile of the play.

EQM Midstream Partners (EQM) slightly lowered the midpoint of its 2019 adjusted EBITDA guidance to $1.335 billion from $1.4 billion, reflecting lower EBITDA from its water business and slight changes in gathered volumes. With new management in place at EQT, which represents EQM’s largest customer, EQM deferred updating long-term guidance until it receives greater clarity from EQT. On its 2Q19 call, EQT mentioned the possibility of lower production volumes in the near to medium term, but indicated that a long-term development plan should lower capital needs for Equitrans (ETRN), which is EQM’s parent, supporting free cash flow generation.

Noble Midstream Partners (NBLX) tweaked its EBITDA guidance range for 2019 from $245-270 million to $245-255 million, indicating expectations to be on the low end of the guidance range initially provided. The tightened range reflects revised expectations for DJ Basin gathering and water delivery volumes and contributions from equity investments. Total gathering and sales volume is expected to be 9% higher in 2H19 relative to the 1H19 average. NBLX also lowered 2019 capex guidance to $150 million from $195 million, representing a 23% decrease.- WMB reduced its forecast for Northeast gathering volume growth for 2019 from ~15% to 13%, and 2020 growth is estimated at 5.5%. Previously, WMB had guided to a compound annual growth rate of 10-15% for Northeast gathering volumes from 2018-21, but noted on the 2Q call that 2020 growth was expected to moderate from 2019. Management said that growth capital spending in the Northeast would also slow down. Importantly, WMB reaffirmed companywide 2019 EBITDA guidance and 5-7% long-term EBITDA growth.

Western Midstream (WES) lowered 2019 adjusted EBITDA guidance from $1.85 billion to $1.70 billion (both at the midpoint) in part due to lower natural gas and NGL prices impacting its Wyoming assets, where there are legacy percentage-of-proceeds and keep-whole contracts (read more). WES indicated they have 7% commodity exposure in the natural gas part of their business. WES cited lower Delaware Basin volumes, particularly for gas gathering and processing, as the largest contributor to the lowered guidance and also attributed the decrease to revised revenue recognition estimates for cost of service contracts.

{kind=link}

{kind=link}