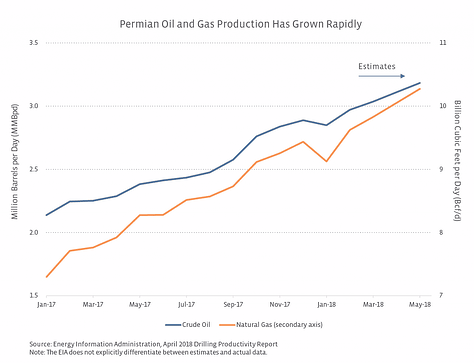

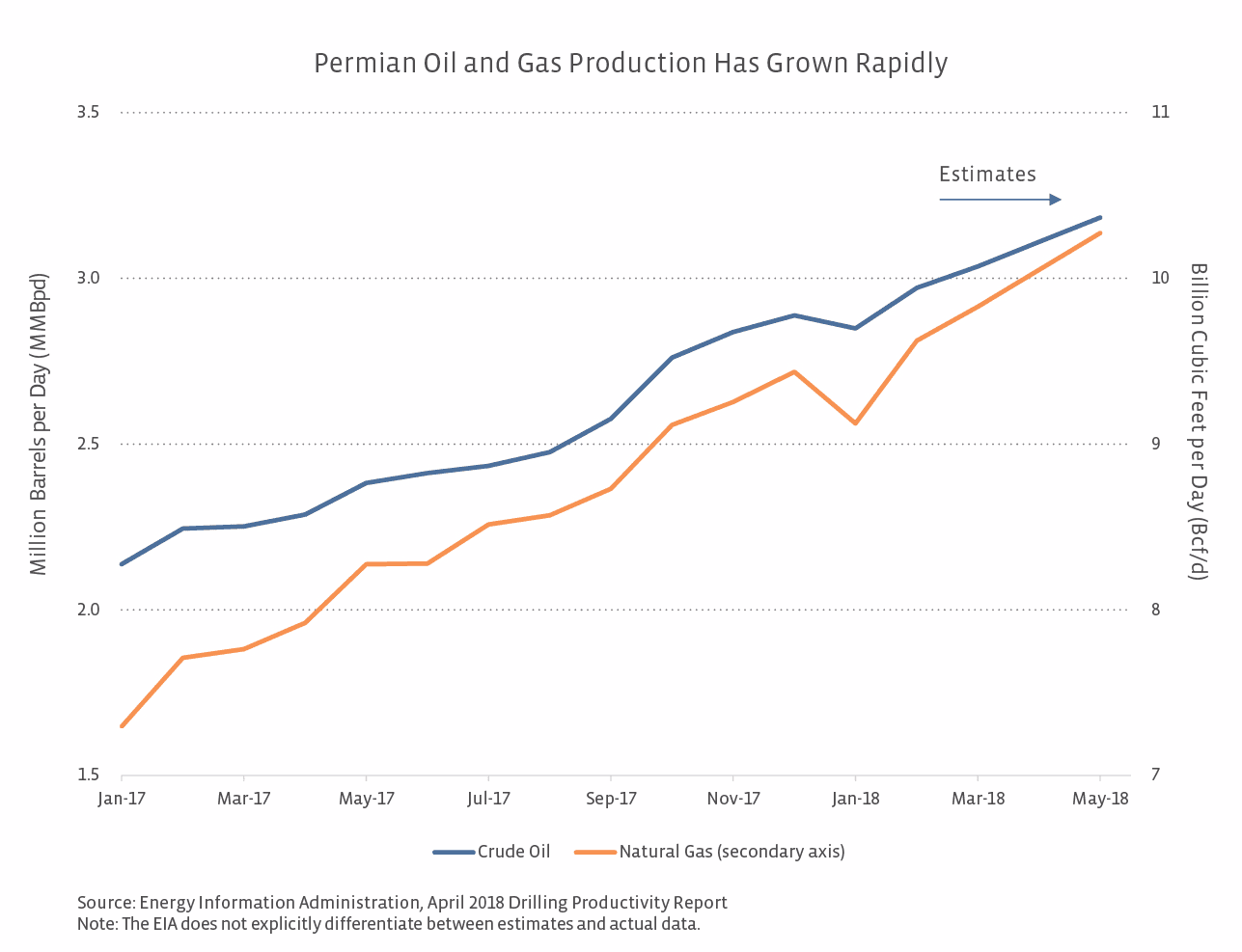

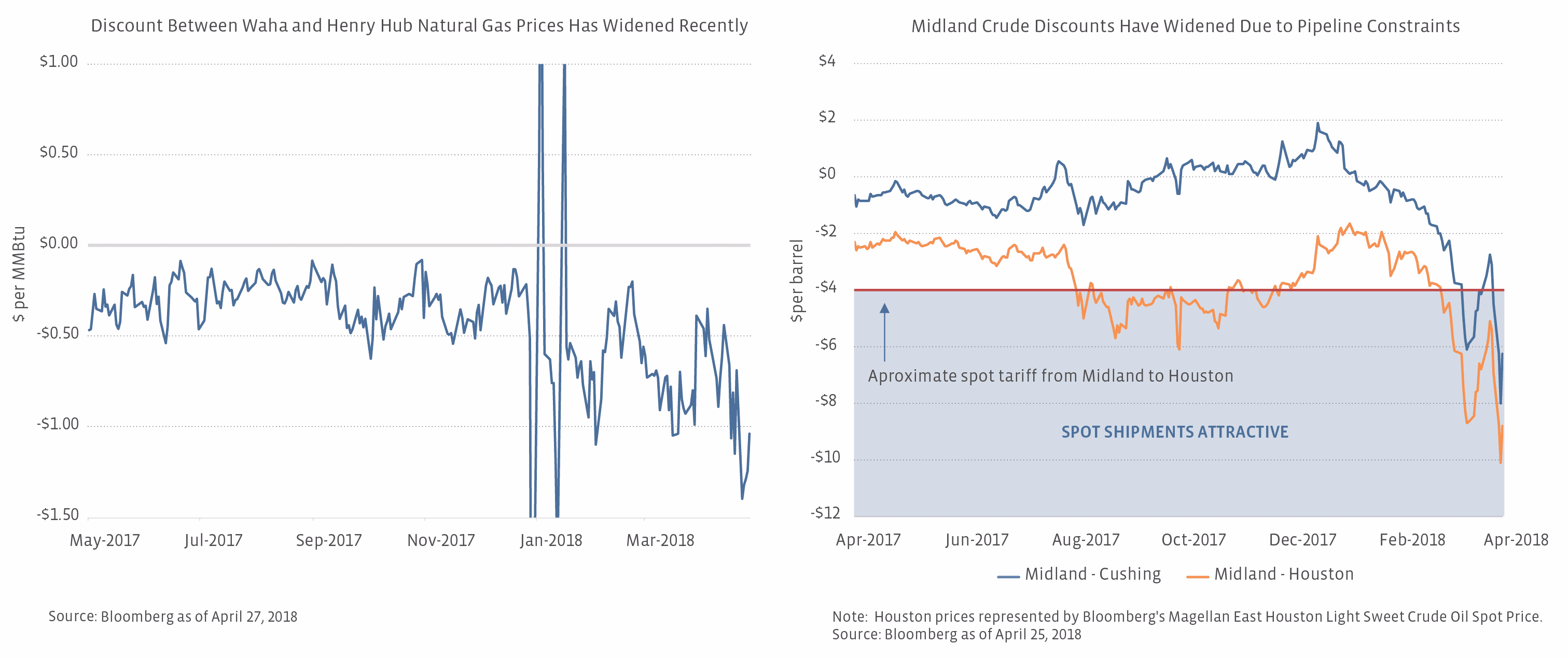

All this production growth has been hard to keep up with in terms of pipeline capacity for both crude and natural gas. Additionally on the crude side, seasonal refinery maintenance lowered demand for Midland crude, as Valero’s (VLO) management discussed on their recent earnings call. As a result, discounts have widened for Permian crude priced at Midland and natural gas priced at the Waha hub relative to benchmarks, as shown in the charts below.

Is producer pain midstream’s gain?

The discounts for Permian crude and natural gas are certainly frustrating for producers. Keep in mind that there is an additional cost to move crude or natural gas to the hub (Midland for crude or Waha for natural gas) using gathering pipelines (and/or trucks for crude), which further cuts into the profits of the producer. Before you start feeling too bad for producers, keep in mind that Midland crude prices were in the high $40’s and low $50’s per barrel (Bbl) in September and October 2017, which was the last time Midland prices were significantly discounted. With the broader improvement in oil prices, producers are still better off today with the absolute price of crude at Midland at $62.50/Bbl as of April 30th. While Waha natural gas prices are lackluster for producers, Permian wells tend to be more oil-focused in terms of production, and oil predominately determines well economics – hence the greater focus on oil prices.

For midstream companies, prolonged discounts for crude and natural gas point to the need for additional infrastructure and justify the planned projects that will add pipeline capacity out of the region. For those MLPs with existing pipelines out of the Permian today, spot capacity (pipeline capacity that’s not under long-term contracts) is likely fully utilized at these price differentials. Spot rates tend to be higher than long-term contract rates, but spot capacity is also limited given that the majority of pipeline space is under long-term contracts.

Let’s take Magellan Midstream Partners (MMP) as an example, using the information in its /media/945DF57E87154EA782F669E49312CE37.ashx" target=“_blank” rel=“noopener noreferrer”>Analyst Day presentation. Committed tariffs on MMP’s Longhorn Pipeline (crude pipeline out of the Permian) average $2.30/Bbl compared to the spot tariff of ~$4/Bbl. MMP keeps 10% of Longhorn’s capacity available for spot shipments. If Midland-Houston differentials remained attractive ($4+/Bbl), spot shipments on Longhorn and BridgeTex (another Permian crude pipeline in which MMP owns a 50% interest) could add up to an incremental $30 million to MMP’s financial results on an annualized basis. Based on MMP’s 2018 distributable cash flow guidance of $1.05 billion, the potential upside is less than 3% — nothing to sneeze at but not much of a needle-mover either.

Arguably, the real beneficiaries of the widened crude discounts at Midland are those refineries that are able to purchase crude at Midland prices and enjoy the crude cost advantage in their refining margins. This includes refineries near the Permian Basin that source Midland-priced crude, as well as Gulf Coast refineries that source Midland crude via pipeline. Refineries undergoing maintenance contribute to the depressed prices for Midland crudes with their reduced demand. For example, if a refinery normally consumes 50 thousand barrels per day (MBpd) and does not process that amount for 30 days due to maintenance, then that’s 1.5 million Bbls of crude that must find an alternative outlet. Based on their earnings call comments, VLO’s management expects Midland crude discounts to narrow as refineries ramp up after maintenance, but the improvement in crude differentials may be short-lived, as discussed below.

When will pipelines catch up to production?

The article mentioned earlier raises the topic of whether producers may stop drilling due to pipeline constraints. With improvement in crude prices, the economics are likely still supportive for most Permian producers; not to mention, it takes time to adjust plans. For reference, the Permian rig count is up 54 rigs year-to-date through April 27th. The backlog of drilled but uncompleted wells (DUCs) also continues to grow in the Permian (read more). It’s hard to make generalizations for an entire basin, but it seems like the price pain we’ve seen so far is not severe enough or lasted long enough to see curbs in production. Smaller producers without committed pipeline space are more likely to hold back production.

The good news is pipeline capacity is coming, but the bad news is significant crude capacity additions won’t be online until 2019 based on current plans. Accordingly, the current futures curve for WTI Midland prices compared to WTI Cushing shows discounts as wide as $10+/Bbl in late 2018 and doesn’t show a more normalized spread of $1/Bbl until December 2019. Keep in mind, Houston prices typically trade at a premium to WTI Cushing, so the spread between Midland and Houston would likely be even wider.

In the meantime, Enterprise Products Partners’ (EPD) Midland-to-ECHO crude pipeline is slated to add 35 MBpd of capacity this month, while Plains All American’s (PAA) and MMP’s BridgeTex pipeline is expected to add 40 Mbpd of incremental capacity in early 2019. Energy Transfer Partners (ETP) expects to expand capacity of its Permian Express 3 pipeline this year. More notably, the 590-Mbpd EPIC Crude Pipeline is expected online in the second half of 2019, and PAA’s 585-Mbpd Cactus II Pipeline is similarly expected in-service in the third quarter of 2019. Phillips 66 Partners’ (PSXP) joint-venture, 700-Mbpd Gray Oak Pipeline is expected online by the end of 2019.

On the natural gas side, Waha discounts to Henry Hub improve in 2019 based on the futures curve, but the differential doesn’t narrow to less than $1 per MMBtu until 2020. In terms of pipeline additions, the 1.98 Bcf/d Gulf Coast Express Pipeline, operated by Kinder Morgan (KMI), is expected online in October 2019. The Pecos Trail Pipeline (NAmerico/Cresta Energy) is also expected to be in service in 2019, and the Permian-Katy Pipeline proposed by Sempra Energy (SRE) and Boardwalk Pipeline Partners (BWP) may come online in the third quarter of 2020.

Bottom Line

Production and pipeline takeaway capacity do not always match in a just-right, Goldilock’s scenario. Today, there’s not enough pipeline takeaway capacity in the Permian to comfortably transport the volume of crude and natural gas being produced. As a result, Permian crude and natural gas prices are trading at discounts wider than what would be justified by typical transportation costs. This creates opportunities for MLPs with spot Permian pipeline capacity, but more importantly, it highlights the need for additional infrastructure, including pipeline projects that are already under construction.

{kind=link}

{kind=link}