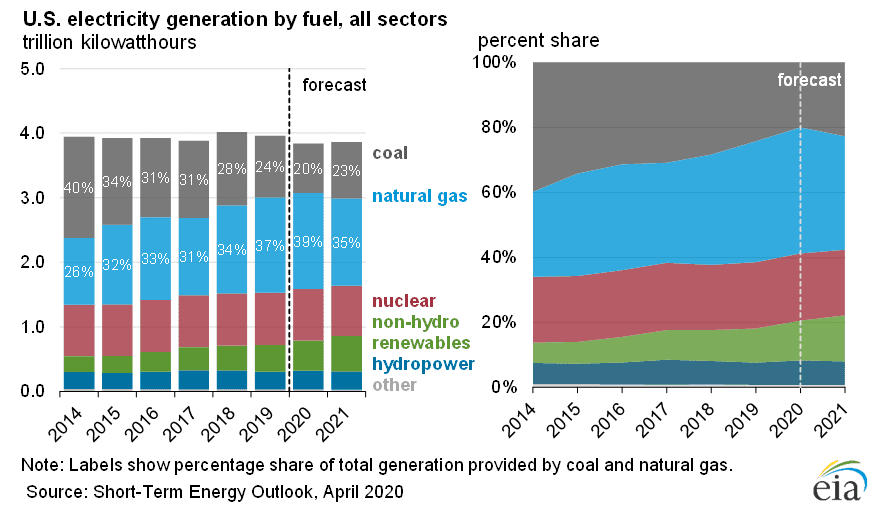

Crude inventories, prices, and production have undoubtedly been front of mind for many energy investors, but the impact of COVID-19 is far-reaching across energy. With the vast majority of Americans under shelter-in-place orders and many businesses closed until further notice, the demand for electricity generation is decreasing. Following a 1.4% decline in 2019, the US Energy Information Administration (EIA) is forecasting that annual US electric power sector generation will decline by 3% in 2020, falling below four billion megawatt-hours for the first time in over a decade. However, not all power sources will feel this demand destruction equally. The brunt of the decline is expected to be absorbed by coal given its declining production and unfavorable emissions profile. Natural gas and renewables, however, will likely emerge relatively unscathed, if not stronger. The EIA’s Short Term Energy Outlook projections show an annual decline of 20% for coal power generation this year compared to a 1% increase in natural gas generation. Through March 18, year-to-date natural gas generation was up 12% on an annual basis despite a 5% year-over-year decline in total electricity generation, demonstrating the impact that dramatically lower Henry Hub prices, new capacity additions, and perhaps some coal-to-gas switching have already had on the power generation landscape in 2020. Renewables are expected to be the fastest growing electricity source this year given lower operating costs but are not totally insulated from the impact of COVID-19, particularly in regard to new capacity. The EIA is forecasting an 11% increase in renewable generation from the electric power sector this year, but the most recent projections for new wind and solar capacity additions were lowered by 5% and 10% respectively. For context, the annual change in renewable generation represents a 73 billion kilowatt-hours (kwH) increase compared to a 17 billion kwH increase for natural gas, but renewables will still represent less than 20% of the total power mix, as seen in the charts below.

The shift in electricity generation away from coal in favor of natural gas has been ongoing for some time. As seen in the charts below, natural gas has grown from 26% of US electricity generation in 2014 to 37% last year, overtaking coal as the largest source of US electricity in the process. This transition has coincided with robust growth in natural gas production. From 2014 to 2019, dry natural gas production grew by 5.4% annually. Even with a projected decline in natural gas production this year, the EIA is still forecasting a gain in gas’s share of electricity generation from 37% to 39%. Coal’s market share is expected to decline to 20% in 2020 – half of what it was in 2014. Based on the EIA’s Hourly Electricity Grid Monitor, coal was behind nuclear energy in the power mix, representing a mere 14% of electricity generation on April 26. Natural gas still represented the largest portion at 35% on that day.

{kind=link}