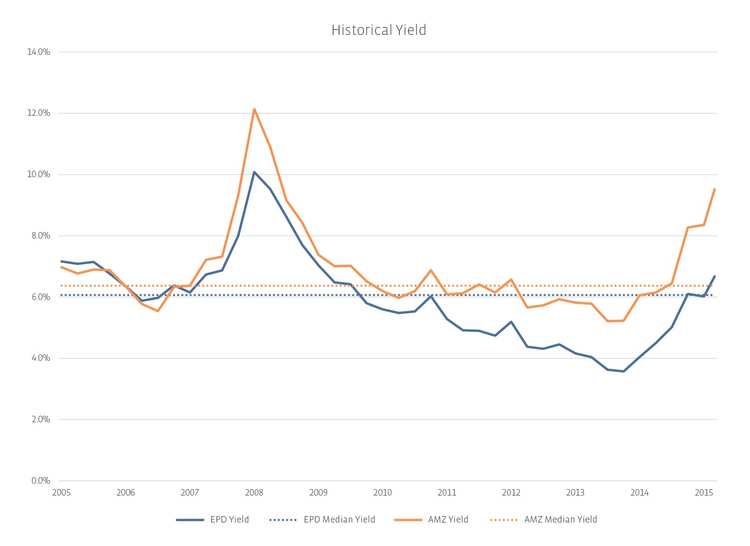

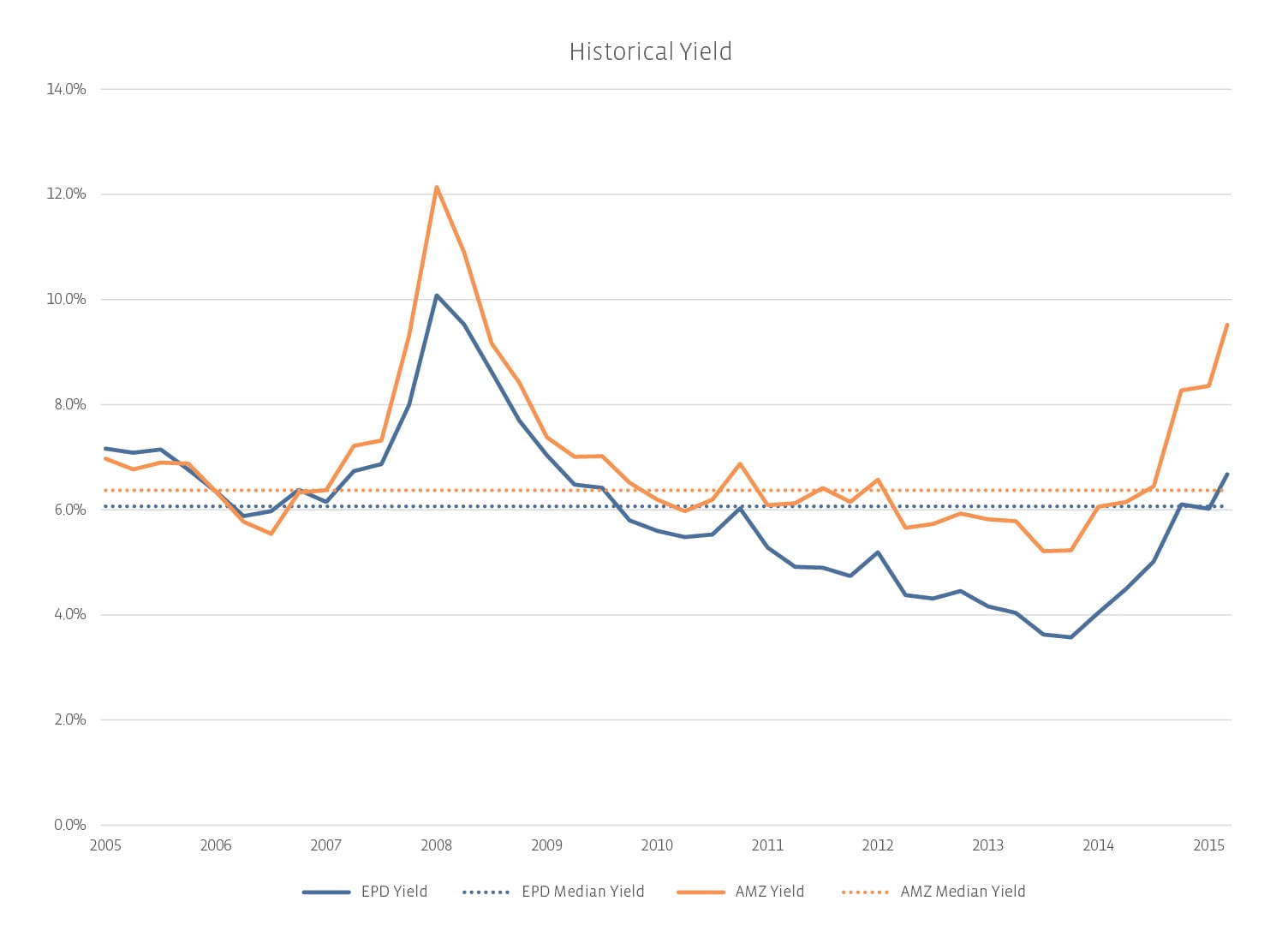

The short-comings of a yield as a valuation metric are even more prominent now that distribution cuts for midstream MLPs are within the realm of imagination (and, according to some analysts, not only possible, but probable and desirable). Cash that was previously paid out in the form of distributions is now being viewed as a potential financing source. Thus, any valuation metric that relies on the yield (which relies on the distribution) is useless.

How to Use P/DCF

To value a midstream MLP, investors will have to do some homework. Instead of simply measuring the cash distributed, investors will have to research how much cash is generated. For MLPs, the best metric to measure useable cash is Distributable Cash Flow (DCF) . Unfortunately, Alerian has yet to find a data provider who reliably calculates DCF (understandable, since DCF is quite company-specific and difficult to automate unless a computer understands how to read footnotes in SEC filings).

A basic DCF calculation begins with net income, adds back depreciation and amortization, removes maintenance capex, and adjusts for any noncash items (such as deferred income tax) and nonrecurring items (such as proceeds from asset sales).

Once DCF has been calculated, a P/DCF ratio can be calculated and compared to the company’s own historical levels as well as to peers. By including the investor’s views as to the future of the MLP, DCF can be estimated on a forward basis. And then, viola, the investor can ascertain whether the MLP is trading above or below an appropriate P/DCF ratio.

Enterprise Products Partners as an Example

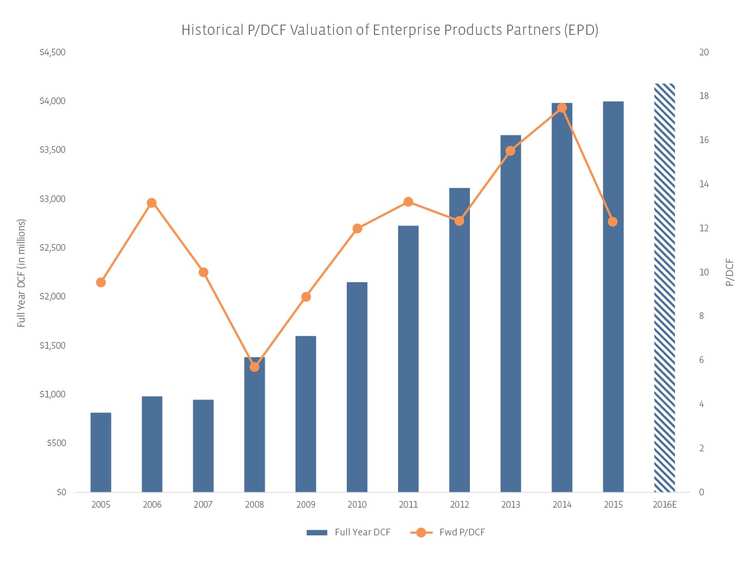

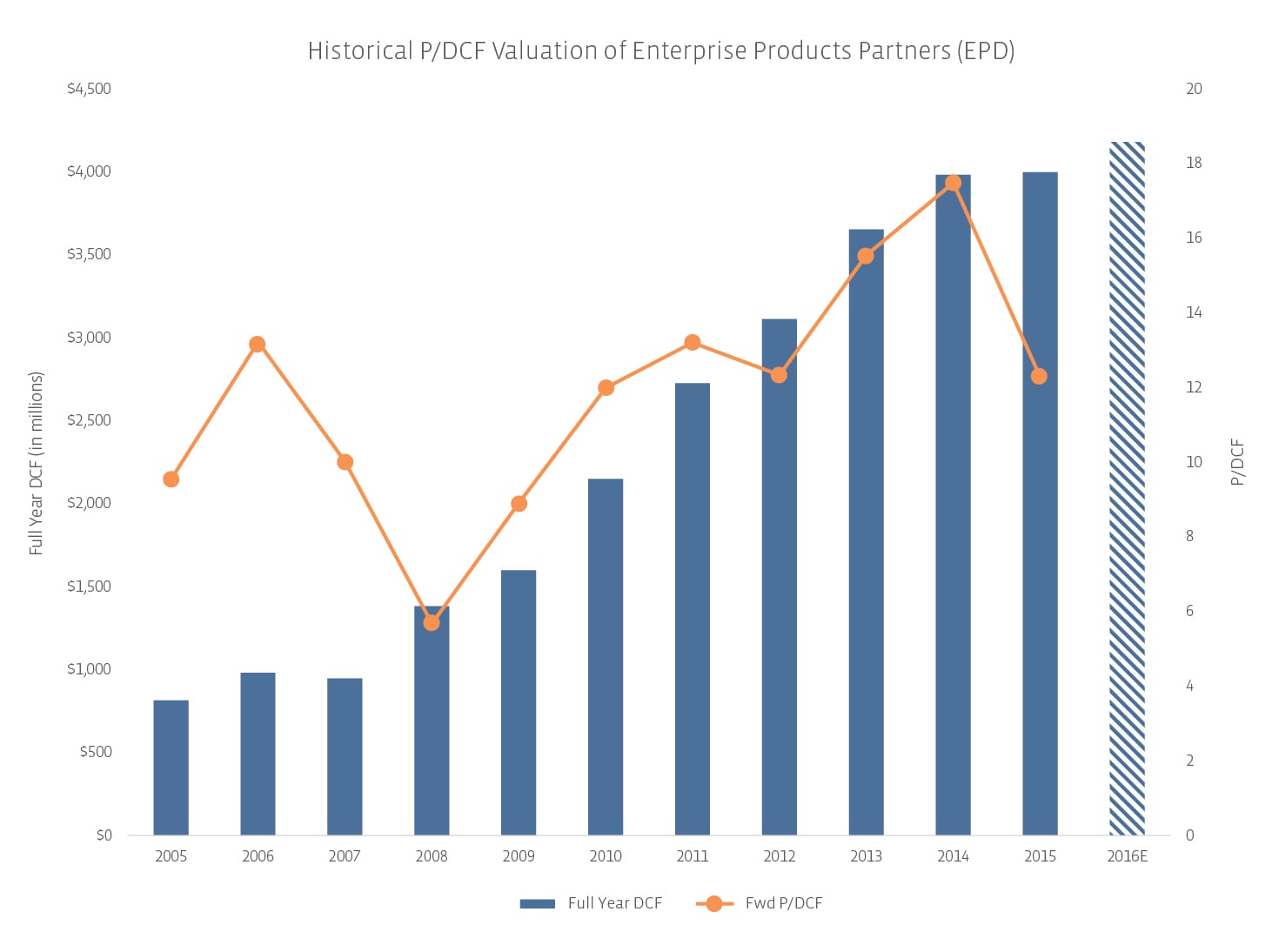

This is all easier said than done, of course. As an example, I calculated historical numbers for EPD. Earnings press releases provide all the numbers necessary to calculate ten years of historical DCF, and even include EPD’s own adjusted DCF number . Since EPD now provides distribution growth guidance, I was able to back into a projected DCF number for 2016 using an estimated coverage ratio of 1.3x .

P/DCF was calculated using the market cap on the last day of the year and the next year’s actual DCF value.

Given this projected 2016 DCF of around $4.2billion, what is an appropriate value for EPD? As I work for an indexing firm, it would be inappropriate for me to suggest a “correct” answer to that question, because it depends on the multiple you use.

Over the years, Enterprise’s P/DCF multiples have ranged from 5x-17×. In determining which P/DCF multiple to use, it comes down to risk-adjusting expected returns. Consider business model risk: businesses with more commodity exposure suggest a lower multiple. So, a small cap G&P MLP with single basin exposure should have a lower P/DCF than a large, interstate natural gas pipeline company. In other words, an investor is willing to pay a premium (higher) multiple for less commodity-sensitive or diversified cash flows. Beyond that, consider a company’s leverage: how much debt has it taken on and can it afford those payments? Does it have a supportive general partner, affordable access to capital, and backlog of visible growth via drop-down assets?

Who Should Use P/DCF

Calculating DCF and determining an appropriate multiple are a lot of work. Technical traders have their own bewildering array of algorithms, but it is those patient investors looking for value within the sector who will find the most utility in P/DCF calculations. All the same, I hope this example has given you not only an idea of a reasonable trading range for EPD, but also how to calculate these numbers for other energy infrastructure companies. It is a lot of work, I’ll grant you. But if something is worth doing, it’s worth doing right.

Edited to fix and clarify that P/DCF is market cap/DCF, not unit price/DCF.

{kind=link}

{kind=link}