Not Just Friends, But Partners

Sometimes, an upstream company and a midstream MLP will jointly own a pipeline. The upstream company appreciates secure access to capacity, and the MLP appreciates having an anchor shipper or shipper whose interests are aligned. The MLP then also will find other, third party customers for the remaining capacity, to diversify their exposure.

For a few quick examples: PXD owns an interest in a Permian gas processing facility owned by Targa Resources (TRGP). Likewise, COG and WPZ jointly own the Constitution Pipeline with Piedmont Natural Gas Company (PNY) and WGL Holdings (WGL).

Controlling the Capacity While Only Indirectly Owning It

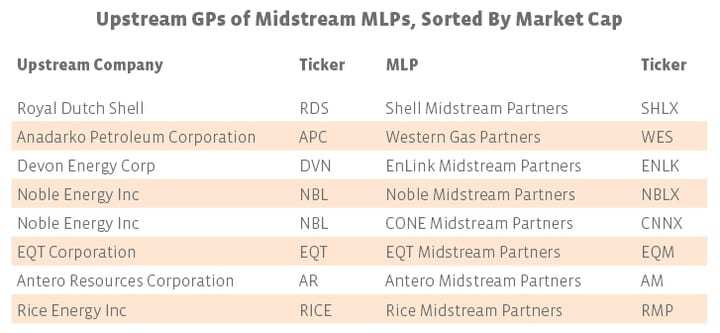

Several upstream companies have gone even farther than partial ownership of pipelines. Since midstream is generally seen as a cost center for a production company, many have formed their own MLPs for just this reason. MLPs often receive premium valuations due to their tax-advantaged status. An upstream company may form an MLP with an initial series of assets (originally built out of necessity to run the upstream business), and more assets may be dropped down over time. By retaining the GP interest and control, the upstream company assures themselves of priority access. In return, the MLP has cash flow stability via (typically) minimum volume commitments.

The other side of the coin is that having most of the business with one entity can be very risky if that entity doesn’t (or can’t) pay its bills. Years ago, Chesapeake Energy (CHK) spun off its midstream assets into an MLP known as Access Midstream Partners (former ticker: ACMP). When ACMP merged with WPZ, the contracts came with them. So, until recently, CHK was one of WPZ’s major customers. While CHK has not declared bankruptcy as had been previously feared, the announcement of the renegotiation of its contracts with WPZ removed some uncertainty around the future of WPZ. Now that investors know only 15% of WPZ’s total revenues will be dependent on CHK, they have allowed its unit price to move higher.

Obviously, this would only be one factor in an investment decision, but when considering the upstream/midstream GP/LP relationship, also keep in mind:

• how much of the LP the GP owns

• where the LP is in the IDR tiers

• the MLP’s customer and basin diversity

• how many assets are still at the GP to be dropped down to the LP

As a gentle reminder, the GP does not owe fiduciary duty to either the LP or to the LP’s unitholders.

The List

If you are looking to invest in an upstream company with a midstream MLP, perhaps it’s because you like the idea of a streamlined, exploration-and-production-only upstream company. Several of them formed the MLP by monetizing their midstream assets and a few also use the MLP as a funding vehicle. On the flip side, if you’re looking to invest in a midstream MLP with an upstream company, perhaps it’s because you like the idea of minimum volume commitments and aligned interests.

Hess Corporation (HES) filed an S-1 to launch its own MLP, Hess Midstream Partners (anticipated ticker: HESM) in 2014. However, the filing has not been updated since late 2015.

Final Thoughts

MLP investors are so familiar with midstream management teams bragging about their customers. Regardless of whether the customers are primarily upstream companies or utilities, we hear not only about how many customers they have, but also about diversity and their credit quality. It’s nice to hear the upstream companies brag about us.